- Today’s Half-Year update tells us more about the new Government’s starting point, than where it’s going. Because the forecasts were finalised before the coalition agreements were made. Nonetheless, the Treasury’s new projections paint a weaker Kiwi economy and deteriorating fiscal accounts.

- The Government’s operating deficits remain elevated in the near-term as expenses exceed revenue. The books are still expected to return surplus in the 2027 fiscal year. However, at just over $100mil, it’s more of a rounding error. There’s real risk the surplus is pushed out – once again.

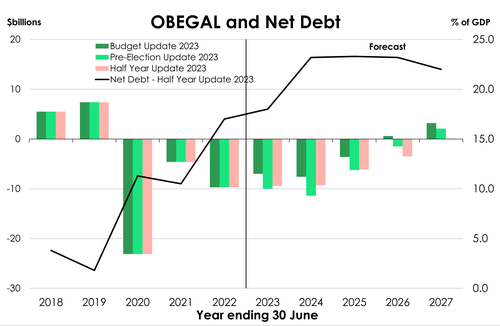

- Net debt ends the forecast period higher than had been presented at the Budget update at 23.3% of GDP. And more debt issuance is required.

The Government opened up its books for all of us (nerds) to see. However, the snapshot is a dated one. The fiscal forecasts were finalised in late November, before the coalition agreements. On top of that, the significant downward revisions in economic output this year, which were revealed last week, were also left out in the Treasury’s new forecasts. So while the economic and fiscal outlook was downgraded, you can bet it’s even uglier given the weaker starting point.

Compared, to the Treasury’s Pre-Election update (PREFU) in September, the economic projections were downgraded. Economic growth is forecast to average just 1.5% in the near-term as elevated interest rates weigh on household consumption and business investment. Strong net migration and the ongoing recovery in tourism are two offsetting factors, but the overall picture paints sluggish growth for the Kiwi economy.

A weaker economic outlook however means a weaker fiscal outlook. Today’s update revealed a deterioration in the Govt’s books. The Government is expected to run deeper deficits and smaller surpluses than anticipated a few months ago. The Operating Balance Excluding Gains and Losses (OBEGAL) is still expected to return to surplus in the 2027 fiscal year. But at just a little over $100mil, it’s hardly a surplus; more a rounding error. And it is $2bn smaller than the PREFU forecast.

A downgrade of the fiscal outlook means the Government’s debt pile is forecast to end slightly higher. Net debt is forecast to hit a high of 23.3% - still in the 2025 fiscal year, but 0.5%pts higher. Net debt is forecast to fall thereafter, but is expected to be 1%pt higher in the 2027 fiscal year. Higher finance costs and additional borrowing needs saw a lift in the NZDM’s planned debt issuance by $7bn, with particularly chunky increase in the current fiscal year of $2bn.

As for the new Government’s mini-Budget, it was just that – mini. Given that they’ve barely had time to get familiar with the new digs, we weren’t expecting much going into today’s release. And indeed, policy announcements were few and far between. We also have to wait until the new year (~March) for the Government’s Budget Policy Statement. So, what did we get today? For one thing, the new Government has managed to find $7.5bn in operating savings and additional revenue over the forecast period. It includes $2.6bn in savings by axing a few programmes of the outgoing Government.

The new Government has also committed to providing income tax relief and reducing taxes imposes on property investors. The Brightline test for residential property will be reduced to two years, from 10 years, effective from 1 July 2024. The Government has also committed to a full restoration of interest deductibility for rental properties – but they’re still ironing out the details as to how it will be rephased.

To ensure the Government’s books are back in black sooner rather than later, more cost savings will be needed. Government agencies have been called to find around $1.5bn per annum in savings. But whether that’s enough to deliver on their policy commitments, remains to be seen.

Today we received a (vague) teaser of what’s to come. But just like a movie trailer, they’ve left the plot twists and big bang announcements for Budget 2024. And in terms of (inevitable) spending cuts, next year we’ll see what’s left on the cutting room floor.

A rather redundant economic update.

Before going into any discussion of what the Treasury see’s ahead for the Kiwi economy, we have to point out it’s rather redundant. All forecasts for today’s economic update were finalised before last week’s shocking GDP number. Over the September quarter the Kiwi economy contracted 0.3% against expectations of a 0.2% expansion. And on top of that, historical data points were revised lower, showing that our economic output is in actual fact around 2% lower than we had all thought. A 2% smaller economy which was not considered in Treasury’s outlook published today. That would have a large impact on future predictions for our output. Seven months ago, Treasury erased away forecasts of the Kiwi economy entering into a recession. And for the past seven months we’ve disagreed. The economic climate has long been deteriorating and signs of slowing activity have been present left, right and centre. Yet, Treasury only sees risk of a recession on a per capita basis. We disagree. We’ve already recorded a 0.3% contraction in economic activity over the September quarter. One more consecutive  contracting quarter and that’s our recession right there…Not to mention our own forecasts saw the kiwi economy entering a technical recession over the December and March quarters ahead.

contracting quarter and that’s our recession right there…Not to mention our own forecasts saw the kiwi economy entering a technical recession over the December and March quarters ahead.

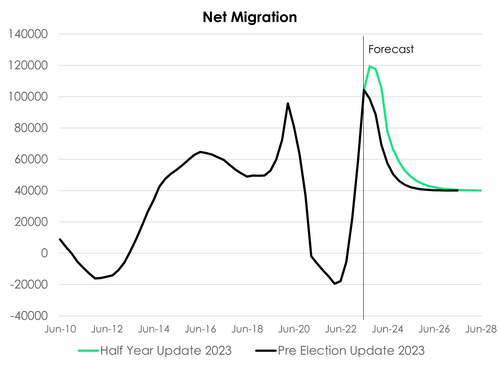

Rationale behind their strong outlook is our even stronger net-migration. And Treasury have dialled up their forecasts for migration. Though still by not enough. Again, these forecasts haven’t been touched since the 10th of November. Treasury had pencilled in annual net migration peaking in September with 119,000 annual net migrants. The data for the October year showed a further rise in net migration up to 129,000. By all accounts, a larger population does pose upside risk to inflation. It’s a large driver behind the Treasury now seeing inflation higher in June 2024 at 4.1% rather than the 3.8% they expected back in September.

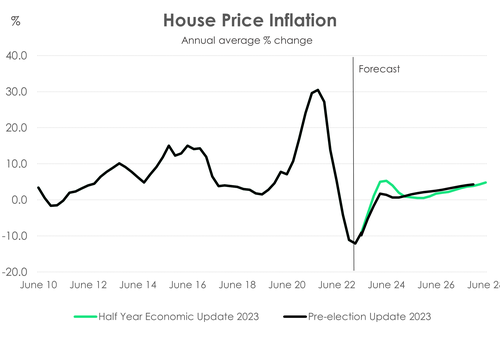

Migration remains the strongest area of concern for the inflationary outlook, particularly on housing. The surge in net migration has seen the housing market correction bottom and turn faster than previously expected. And now, migration is driving price gains. With a larger population, Treasury now forecasts house price gains to reach 5.3% in the year to June 2024. Much higher than the 1.6% gains expected in their pre-election update.

Migration remains the strongest area of concern for the inflationary outlook, particularly on housing. The surge in net migration has seen the housing market correction bottom and turn faster than previously expected. And now, migration is driving price gains. With a larger population, Treasury now forecasts house price gains to reach 5.3% in the year to June 2024. Much higher than the 1.6% gains expected in their pre-election update.

But overall, the latest (and not included) GDP numbers reveal a different story. We have a smaller economy. And even with colossal migration, output has fallen, and inflationary pressures are likely to be less.

The fiscal starting point.

Reader beware: the fiscal forecasts in the HYEFU were finalised late in November, before the new coalition government was even formed. The numbers do not incorporate: coalition agreements, the Government’s 100 Day plan and the decisions made on the Mini-Budget. The HYEFU serves more as an update of the PREFU. So consider it the new Government’s fiscal starting point. And, no surprises – the outlook has deteriorated.

Crown revenues continue to undershoot forecasts. The corporate tax take, in particular, is falling short of forecasts. It’s a clear reflection of slowing economic activity. The rising interest rate environment is taking a toll on the economy, and demand is easing. These drivers are expected to persist. But it’s a game of two halves. A strong lift in nominal GDP – helped by a larger population and persistent inflation – marginally increases Core Crown tax revenue forecasts in the 2024 and 2025 fiscal years. But thereafter forecasts were significantly downgraded, in line with new expectations of a delayed recovery in economic activity. Over the forecast period, Core Crown tax revenue track was lowered by $1.6bn compared to the PREFU.

On the other side of the ledger, the expenditure track was lifted – big time. Core Crown expenses are forecast to be higher in each year of the forecast period. Over the entire period, Crown expenses are forecast to be over $6bn more than expected at the Pre-Election update. The biggest lift in expected expense is for the 2027 fiscal year with a $2.3bn increase to forecast, compared to the PREFU. Elevated interest rates mean higher finance costs. And additional borrowings are now needed to cover the downward revision in tax revenue forecasts.

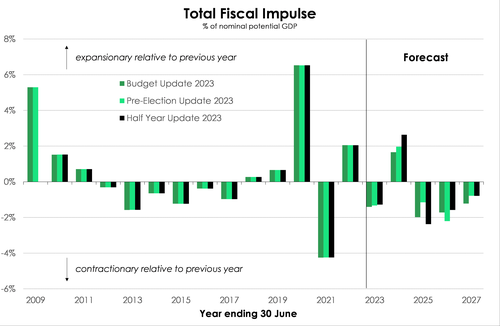

Government spending is still forecast to decline over the forecast period. However, fiscal settings are now assumed to be even more expansionary in 2023/24. Treasury’s fiscal impulse analysis provides a measure of how much fiscal policy is either adding to or taking away from aggregate demand from one year to the next. And in 2023/24, the fiscal impulse is expected to move deeper into expansionary territory. A total fiscal impulse of 2.6% of nominal potential GDP is now forecast for the 2024 fiscal year, compared to the Treasury’s 2% forecast in September and 1.7% in May. A larger fiscal deficit, driven by higher operating expenses lies behind the stronger fiscal impulse.

Government spending is still forecast to decline over the forecast period. However, fiscal settings are now assumed to be even more expansionary in 2023/24. Treasury’s fiscal impulse analysis provides a measure of how much fiscal policy is either adding to or taking away from aggregate demand from one year to the next. And in 2023/24, the fiscal impulse is expected to move deeper into expansionary territory. A total fiscal impulse of 2.6% of nominal potential GDP is now forecast for the 2024 fiscal year, compared to the Treasury’s 2% forecast in September and 1.7% in May. A larger fiscal deficit, driven by higher operating expenses lies behind the stronger fiscal impulse.

Piecing it all together, a lower revenue track and a higher expenditure track has resulted in a softer fiscal outlook. Near-term, the operating (OBEGAL) deficit is stronger than expected, given the upgrade in tax revenue. But the books deteriorate significantly from the 2024 fiscal year onwards. In 2024/26 and 2026/27, the OBEGAL is around $2bn weaker than assumed at  the PREFU. And while a return to surplus is still forecast to occur in the 2027 fiscal year, it is significantly smaller than expected at the PREFU – down $2bn.

the PREFU. And while a return to surplus is still forecast to occur in the 2027 fiscal year, it is significantly smaller than expected at the PREFU – down $2bn.

Deeper deficits, however, pushes up the eventual peak in debt load. As a share of the economy, net debt is now expected to peak at 23.3% - still in the 2025 fiscal year, but 0.5%pts higher than expected at the PREFU. Net debt declines thereafter, but is expected to be around 1%pt of GDP higher than previous forecasts. Despite the lift, the other half of the other fiscal rule is still comfortably met. At a peak of 23.3%, net debt sits comfortably below the Govt’s 30% self-imposed limit.

The Treasury has tried to capture the potential (direct) fiscal impacts from the Government’s mini-Budget. By their calculations, the revenue track would be $2.1bn higher than the HYEFU’s forecast, and the expenditure track down $5.4bn. Overall, the mini-Budget decisions is expected to improve the fiscal outlook as presented in the HYEFU. But, the Treasury concludes that when combined with future signalled commitments (e.g. tax plans), the overall impact would be “broadly neutral over the forecast period”.

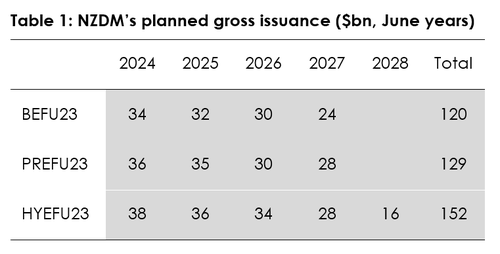

More debt, more issuance.

Deeper operating deficits, a smaller forecast tax base, and higher finance costs mean a lift in the debt profile. And more debt needed means more issuance. Planned gross issuance was increased – once again – by $7bn out to the 2027 fiscal year. The 2027 fiscal year was also added to the forecast period, with a $16bn bond programme. The planned issuance profile is below.