- The RBNZ made no changes to current monetary policy settings. The OCR remains at 0.25%, the LSAP is capped at $100bn, and the FLP ensures the supply of credit continues to flow.

- The RBNZ re-ran their numbers, and they’re suitably more upbeat. The peak in unemployment has been lowered and inflation expectations are firming. The economy has proven to be more resilient.

- The exuberance in the Kiwi housing market represents a significant challenge, however. LVR restrictions will dampen some of the investor-led frenzy. But much more needs to be done. We’d like to see the RBNZ facilitate more accurate lending rates

The RBNZ made no changes to current monetary policy settings, keeping the Kiwi economy jogging on the spot. The OCR remains at 0.25%, the LSAP is still capped at $100bn, and the FLP ensures the supply of credit continues to flow. But it was the central bank’s stance on future monetary policy that was of greater interest. Murmurs of rate hikes have been growing as the Kiwi economy has largely outperformed post-lockdown. The statement acknowledged the stream of strong local economic data that has largely surprised on the upside. But to temper the noise around rate hikes, the RBNZ placed heavy emphasis on the risks that remain. The active community cases are a reminder that we’re just one outbreak away from paring back the health and economic gains made so far. The RBNZ is indeed much closer to achieving its inflation and employment mandate than many of its peers. But in absolute terms, there’s still significant spare capacity in the labour market and current inflationary pressures can be described as transient.

“The economic outlook ahead remains highly uncertain, determined in large part by any future health-related social restrictions. This ongoing uncertainty is expected to constrain business investment and household spending growth. The Committee agreed that inflation and employment would likely remain below its remit targets over the medium term in the absence of prolonged monetary stimulus.”

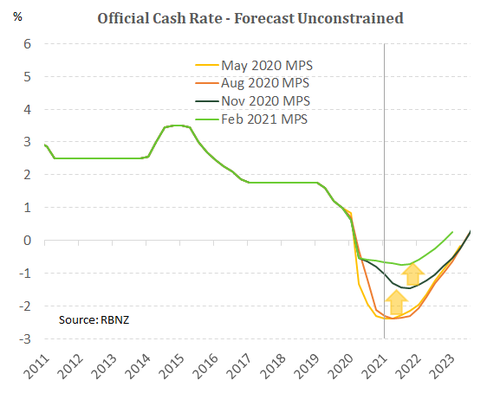

The current environment is providing ample stimulus to fuel and maintain the recovery that’s already taking shape. But the RBNZ has reassured that they remain on the front foot, and will maintain stimulatory policy until inflation is sustainably at the 2% target. The RBNZ however (again) refused to play with the OCR track, preferring to play with the “unconstrained OCR”, which was lifted again. Suggesting the impact of the LSAP (and tapering from now) will play out by the end of next year. The track does support the notion that the next move is higher, but not for a long time yet.

The RBNZ would be comfortable with the reaction in financial markets. The Kiwi dollar and Kiwi rates are little changed. The RB played a straight bat, kept policy unchanged, and squashed expectations of imminent action.

Delivering a reality check

The RBNZ’s statement downplayed somewhat the consistently strong local developments since November. The Bank wants to play a wait and see strategy, holding its nerve as it keeps settings stimulatory. And until inflation is sustainably back at the target mid-point of 2% and employment is at or above its maximum sustainable level, settings will remain supportive.

The Bank noted: “Much of what we have learned to date provides us with some indication that this higher level of economic activity will be maintained”. However, there remains considerable uncertainty around the path of recovery, particularly around how effective the global rollout of covid vaccines will be. The RBNZ provided a reality check on the surprisingly strong developments since late last year:

- Economic growth rebounded from lockdown with significant vigour in the September quarter up 14%qoq and back at pre-covid levels. But the rebound has been uneven and will remain so with our borders closed.

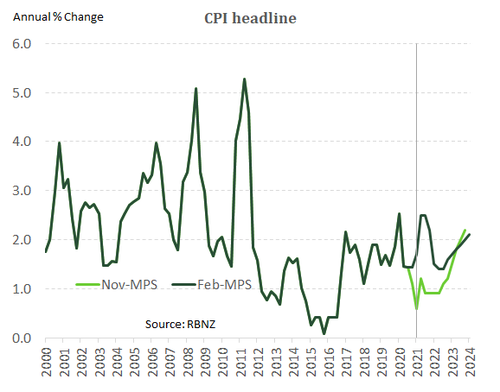

- Robust domestic demand helped generate above forecast inflation in the December quarter. And inflation is expected to strengthen in the near-term. However, only temporarily. Global supply chain disruption should dissipate.

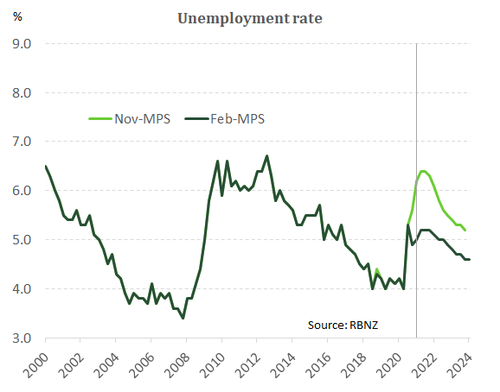

- The labour market astounded with a fall in the unemployment rate to 4.9% at the end of 2020, thanks to a sharp jump in the demand for construction and retail sector workers. Employment though, remains below the maximum sustainable level.

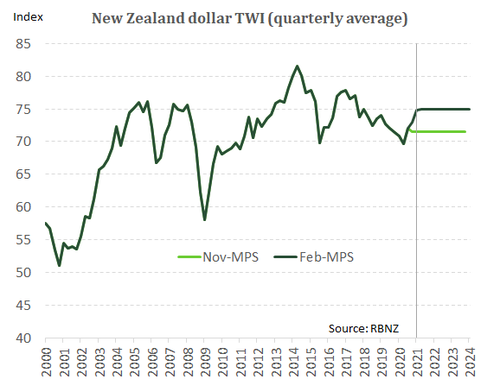

- NZ’s key export commodity prices (such as dairy) have outperformed and benefited from a faster recovery in the Chinese economy. The global economy, and demand, is dependent of the success of the international vaccine rollout.

- The housing market is running hot. Annual house price growth across Aotearoa is nearing 20%, in a market whipped up by record low mortgage rates and limited supply of listed property. But like us the RBNZ sees some of the driving forces behind frenzied house price growth wane this year.

A shade more rosy

The Reserve Bank’s new forecasts were faithful to the recent run of strong local economic data. Nearly every development since November has surprised on the upside. The bounce back in economic activity was much stronger than anticipated, the unemployment rate unexpectedly fell, and inflationary expectations are firming. Adding to the good news is our vaccine rollout. The covid immunisation programme has begun, and we are one step closer to reopening our borders. The Reserve Bank has accordingly raised the growth outlook for the Kiwi economy. A second technical recession is no longer forecast, the peak in unemployment has been revised lower and CPI is expected to be nearer to the 2% target than forecast in November.

The Reserve Bank’s new forecasts were faithful to the recent run of strong local economic data. Nearly every development since November has surprised on the upside. The bounce back in economic activity was much stronger than anticipated, the unemployment rate unexpectedly fell, and inflationary expectations are firming. Adding to the good news is our vaccine rollout. The covid immunisation programme has begun, and we are one step closer to reopening our borders. The Reserve Bank has accordingly raised the growth outlook for the Kiwi economy. A second technical recession is no longer forecast, the peak in unemployment has been revised lower and CPI is expected to be nearer to the 2% target than forecast in November.

The RBNZ is closer to achieving its dual mandate than many of its peers and far sooner than previously believed. But there’s still significant spare capacity in the labour market, with unemployment still forecast to rise to 5.2%. And while the risk of deflation may have dissipated, current inflationary pressures may simply be described as transient. Inflation is forecast to rise to 2.5% later this year then falling back to 1.4% by Q2 2022. Temporary supply chain disruptions are largely underpinning these price pressures. Furthermore, the active community cases are a reminder that we’re just one lockdown away from paring back the health and economic gains made so far. The outlook for the Kiwi economy may be brighter, but remains highly uncertain. Given the risks, monetary policy will have to remain accommodative for some time. For fear of moving first and pushing up the exchange rate, the Reserve Bank will have to join the choir of other central banks, rather than sing lead.

Market reaction

The RBNZ played a straight bat. Nothing in the statement was surprising, and Orr stuck to script in the press conference that followed. The statement acknowledged the upbeat economic developments to date, yet placed heavy emphasis on the risks that remain around covid. Vaccine rollouts, coordinated monetary easing and massive fiscal (Govt) support packages have traders pricing in higher rates of growth and inflation. But most of the “good news” was already priced. The Kiwi was trading at 73.5c heading into the announcement and is now sitting relatively unchanged at 73.7c. Kiwi rates too were little changed. The 2-year swap rate started the day at 0.39%, and found itself a little higher at 0.41%. The 2-year swap rate had been trading negative (-0.01%) as late as November last year. The reaction in financial markets was to be expected.

The lack of action in financial markets reflects that the RBNZ largely delivered as expected. It’s a job well done in shifting the rhetoric from negative rates to a neutral stance without causing too much volatility. The RBNZ would be comfortable with the reaction in financial markets.

The lack of action in financial markets reflects that the RBNZ largely delivered as expected. It’s a job well done in shifting the rhetoric from negative rates to a neutral stance without causing too much volatility. The RBNZ would be comfortable with the reaction in financial markets.