- Kiwi house prices have been rising, modestly, since May. House prices have risen 2.1% since May, and May may be the low in this correction. There are signs of further strength to come. The true litmus test for the housing market will be in spring. And we expect to see an uplift in confidence and activity.

- House prices are down 16% from the November 2021 peak (up from -18% in May). The RBNZ’s rapid rate rises restrained demand. We look to rate cuts next year. If realised, the housing market will recover faster.

- Our forecast peak to trough correction of -20%, may prove to be a bit pessimistic. Migration is also surging. And the 100,000 additional migrants will need at least 40,000 houses. Houses we haven’t built.

The true litmus test is now.

Kiwi house prices rose a solid 0.9% in the month of August. The housing market looks to have found its footing and is going into the warmer months with a bit of a “spring” in its step. Indeed, it’s the months of spring that will be the true litmus test for housing. And we’re expecting the buoyancy to continue. Because the surge in migration is providing additional demand to an already tight market.

National house prices have fallen 16% from the peak, slightly better than the -17.7% peak to trough recorded in May. Over the last year, house prices are down just 4.7% (up from -14% in March). And let’s not forget the massive 47% gain in the 18 months to November 2021. It was these extraordinary gains over 2020-21 that prompted such an aggressive response from the RBNZ. Interest rates were ratcheted higher to wrestle house prices back down to more “sustainable” levels. House prices are now at more sustainable levels. They’re not at affordable levels. But they are not as extreme as they once were. We think that the correction for past excesses has now run its course.

Policy must focus on supply, rather than restraining demand. All our housing market problems stem from a lack of supply. And our lack of supply is linked to a lack of infrastructure maintenance and investment. Investors are not the villains here. They’re just an easy target.

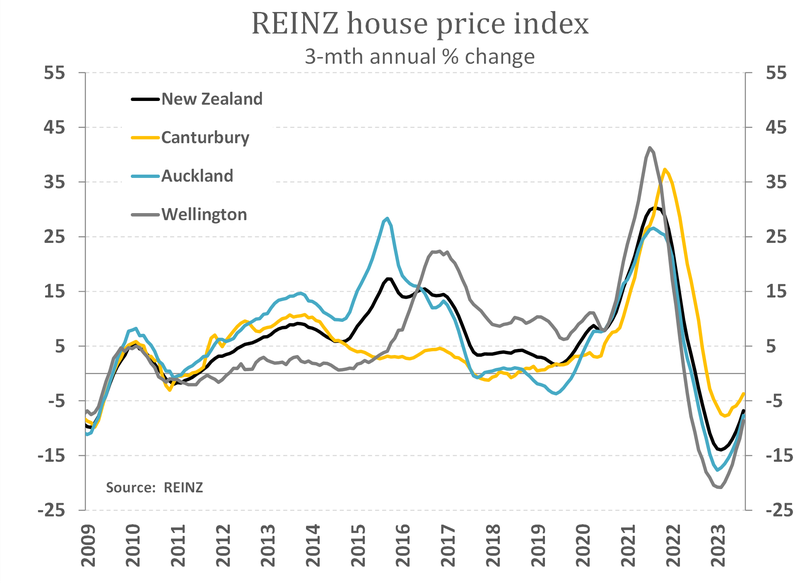

Our first chart plots the swift swing higher in momentum. It looks like we can put a stake in the ground, with May 2023 being the trough in house prices. The peak in interest rates, about now, coincides with the bottom of the downturn. And rate cuts, hopefully next year, will support the rebound. Migration is also surging, adding demand.

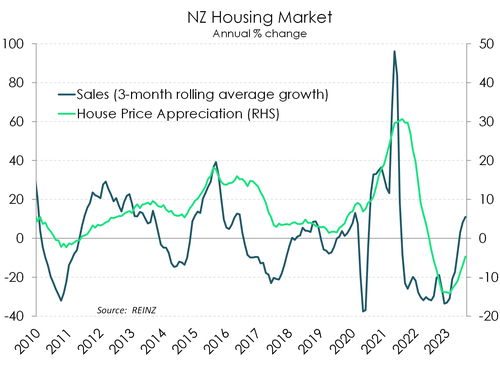

Our second chart plots the undeniable uplift in activity. Sales have rebounded and point to an uplift in prices.

Our second chart plots the undeniable uplift in activity. Sales have rebounded and point to an uplift in prices.

Proof of concept will take place over the warmer months. As the housing market thaws out from a cold, and frustratingly wet, winter, we will see a sharp bounce in activity, and potentially price gains – modest gains. There are signs of hope, or hopeium as Darcy Ungaro puts it in his latest podcast (see Property on Hopium: Jarrod Kerr).

In our regional outlook titled “It was a cold winter, and regional activity was frost bitten in parts”, we highlighted some of the anecdotes from our business bankers and mortgage managers across the country. In short, things are not as bad as the data suggests, especially in housing.

A spring in your step.

House sales have picked up 9.2% over the last year. Remember, house sales had fallen a whopping 37% in 2022. So we’re bouncing back, strongly. Where sales go, prices follow. And the major cities are leading the way.

Despite the lift in prices and solid activity, the days to sell still reflects a buyers market. The number of days it takes to sell fell from a frustratingly long 49 to 43, compared to a long-term average of 39. We expect the days to sell to speed up in spring.

Confidence in the market is better gauged over the warmer months. We expect interest rates to fall into 2024, net migration is surging, and there’s still a shortage of dwellings. Price gains are likely to continue.

In the real capital, Auckland, house sales have bounced 18%, having fallen 40% in 2022. And the average days to sell has fallen from over 50 days to around 40 days now. The days to sell is still higher than normal, but the sharp fall is encouraging. The rebound in activity, and drop in days to sell, has seen house prices in the ‘city of sales’ lift 3% since May. House prices are down 5% over the year, and are off 21% from the November 2021 peak. But the momentum points to continued gains from here.

“I am seeing more of an opportunity for the first home buyer with the price reductions. Certainly not favourable for the seller.” Joe Tongotea Mobile Mortgage Manager

In the other capital, Wellington, house sales remain down 2.5%, after falling 30% in 2022. Activity is taking a little longer to recover, but there has been a material decline in the days to sell. Days to sell have fallen from close to 70, to a little under 40. That’s a big shift. House prices are down 5% over the year, and are off 22% from the November 2021 peak. Again, the uplift in momentum points to price gains.

"It appears to be picking up steadily, and with low stock on the market this is likely to push prices up again as demand continues to rise." - Nadine Davison, Mobile Mortgage Manager, Wellington

In the garden city, Christchurch, prices have not fallen as far, and the rebound is a little more entrenched. House prices have fallen, but only -7% peak to trough. Days to sell is about average, so nothing to worry about here. And activity has picked up, with a strong 25% gain in sales over the last year.

“The outlook is positive for the Garden City.” Greg Bramley - Senior Property Finance Manager, South Island.

Across the regions, the housing market is primed for a recovery. Regional housing markets are springing to life in spring. For much of the past two years, regional housing markets capitulated under the pressure of tightening credit conditions (CCCFA), rapidly rising mortgage rates, investor tax policy changes and stretched affordability. The correction may be over. It looks like the regions are playing catch up to major cities. There were mixed gains and losses across the regions, but green shoots have emerged.

In the mighty Bay of Plenty, sales activity has kicked up, and the days to sell has fallen from the lofty levels (over 70!) of last year. Confidence is returning, although the days to sell of 50 still reflects a weak market. Prices in the Bay are down just 4% over the year, and 15% from the 2021 peak.

“I think the post-election period will see a flurry of activity again – it will be spring, and people and people keen to move before Xmas. Summer brings people into this region which almost always creates demand for property from people wanting to move here. I don’t see prices falling much unless the labour market tanks.” Donna Neville, Mobile Mortgage Manager, Bay of Plenty

In Mooloo territory, the housing market is showing some promise. The days to sell has come in lower at 49 days, compared to recent prints close to, and above, 60. Sales activity has bounced, rising at a double digit (+16%) pace.

“Customer enquiries are heating up post a cool winter. FHB are back, and refinancing is a big talking topic.” Leanne Richards, Mobile Mortgage Manager, Waikato

In Northland, house prices are down nearly 10% over the year, and off 13% from the 2022 peak. Sales activity is mixed. And we have yet to see a convincing return. Watch out over spring and summer.

In Northland, house prices are down nearly 10% over the year, and off 13% from the 2022 peak. Sales activity is mixed. And we have yet to see a convincing return. Watch out over spring and summer.

Across much of the South Island, housing markets remain soggy, with weak sales activity and long days to sell. Prices are bottoming, and look to recover in coming months.

Otago paints the picture. Sales activity was still weak in winter, and the days to sell are long and hard. But prices are improving. And we should see a bounce in spring.

"Feels like it's starting to pick up with there being more 'bang for your buck' out there. Looks like there is some really good buyer demand and Dunedin is starting to stabilise. There is a good window for buyers to get out there and buy but it hasn't yet flowed through to value." - Leanne Hannah, Mobile Mortgage Manager, Dunedin.

A rebound is underway.

There are three drivers of the housing market. Firstly, falling mortgage rates will support confidence and activity next year. Although mortgage rates have risen recently, we expect to see falls in mortgage rates into next year. Secondly, the demand/supply imbalance will worsen. The surge in migration and the loss of dwellings at high risk of climate change will only exacerbate the housing shortage. And finally, the residential construction boom is cooling quickly. The number of dwellings coming to market will fall back from very high levels. The growth in demand, with a migration boom, will once again outstrip supply in coming years. All three drivers point to a strengthening housing market, and price gains. We are likely to see a continuation of monthly house price gains – albeit very modest gains – in the warmer months. We forecast annual gains creeping up to 2% by the first quarter of 2024, before hitting a high of 6% by the middle of next year.