The unemployment rate tumbled to 3.9%

Key Points

- A surprise swoon in the unemployment rate to 3.9% - an 11-year low – shows the market remains a bright spot in the NZ economy.

- At 1.7% yoy employment growth in the June quarter was better than expected, and the number of people unemployed fell. Kiwis remained engaged, with a steady participation rate. And the decline in unemployed people saw the unemployment rate tumble to 3.9%, from 4.2%.

- The chunky $1.20/hr hike to the adult minimum wage was an unsurprising driver of wage growth in the quarter. The private sector LCI was up 2.2% yoy, well ahead of general inflation over Q2 (1.7%yoy).

- The labour market stats are what we call a lagging indicator. They take a while to turn. And the strength in the numbers does not reflect the pessimism in business surveys.

- The report won’t add a great deal to the RBNZ deliberations this week. We believe the RBNZ will deliver a 25bp cut to 1.25%. And the RB will continue to cut to 0.75% in this cycle.

- Female participation continues to climb, even in the Kiwibank economics team.

Kiwibank Summary

The labour market report was undoubtedly strong. The pick up in employment was impressive, but so was the drop in unemployment. The participation rate was unchanged, and that meant the unemployment rate tumbled to just 3.9%. The Kiwi unemployment rate is now at the lowest level since 2007. That’s great news. The other good news in the report was the strong lift in wages growth. It appears firms held off last quarter, but paid out this quarter. The impact of the higher minimum wage has now come through. The labour market is decidedly tight at present. Other metrics of slack in the labour market, such as the underutilisation rate fell too. The underutilisation rate came in at 11%, again an 11-year low.

But it is old data reflecting an economy of yesterday. Labour market statistics are lagging, by about 9 months. The strong growth we experienced last year has slowed, and the forward-looking indicators have deteriorated – esp. business confidence.

All eyes now turn to the RBNZ on Wednesday for the latest MPS. A 25bp cut to the OCR to 1.25% seems a foregone conclusion. More importantly is what the Bank does next. Given heightened global uncertainties and a deteriorating outlook domestically we now expect the RBNZ will be moved to cut the OCR to below 1% at the start of 2020.

A fresh perspective

Despite the global economic slowdown, the latest labour market data release shows everything where it should be – the unemployment rate has fallen to an eleven year low of 3.9%, we’ve seen the largest percentage increase in average ordinary time hourly earnings since June 2009, and wage rates increased at a strong 2.1% annually. Minimum wage increases requiring increased wages from the private sector as well as multiple collective agreements formed to provide higher pay for professions such as nursing play a factor in this.

The report reflects positive outlooks for minorities. The female employment rate is the second highest on record and we’ve seen a 0.7% decrease in underutilisation. This is due to continued social progress – increased acceptance in the workplace and more career opportunities, nationally and globally. More pressing requirements for a financially stable household are another significant factor.

Meanwhile, Māori unemployment rate has fallen to 7.7%, its lowest point since the June 2008 quarter, down from 9.4% last year. A continued decreasing trend of minority unemployment will yield positive economic benefits in the long run as we increase the scope and diversity of the labour force. Despite this, work is still to be done to make career paths more accessible for these people, as well as ensuring more wage equality in the industries.

While the data looks pleasing, it doesn’t warn us of the forecast headwinds. The outlook for the coming year is still negative as we begin to feel the effects of the global economic slowdown more prominently.

This section was written by Sofia Angelova Bray and Aishi Jain of Westlake Girls High School. Sofia and Aishi are economists for the day, at the mighty Kiwibank. The economics teacher at Westlake, Dan Renee, once inspired our Chief Economist at Rosmini College (too many years ago).

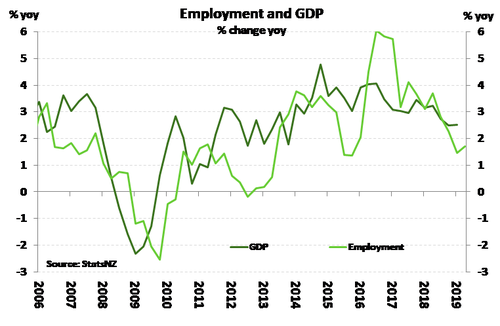

Employment bounces

Following on from a disappointing fall in employment in the March quarter, employment rebounded 0.8%qoq in Q2. Both full- time and part-time employment contributed to employment growth over the period. This was stronger than we had expected, but still doesn’t bode well for growth (see chart below). Adding to the solid HLFS numbers, the number of those unemployed were 7,000 people less in the quarter. Looking at the detail there was plenty to like about the HLFS numbers. Māori and the young (two groups that tend to have worse labour market outcomes than the average) showed falls in unemployment.

time and part-time employment contributed to employment growth over the period. This was stronger than we had expected, but still doesn’t bode well for growth (see chart below). Adding to the solid HLFS numbers, the number of those unemployed were 7,000 people less in the quarter. Looking at the detail there was plenty to like about the HLFS numbers. Māori and the young (two groups that tend to have worse labour market outcomes than the average) showed falls in unemployment.

The Quarterly Employment Survey’s (QES) measure of employment, full-time equivalent employees, was 0.7% qoq higher. However, this measure isn’t directly comparable to the HLFS’s employment number. Annual employee growth was 1.8% yoy and has been trending lower in recent years.

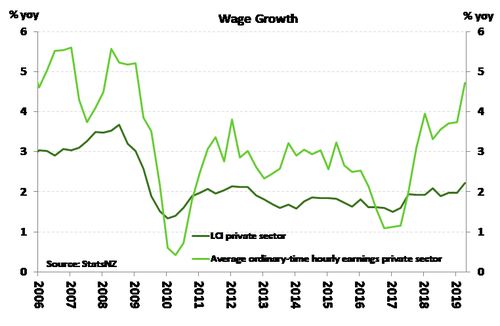

Minimum wage hike delivers a boost to pay

It looks as though firms held off until the June quarter to put through wage hikes following unusually weak inflation. The private sector Labour Cost Index (LCI) jumped 0.8%qoq to take annual wage inflation to 2.2%yoy. Annual wage growth was the highest since the 2.6%yoy recorded back in June 2009. A key contributor to a lift in wage growth was the 1 April $1.20/hr hike to the adult minimum wage to $17.70/hr. In terms of its impact StatsNZ noted that if wages impacted by the minimum wage had remained constant, then underlying wage growth would have been 0.5%qoq – a decent rate of underlying wage growth given recent history. Adding to the evidence were the industries that experienced the biggest gains in wage rates. Industries such as retail and accommodation services – industries that typically have a large proportion of workers on the minimum wage – recorded the largest wage rises.

It looks as though firms held off until the June quarter to put through wage hikes following unusually weak inflation. The private sector Labour Cost Index (LCI) jumped 0.8%qoq to take annual wage inflation to 2.2%yoy. Annual wage growth was the highest since the 2.6%yoy recorded back in June 2009. A key contributor to a lift in wage growth was the 1 April $1.20/hr hike to the adult minimum wage to $17.70/hr. In terms of its impact StatsNZ noted that if wages impacted by the minimum wage had remained constant, then underlying wage growth would have been 0.5%qoq – a decent rate of underlying wage growth given recent history. Adding to the evidence were the industries that experienced the biggest gains in wage rates. Industries such as retail and accommodation services – industries that typically have a large proportion of workers on the minimum wage – recorded the largest wage rises.

Market Reaction

The financial markets were forced into action today. It was meant to be a boring number ahead of the RBNZ. But it was anything but boring. Kiwi swap rates are +5bps higher as a few stops may have triggered. Traders have accumulated heavy long positions in bonds ahead of the expected RBNZ rate cut tomorrow. Where rates go, currencies follow. The Kiwi flyer is a little higher. NZD/USD jumped from 0.6513(ish) to 0.6587(ish) before stabilising around 0.6565(ish). The Kiwi flyer is trading around our forecast 65c, but is likely to ease towards 63c (at below) by year end.

Despite the small back up in interest rates on today’s report, the trend has been amazingly clear. Interest rates around the world have fallen, and the US-China trade conflict has fuelled the fear in the rush for safety.