- The Kiwi unemployment rate has fallen, again, to 4.7%. And more workers have been attracted into the labour force, with a good lift in participation. Wages were up as well. And women dominated the search for work.

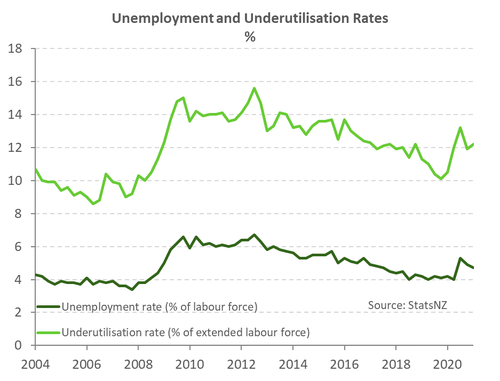

- The was a slight lift in underutilisation, people wanting more work, but that was skewed higher by the Auckland lockdowns during the Americas cup.

- The gains in wages over the quarter were stronger than we expected, as firms try to attract workers (without access to migrants).

- Today’s report is unlikely to veer the RBNZ ship off course. The economy is in a far better position. But the RBNZ’s mandates are still far from being met. Monetary policy settings will likely remain supportive over the coming year.

New Zealand’s labour market has continued to improve, against all odds. The drop in the unemployment rate to 4.7% bet our estimate of 4.8%. And we were the lowest, or most optimistic, in the consensus of economists, ranging from 4.8 to 5.2%. Today’s report was a great read, and confirms the strength of the Kiwi economy. The economic scarring from Covid lockdowns is far less than anyone had predicted 6 months ago.

There were 15,000 jobs created over the first quarter, with 5,000 fewer unemployed. The labour force participation rate rose from 70.2 to 70.4%, as workers were attracted back. And firms offered a larger carrot, to get workers. Wages lifted 0.4% over the quarter, against our upbeat estimate of 0.3%, to be up 1.6% over the year. Wages will jump again in the second quarter, as the April 1st minimum wage hike kicks in.

The labour market has completely confounded forecasters. During the depths of the nationwide lockdown, a double-digit unemployment rate had seemed more likely than not. There’s no doubt that the fiscal support - particularly the early deployment of the wage subsidy - was instrumental in safeguarding employees. Many businesses adapted and jobs were protected through the pandemic. And the recovery momentum is likely to continue.

The slight dampener in the report, was the lift in the underutilisation rate – more people wanting to work more hours. The underutilisation rate rose from 11.8% to 12.2%. Auckland was the source of the lift in underutilisation, and the two Auckland lockdowns – during the America’s Cup – played a part.

The strength in the labour force reflects the underlying strength in the economy, and highlights the adaptability of Kiwi business. We have entered 2021 on a firmer footing. There is solid momentum across the economy. A 4.7% unemployment rate is a fantastic outcome. Provided we make our way through 2021 without any major lockdowns, we’re firmly fixated on the light at the end of the Covid tunnel. Statistics on Covid cases are already becoming overwhelmed by statistics on Covid vaccinations. And next year may be the year of international travel.

Under the hood

Employment indicators throughout the March quarter suggest strong labour demand coming through. Job ads were at record highs and business confidence surveys report strengthening employment intentions among firms. But anecdotes suggest that the closed border continues to weigh on firms’ employment decisions. But while the closed border was felt deeply in areas reliant on tourism, the damage doesn’t appear widespread.

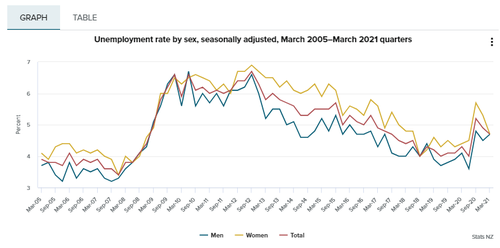

The number of people employed lifted once again by a modest 0.5% in the quarter. And women made up 78% of the quarterly rise. Over the past two quarters, there have been some strong gains in labour market outcomes for women. With 8,000 fewer women unemployment, the female unemployment dropped steeply from last quarter’s 5.3% to 4.7%. However, the annual changes reveal that the labour market is yet to return to pre-Covid levels. Annually, there are still almost 4,000 more women unemployed, and 15,000 no longer in the labour force. Another worrying trend is the majority of those wanting more hours to work are women in part-time employment. Compared to men, women continue to have a higher rate of underemployment.

The number of people employed lifted once again by a modest 0.5% in the quarter. And women made up 78% of the quarterly rise. Over the past two quarters, there have been some strong gains in labour market outcomes for women. With 8,000 fewer women unemployment, the female unemployment dropped steeply from last quarter’s 5.3% to 4.7%. However, the annual changes reveal that the labour market is yet to return to pre-Covid levels. Annually, there are still almost 4,000 more women unemployed, and 15,000 no longer in the labour force. Another worrying trend is the majority of those wanting more hours to work are women in part-time employment. Compared to men, women continue to have a higher rate of underemployment.

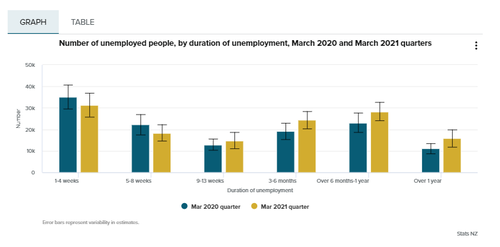

Another area of concern, is the slight lift in the duration of unemployment. When comparing the March quarter 2021 to 2020, there has been a drop in the number of people out of work for up to 8 weeks, and a lift in the number of people unemployed for longer than 9 weeks. It appears those workers displaced, and struggling to obtain new jobs. The Stats NZ department has seen a significant, and unhealthy, lift on the number of unemployed for 6 months or more. The report highlights the difficulty of losing jobs in a struggling industry, or tourism town, and the need to help mobility and retraining.

Wage pressure builds

Wage growth, as measured by the private sector Labour Cost Index (LCI) rose a modest 0.4% in the quarter, lifting annual wage inflation to 1.6%yoy. Annual wage growth entered the pandemic at just under 2.5%, but has been shunted lower because of Covid. Moreover, firms have held back on increasing wages ahead of the minimum wage rising to $20/hr from 1 April. Looking ahead, we are expecting a gear shift in wage growth in the second quarter. The minimum wage hike and base effects of subdued pay movements during lockdown will be in play.

At 12.2%, the underutilisation rate is still almost 2%pts above pre-covid levels. However, the past two labour market reports have painted a faster-than-expected recovery of the labour market. As the remaining slack continues to erode, the belt around the labour market tightens. And the tighter the labour market, the more pressure on wage growth. And wage inflation is not as easily dismissed by the Reserve Bank as inflation generated by temporary supply disruptions.

The RBNZ is unlikely to veer off course following today’s report. The Kiwi economy is performing far better than anyone’s best guesses. But we’ve not yet crossed the finish line. Orr & Co. will likely keep monetary policy settings accommodative and supportive over the coming year.