- We now expect a shallower correction in house prices of 6%, down from 9%. With short supply persisting, our projected house price falls should meet strong resistance.

- The regions have fared far better than expected. Covid lockdowns barely affected farming, and the ‘working from home’ trend is fuelling demand.

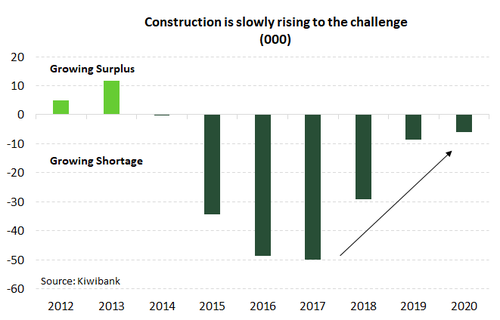

- The supply of homes has increased sharply. But we’re still falling short to the tune of 80,000 houses. The impact of Covid-19 casts a long shadow over the construction industry into 2021. Commercial property looks likely to bear the brunt of the adjustment.

We warned of a correction early, but may be surprised.

In April, during the most intense shut down of economic activity in living memory, we issued a warning. We said the lockdown was likely to cause a spike in unemployment to over 10%, and house prices would follow a similar, but inverted path, falling 9%. At the time, we highlighted the very real risk of a much higher unemployment rate of 15%, and therefore a much deeper correction in house prices. Since leaving lockdown earlier than expected, we’ve become more optimistic. We now expect a modest decline in house prices of 6% (down from 9%).

We’re simply more comfortable that the downside risks are receding. And that’s a massive change in mindset. We continue to expect the unemployment rate to creep towards 9%, but the impact on housing is likely to be reduced. The impact of the lockdown is far greater than any other economic event since the Great Depression. But it lasted only 6 weeks. Unlike previous recessions, the impact on the financial system was limited. Banks are lending, and the appetite to do so remains strong. If all goes well (big if), a 5-6% dip in house prices would represent a very mild reaction to such a dramatic economic upheaval.

There are 3 strong foundations supporting the housing market:

- The housing market has a chronic shortage;

- Mortgage rates are at record lows;

- Population growth will continue, after the disruption.

Pay attention to the regions.

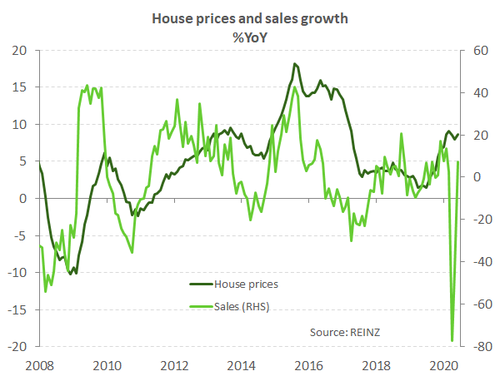

At the national level, the housing market is making a vigorous comeback. April’s lockdown merely delayed settlements, and pent-up demand. Stay-at-home orders meant ‘for sale’ signs were left in the car boot and agents took Sundays off. But the housing market has fired up since leaving lockdown. Following back-to-back monthly price falls, house prices rose 0.9% in June with good momentum into August. Annual house price growth also lifted and is on track to return to the 9%yoy rate seen pre-Covid. The +6,000 house sales were the highest tally for a June month in four years. And realestate.co.nz recorded a whopping 20%yoy spike in listings in July. The market is playing catch-up.

A regional breakdown shows some regions are faring better than others. Because measures taken to combat Covid-19 have had a disproportionate impact on the economy. Farming was considered an essential service. And farmers have fared well with strong output and solid prices in dairy, meat and other essential products. Regions of the “old economy” have weathered yet another storm (and drought).

Whanganui/Manawatū, Wellington and Canterbury are the star performers coming out of lockdown. Each region recorded surprisingly strong rebounds in house sales and prices. Waikato, Taranaki, Christchurch, Bay of Plenty, Hawkes Bay, Gisborne and Northland are also doing remarkably well, all things considered. Whereas Queenstown, Rotorua and Auckland are more affected by the locking out of international tourists.

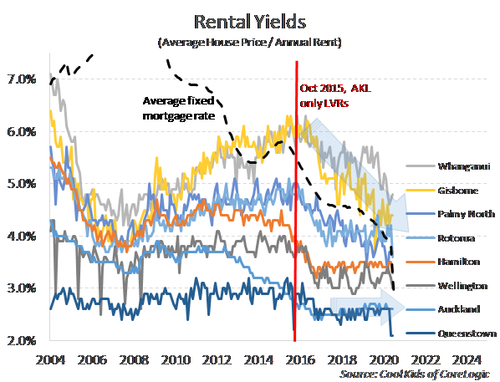

We asked our network of regional managers to give us a ‘feel’ for activity across the regions. We incorporate their insights below.The big attraction of the regions, for investors, is rental yield. Deposit rates have tumbled well below 2%, and mortgage rates have fallen well below 3%. In a lower for even longer interest rate world, rental yields play a greater role in the decision to invest in property. The regions typically offer a higher yield to the major cities, with Whanganui, Gisborne, and Invercargill conspicuously above 4%. Most of the regions sit comfortably above 3.5%, and compare nicely to Auckland’s 2.6%. Queenstown is going through a difficult adjustment. Rents are falling. Previously lucrative Airbnb accommodation is now offered for long-term rent, and at a time when tourism-related employment is in doubt. Corelogic’s latest data show a sizable drop in rental yield to just 2.1%. House prices are falling, but rents are falling faster.

Queenstown brings mixed emotions in a tough time, 4/10

“New properties are selling, esp. “Jacks Point”. That said there are many more Airbnb properties utilised as long-term rentals. Residential rents are down. Will these properties hit the market, or will people be able to hang on for post Covid?” Andrew Voss Senior Commercial Manager

“New properties are selling, esp. “Jacks Point”. That said there are many more Airbnb properties utilised as long-term rentals. Residential rents are down. Will these properties hit the market, or will people be able to hang on for post Covid?” Andrew Voss Senior Commercial Manager

“I feel our community is optimistic as we are known as the “Adventure Capital of the World”. The closed border has allowed domestic travellers to come experience this slice of the adventure and pick up some very good deals as lots of local tourism companies are working together. Kiwis are coming here to experience what most have said that in the past they couldn’t afford... Once the wage subsidy comes off, and if local employers can’t retain their staff, household incomes could be impacted. We may see a rise in housing stock on the market as people either can’t afford their high new built mortgage or they have to leave town.” Sarah Russell, Business Manager.

Northland is attracting (WFH) Aucklanders, 7/10

“The housing market remains buoyant with demand strongly outweighing supply in the lower to mid-levels; however the upper end is now stagnating as discretionary income is less readily available.” Clarc Morris Area Manager

“The housing market remains buoyant with demand strongly outweighing supply in the lower to mid-levels; however the upper end is now stagnating as discretionary income is less readily available.” Clarc Morris Area Manager

Northland may be picking up steam. Mangawhai continues to experience relentless growth (with Aucklanders finding an affordable alternative). A little further north, there’s been a significant pick up in inquiry and construction (renovations especially) around Whangarei heads. The ability to work from home looks to be a key factor driving the recent spike in interest.

Bay of Plenty feels like 8/10, with not so plenty housing

“The Bop housing market continues to show strong demand from buyers, particularly in new builds. Some housing companies have up to 90 individual deposits paid, waiting for house and land packages. Forward work for the building and construction sector continues to look positive with our clients suggesting they have more than enough to keep them occupied for the next 12 months. Motels have it hard, the ones not accommodating social housing are averaging around 40% occupancy.” Nick Hosking, Senior Commercial Manager

“The Bop housing market continues to show strong demand from buyers, particularly in new builds. Some housing companies have up to 90 individual deposits paid, waiting for house and land packages. Forward work for the building and construction sector continues to look positive with our clients suggesting they have more than enough to keep them occupied for the next 12 months. Motels have it hard, the ones not accommodating social housing are averaging around 40% occupancy.” Nick Hosking, Senior Commercial Manager

The front line ‘8/10 feeling’ has yet to be picked up in the data, Real Estate Institute NZ (REINZ) data shows the BoP housing market lagging behind. House prices recorded a second consecutive drop in June and the median number of days to sell soared to 73 days, a 9-year high. Following the trajectory of most other regions, next month should see the market bounce back.

Whanganui/Manawatū is ‘hot in the city’, and feels like 7/10

“In the words of Billy Idol, Hot in the City. Whanganui and Manawatū are seeing high demand due to low supply and strong record sales since we have come out of lockdown. Still strong migration from the more expensive cities. Rental Yields are still high, although have reduced by about 2% on the back of a rising median sale prices. The region is not reliant on the Tourism market, there was already a large pipeline of infrastructure and shovel ready projects pre-Covid. Tradies and Businesses are enjoying the massive sugar rush but have concerns about the wave that might be behind them, therefore holding off employing staff.” Natalie Sara, Business Manager

“In the words of Billy Idol, Hot in the City. Whanganui and Manawatū are seeing high demand due to low supply and strong record sales since we have come out of lockdown. Still strong migration from the more expensive cities. Rental Yields are still high, although have reduced by about 2% on the back of a rising median sale prices. The region is not reliant on the Tourism market, there was already a large pipeline of infrastructure and shovel ready projects pre-Covid. Tradies and Businesses are enjoying the massive sugar rush but have concerns about the wave that might be behind them, therefore holding off employing staff.” Natalie Sara, Business Manager

Whanganui/Manawatū recorded a 3.7% monthly rise in June, and the number of monthly sales has returned to pre-lockdown levels.

Gisborne feels like a steady 6/10, with businesses back.

“The majority of businesses in the Bay of Plenty and Gisborne regions have returned to near normal trading levels seen at this time last year, with the obvious exceptions being motels and tourism. Forestry in Gisborne has come back on stream with contracts being offered for harvesting of up to 5 years. There is big investment in horticultural production being undertaken at the moment, particularly in kiwifruit and avocados. The first Medicinal Cannabis extraction facility is now complete, with commercial licenses being issued before Christmas. The completely new industry in the region will need over a 100 staff in the first 3 years.” Nick Hosking, Senior Commercial Manager

“The majority of businesses in the Bay of Plenty and Gisborne regions have returned to near normal trading levels seen at this time last year, with the obvious exceptions being motels and tourism. Forestry in Gisborne has come back on stream with contracts being offered for harvesting of up to 5 years. There is big investment in horticultural production being undertaken at the moment, particularly in kiwifruit and avocados. The first Medicinal Cannabis extraction facility is now complete, with commercial licenses being issued before Christmas. The completely new industry in the region will need over a 100 staff in the first 3 years.” Nick Hosking, Senior Commercial Manager

The mighty Hawke’s Bay feels hot, 9/10

“I have a number of customers actively looking for rental properties. Looking for high yields. Bars and restaurants have had a record June, with matched turnover from the Summer period. High end luxury accommodation was up 150% on last year, with good forward bookings for rest of the year. There are a lot of 1st time visitors who couldn’t go on overseas trips.” Karl Trafford, Business Manager.

“I have a number of customers actively looking for rental properties. Looking for high yields. Bars and restaurants have had a record June, with matched turnover from the Summer period. High end luxury accommodation was up 150% on last year, with good forward bookings for rest of the year. There are a lot of 1st time visitors who couldn’t go on overseas trips.” Karl Trafford, Business Manager.

“What Covid downturn? Hawke’s Bay property market is still red hot, just like the climate. Strong demand, short supply, properties selling quickly. Investors are active… The need for feed. Hawke’s Bay has been hit by a severe drought. Farmers’ resilience levels tested. On the upside, try and find a tradie at less than a months’ notice – mate you’re dreaming!” Garth Duncan, Senior Commercial Manager.

The Hawke’s Bay only experienced one monthly setback and began bouncing back in May – a month earlier than most. And housing market activity continues with gusto. Prices rose 2% in June and the median number of days to sell is already back to pre-lockdown levels. Should there be a second lockdown, bunkering down in the Bay doesn’t sound like a bad idea. There’s no need to stock up on alcohol.

Auckland feels like a 4-6/10, depending on traffic

“Millennials are battling baby boomers at auction sites in Auckland for tiny pieces of this city, while everyone else shakes their heads in disbelief at the property prices (post lockdown, mid global pandemic). It still takes 2 hours to get anywhere when it rains…” Namrata Heble, Business Manager

“Millennials are battling baby boomers at auction sites in Auckland for tiny pieces of this city, while everyone else shakes their heads in disbelief at the property prices (post lockdown, mid global pandemic). It still takes 2 hours to get anywhere when it rains…” Namrata Heble, Business Manager

“Houses in Akl market are still selling, but only to those with high incomes. The rest of us spend an hour in a traffic jam next to a car that has more power going to its speakers than its wheels.” Ged Curtain, Senior Commercial Manager

Auckland is the gateway to the North. But the drawbridge has been raised. Auckland’s rebound is showing less vigour. Prices are slowly trekking higher, but with a long shelf-life. The median number of days to sell is yet to return to pre-lockdown levels. Nonetheless, Auckland’s housing market is heating up into spring. Take for example the 40%yoy spike in listings on realestate.co.nz, Barfoot’s highest sales performance in July for five years, and the recent 300-person viewing party for a brick-and-tile granny’s flat. You’ll only find more Jaffas in a Cadbury sack, or rolling down Baldwin street. Record low interest rates and loosened LVRs are pulling more first home buyers, and investors, off the sidelines – as intended.

The Waikato, MooLoo territory, is just $100 away, and 6/10.

Many Aucklanders continue to leave in search of a better life. The Auckland price of petrol, however, means many only make it as far as Hamilton. “Housing prices are firm with agents reporting a lack of stock on the market and open homes are well attended. Investors are looking to take advantage of low interest rates. Work from home opportunities are driving an increase in out of town buyers looking to bring families to Hamilton for the great schools and 1 hour travel to either coast. Builders have plenty of work for 2020, and they have voiced concerns that there may be a lack of sections coming on the market in 2021 so demand may continue to outstrip supply”. Lincoln Trent, Commercial Manager.

Many Aucklanders continue to leave in search of a better life. The Auckland price of petrol, however, means many only make it as far as Hamilton. “Housing prices are firm with agents reporting a lack of stock on the market and open homes are well attended. Investors are looking to take advantage of low interest rates. Work from home opportunities are driving an increase in out of town buyers looking to bring families to Hamilton for the great schools and 1 hour travel to either coast. Builders have plenty of work for 2020, and they have voiced concerns that there may be a lack of sections coming on the market in 2021 so demand may continue to outstrip supply”. Lincoln Trent, Commercial Manager.

Windy Wellywood feels like a blustery 8/10

“A shortage of supply still dominates the market with no indication that the rise in house prices is slowing. Residential rentals may have now plateaued.” Peter Charlesworth Regional Manager

“A shortage of supply still dominates the market with no indication that the rise in house prices is slowing. Residential rentals may have now plateaued.” Peter Charlesworth Regional Manager

“FHB enquiry is increasing with few new listings coming on the market. As is always the case, when there are many buyers and few listings house prices continue to increase. The market is very competitive with most houses listed for tender resulting in multi-offer situations. There is a big focus on residential construction which has led to land prices steadily increasing. FHB trend is moving toward northern suburbs and Wairarapa for more affordable housing.” Philippa Scott, Mobile Mortgage Manager

Taranaki housing market is a strong 7/10

“Realtors across the region are reporting soaring house prices and a shortage of listings. July, August are traditionally the quieter months but it’s the opposite at the moment. There is competition between investors and Kiwi’s returning to the Amber and Black province, which is making it difficult for first home buyers.” Jayden Devonshire, Regional Manager

“Realtors across the region are reporting soaring house prices and a shortage of listings. July, August are traditionally the quieter months but it’s the opposite at the moment. There is competition between investors and Kiwi’s returning to the Amber and Black province, which is making it difficult for first home buyers.” Jayden Devonshire, Regional Manager

Canterbury feels like a resilient 7/10

“Our clients are selling stock at the ‘affordable’ end of the market in Christchurch (land or townhouses / houses to be built). They’re moving them like hot cakes. And they can’t build them fast enough. Further up the value chain it feels a bit slower…” Greg Bramley, Property Finance Manager

“Our clients are selling stock at the ‘affordable’ end of the market in Christchurch (land or townhouses / houses to be built). They’re moving them like hot cakes. And they can’t build them fast enough. Further up the value chain it feels a bit slower…” Greg Bramley, Property Finance Manager

The end of lockdown meant the Christchurch rebuild could resume. Paused projects can flow through the pipeline once again, breathing new life into the market. Moreover, wider Canterbury is heavily backed by the rural sector. And our primary industries are expected to perform relatively well in the post-Covid recovery period. The rebuild and resilience of Canterbury sets a floor under how low house prices will drop.

Otago, excluding Queenstown, is a little stronger with 6/10

“Still seeing an imbalance between listing numbers & buyers, with more properties being purchased than listed. Reduced stock, increased competition, continues to place an upward pressure on prices.” Leanne Hannah, Mobile Mortgage Manager.

The damaging impact of shutting out the rest of the world is starting to show among our tourism-centric regions. House prices fell in Otago for a fourth consecutive month, and are down 5.6% since February. But house sales jumped in June and were a little higher than the same month last year. Homeowners may already be feeling the pinch, feeling forced to sell, and compelled to accept a lower price. The absence of international tourists questions the survival of many tourism operators. And with job security tied to border reopening, the date for which is tbc, the housing market is set to cool further.

Job losses will mount in the region. We can expect an exodus of people to neighbouring cities, looking for other lands flowing with milk and honey (employment, that is). Greater migration should support the housing markets in neighbouring cities.

Our housing shortage persists…

In August 2018, we identified a staggering shortage of 100,000 dwellings (see here). We re-ran the model in 2019 (see here), and given StatsNZ’s population estimates, we found a significant worsening to 130,000. The migration boom had continued. And the shortage had worsened. The shortage ballooned despite the industry’s best efforts to boost supply. The construction sector was firing on all cylinders at the time. Solving NZ’s chronic shortage of affordable dwellings seemed even more difficult with(out) Kiwibuild.

So where do we sit now?

Well, with the stroke of a pen, StatsNZ made some rather large revisions to population estimates, that should have been clear from the 2018 census. Basically, our “team of 5 million” took longer to get to 5 million. The ‘revised’ population estimates are 50,000 short of the numbers we used this time last year. And an economic model is only as good as the data you pump through it.

- Despite the debacle that was our census, NZ still has a chronic housing shortage. We (re)estimate the shortage to be 80,000 and growing.

- The supply of homes has increased sharply. But we’re still falling short. And the prolonged impacts of Covid-19 cast a long shadow over the construction industry into 2021. Commercial property looks likely to bear the brunt of the adjustment.

- With housing in such short supply, our projected house price falls should meet strong resistance.

…but perhaps not for much longer

The construction sector has geared up to build the houses we need. And the start of the year we were finally building enough homes to offset growth in demand. NZ looked set to start addressing the housing shortage that had built up since 2015. Then along came Covid-19, lockdowns, and a bubble of 5 million. And then there’s the flood of Airbnbs reluctantly hitting the market. The outlook for construction activity has been upended.

But there’s a glimmer of hope for the residential construction sector. It turns out that the “Building Together” Budget involves actual building. A $5bn housing spend was stipulated in the May Budget. Over the next five years, the Government aims to build 8,000 new state homes. The investment is on top of the 6,400 homes already promised which are currently “in the pipeline”. The package should encourage employee retention and provide companies with some certainty planning ahead. Well, that’s the intent. The project however is showing some semblance to its (disappointing) older brother, Kiwibuild. But with a more realistic target, and some slice of the $1.6bn trades training funding pie, Kiwibuild Jr. could stimulate the weakened sector and reduce our housing shortage.

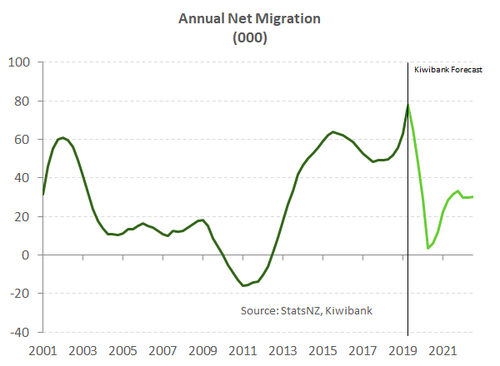

NZ’s population growth surged 2%yoy in the first quarter of the year. That’s a rate of population growth we haven’t seen since late 2016 – at the height of the last migration boom. Net migration was the main driver, hitting a new record high of almost 85,000 people in the year ending March. Kiwis returned home in droves as NZ headed into lockdown. The typical net outflow of Kiwis reversed into a rapid inflow. But there was another element contributing to the jump in net migration. StatsNZ noted a significant number of short-term arrivals stayed in the country as Covid-19 engulfed the world. Leaving NZ became difficult, given a lack of departing flights. And some visitors may have decided to stay put until things blew over (and they’re still waiting).

However, the surge in population growth is not expected to be sustained, in the near-term at least. Net migration is falling fast. The closure of our borders to all but NZ citizens and residents, has seen the cross-border flow of people evaporate. We are set to see annual net migration plunge from here, while our borders remain closed. We are forecasting annual net migration to fade to a paltry 3,500 by March next year. With the number of Covid-19 cases rising at a frightening pace outside NZ, the prospect of our borders opening anytime soon looks remote.

However, the surge in population growth is not expected to be sustained, in the near-term at least. Net migration is falling fast. The closure of our borders to all but NZ citizens and residents, has seen the cross-border flow of people evaporate. We are set to see annual net migration plunge from here, while our borders remain closed. We are forecasting annual net migration to fade to a paltry 3,500 by March next year. With the number of Covid-19 cases rising at a frightening pace outside NZ, the prospect of our borders opening anytime soon looks remote.

We are assuming that NZ will re-open borders around the middle of next year. But we understand the significant degree of uncertainty around the timing of open borders. And we could be in a situation of restricted international movement for years to come. Falling net migration is expected to see housing demand ease into 2021. So long as the building sector can keep the current pace of building, NZ’s housing shortage will fall next year.

We must bear in mind that migration data is subject to significant revisions. Because StatsNZ uses the so called 12/16-month rule. A long-term arrival is someone who spends 12 of the next 16 months in NZ. And a long-term departure is someone 12 of the next 16 months living abroad. These numbers can be thrown around as people change their mind. At present, the significant number of short-term arrivals staying in NZ, could easily become outflows in coming months. Future updates to net migration figures will probably be thrown around somewhat.

An outflow of Kiwis is unlikely at present. Labour markets around the globe have been ravaged by Covid-19. Likely putting off even the most intrepid Kiwi intending on an OE. And the willingness of Kiwis to move overseas must have been reduced by the virus itself. But for those brave enough to leave God’s country, key long-term destinations have fewer restrictions on Kiwis. So you’re a Kiwi human rights lawyer, and you actually want to move to Amsterdam? Come on in. You don’t have to isolate. Tell us how you guys did it?

When our borders are reopened, we expect to see a lift in both Kiwis heading offshore, and migrants knocking down the door. The Covid-19 pandemic has strengthened Kiwi.inc. Our reputation as a must-see country has gone from strength to strength. And there’s been a spike in foreigners wishing to move to NZ as a result. Longer term, NZ as a destination, either a tourist destination or final destination, should see net migration remain supportive of economic activity and housing.

A lack of job security will weigh on demand for housing

Slowing population growth won’t be the only element sapping housing demand over the second half of the year. NZ’s labour market has come under the strain of Covid-19 and the associated lockdown. Jobs have been shed and the unemployment rate is heading for the highest rate in around 30 years. Job security is an important driver of confidence among individuals to buy and invest in housing – typically the largest financial decision someone will make in their lifetime. And job security is likely to come under renewed threat for many.

According to the latest unemployment rate at least, the labour market has so far weathered the Covid-19 crisis unscathed. If the headline number is to be believed, the unemployment rate fell to 4% in the June quarter. Yes, NZ managed to come out of lockdown much sooner than many had thought possible. But we can’t fathom that the unemployment rate would fall during the greatest economic crisis since the great depression. And in reality, it didn’t. To be counted as unemployed someone must be actively seeking paid employment. It was impossible to actively seek anything during lockdown. Many people that would have usually been counted as unemployed in Q2 were classified as being outside the labour force. Underlying data tells a more damaging story. The total number of hours worked plunged over 10% in the second quarter. And around 650k people were either away from jobs, worked fewer hours than they wanted, or were less active over the quarter.

NZ’s labour market clearly isn’t unscathed, and the June quarter is far from the low point in the current crisis. Cushioning the blow to the labour market has been policy such as the Government’s wage subsidy. And the current form of the wage subsidy will come to an end in the coming weeks. Applications for an extended 8-weeks of subsidy for employees was opened from June 10 and closes on the 1st of September. That means early applicants will be close to exhausting the latest subsidy. We expect to see further job losses as some firms still face difficulty retaining staff post subsidy. Unless of course the Government announces another extension to this policy. But an additional extension looks unlikely at this stage unless NZ is forced back into some form of lockdown.

Another concern for the labour market is NZ’s closed border. Short-term visitor arrivals into NZ look like an increasingly distant prospect. And once NZ’s sugar rush of post lockdown spending wears off, firms reliant on international visitors will be exposed once again. Finally, international developments have deteriorated in recent months. The surge in cases of Covid-19 is putting the recovery of nations previously thought to have controlled the pandemic at risk. The US is the most obvious example. But there are rising cases in some of our key trading partners such as Australia and the European Union. We are expecting another round of job losses over the second half of 2020. And an unemployment rate that will peak over 9% in the final quarter of the year. For the housing market, a rising unemployment rate doesn’t bode well for housing demand and house price growth.

Covid-caused commercial construction conundrum

The Covid-induced lockdown has accelerated the trend toward a more digitized world. Our spending data has shown a structural break higher in online shopping. We were already moving towards the convenience (and greater choices) of online shopping, but being stuck at home for 6 weeks sped up the move. Many consumers tested online shopping for the first time, and had a good experience.

More importantly, we shopped more online as we worked from home. And now many businesses are taking the opportunity to rethink their workspaces. Many service-based businesses, including accountants, lawyers, bankers, and any sales force, are embracing the ability of staff to work more from home. Scheduling staff days in, and out, of the office is enabling many businesses to reduce floor space. It’s a productivity push that is helping many firms cut costs on costly overheads, and actually boost output. Studies have found that employees working from home spend more time on their computers. In Auckland’s case, cutting 2 hours of infuriating time spent in traffic, brings a valued lift in workplace well-being. It’s the way of the future.

But what does that mean for commercial property? A shift to working from home will change the nature of many places of work. If a large share of the workforce continues to work from home, office space in our largest centres will be freed up, helping to boost productivity. Businesses may find more resources to invest in the next opportunity. On the flipside however, the commercial property sector will likely face the challenge of reduced demand. We expect to see a continued increase in available office space (leases) into 2021. We are already hearing anecdotes of commercial property projects being shelved, or even converted into residential projects. Construction is running at high capacity, finishing off existing projects, but there’s likely to be a significant drop in commercial space into 2021. NZIER’s latest Quarterly Survey of Business Opinion noted similar observations. Architects are feeling uninspired and their pencils remain sharp as they expect a fewer visits to their loft office.

Many industries may grab onto opportunities made available by disruptions to global supply chains. The inevitable reallocation of resources towards more productive firms and processes will have benefits. The faster adoption of productivity enhancing technologies such as AI and automation seem obvious.