The Kiwi economy expanded 0.6%qoq to post a 2.5% annual rate. The details are a little shaky in the Isles, however.

Key Points

- The NZ economy had a respectable start to 2019, expanding 0.6%qoq. The annual rate of 2.5% was slightly above expectations. But growth will cool.

- Construction was the key driver of growth, with “higher investment in both residential and non-residential building”. We suspect the strong growth to cool from here, as capacity constraints bite.

- The primary sector was weak across the board, due to dry conditions. Retail was soft with weaker (Chinese) tourist numbers. The service sectors posted weak results, the softest since 2012.

- We expect growth to ease in 2Q 2019 to ~2.2%. The path (higher) into 2020 is dependent on the fiscal impulse. Further easing by the RBNZ and a weaker currency should assist.

Summary

Growth at the start of 2019 was slightly ahead of forecast. The economy has posted a 0.6%qoq, on par with December quarter growth, taking annual growth to 2.5%yoy. But recent indicators of activity suggest growth will weaken. As had been already signalled, construction sector activity was a key contributor to growth at the start of 2019. However, services sector activity posted a meagre 0.2%qoq – the weakest rate since 2012. Weak tourist numbers, slowing population growth, and a quiet housing market were key reasons for this. A slowing service sector is concerning. Service sector growth tends to be a stable source of growth and makes up around two-thirds of the economy.

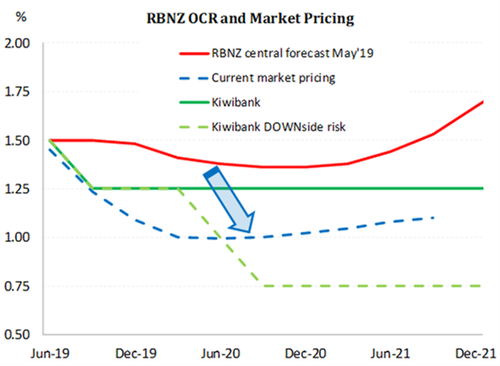

As we outlined in our updated forecast note last week (Fake Plastic Trees), growth is likely to weaken. We are forecasting growth to fall to around 2%yoy in the June quarter. The economy is growing below its potential and with other central banks cutting rates or looking to add stimulus, the RBNZ has more to do to ensure inflation can get back to target. We don’t see the Bank cutting the cash rate at next week’s OCR review. We expect the RBNZ to use the full forecasting round with the new Monetary Policy Committee in August to make the next big decision. We expect the RBNZ to deliver another cut in August to 1.25%. After all, it’s only another 6 week wait. Financial markets (via a lower currency and wholesale interest rates) have done some of the work for the RBNZ in recent weeks. Although more work is required. We still believe there’s a 40% chance the RBNZ is forced to keep going to 0.75%.

We can’t just build our way out

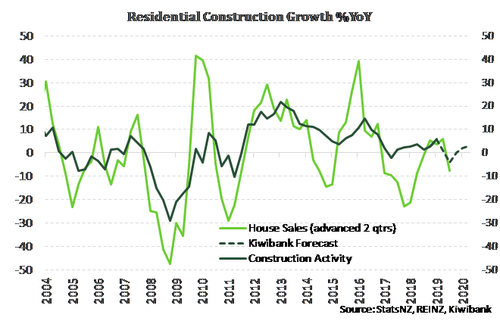

Construction activity was the stand-out performer at the beginning of the year, expanding 3.7%qoq. That’s a rate of expansion that was common back in 2015, at the tail end of the Canterbury rebuild surge and as the sector geared up to meet the growing demand for homes in Auckland. Both home building (2.7%qoq) and commercial construction (9.9%qoq) activity boomed in the March quarter. Given the shortage of housing NZ still has, this is a welcome result. However, we don’t expect stellar growth in the construction sector to continue. Because it physically can’t! Capacity constraints are a major impediment to the sector and NZIER’s quarterly business survey shows us that builders capacity utilisation has been periodically punching survey highs since mid-2015. Moreover, residential building is linked closely to the fortunes of the housing market (see figure below). Housing market activity remains weak, a cooling housing market reduces the incentive to build and renovate.

In what has been uncharacteristic for the economy of late, the services sector has contributed little to growth. Services expanded only 0.2%qoq, which was the lowest rate of growth since 2012. And services make up around two thirds of the NZ economy. Population growth is now easing and so too is the growth in demand for services in general. Within services there were falls in several categories, including transport and retail and accommodation. The latter is likely to have been driven by a fall in tourist numbers. Visitor arrivals to NZ, particularly from China, dipped at the start of the year. The Chinese economy has been under pressure from an escalating trade war, which is hitting growth. Rental and hiring services recorded a 0.2%qoq dip. The industry is closely linked to the property market and the slowdown in housing market activity is likely to have played a big part here.

Primary sectors had another tough time, contracting 2.3%qoq and follows a 0.3%qoq fall at the end of 2018. Adverse weather, particularly the dry conditions faced by many at the start of the year, contributed to a hit to farming and forestry activity. Mining activity was surprisingly strong, lifting almost 10%qoq on the back of exploration activity and oil and gas extraction. The jump occurred despite disruption to the biggest producing gas field (Pohukura) for repair and maintenance over the period. Perhaps oil and gas producers are bringing exploration activity forward following the Government’s future ban on offshore drilling.

Expenditure growth was good

On the expenditure side of the equation, the economy grew 0.8%qoq. Spending expanded across the board. Household spending lifted 0.5%qoq. Investment activity was driven by solid construction sector work. Meanwhile, export growth held up on strong dairy exports – likely to be from the impressive run-up in milk production at the start of the season.

Per capita growth fails to impress, again!

GDP per capita was weak, again. GDP per person rose just 0.1% in Q1 2019, after an upwardly revised, but still weak 0.2% reading in Q4 2018. GDP per capita has risen just 0.9% over the year, and remains at the lowest rate since 2011. We’re still in the largest migration boom in the nation’s modern history. We expect a bit of indigestion as you throw a record number of people into the equation. Even if the stats department don’t know exactly how many people there are. Population growth is slowing, and as the past rise in net migration is integrated into the economy, should help support higher per capita GDP growth.

Market Reaction

Market traders were drawn to the US Fed statement overnight. The Fed have appeased calls for rate cuts and acknowledged the growing “uncertainties” around the US economic outlook. The Fed dropped the term “patient”, implying a move is coming. The Fed downgraded the pace of economic activity to “moderate” from “solid” and were forced to rebase their inflation expectations lower. James Bullard dissented on the decision, opting for a 25bp rate cut. The tide has turned. The Fed’s dot plots imply two rate cuts into 2020. The market has 4-5 rate cuts priced, with the Fed fund futures showing 1.3% rate by December 2020 (down from 2.25-2.5% today). We believe the market is fairly priced. We expect two 25bp rate cuts from the Fed this year. And we expect at least another two 25bp rate cuts from the Fed next year. If delivered, the Fed funds rate will fall to a 1.25-1.50% band. The RBNZ will stay ahead of the Fed, or risk a higher NZD/USD.

The Fed’s change in language caused a sharp fall in US interest rates overnight. The rate on the US 2-year Treasury bond fell 13bps to 1.73% (compared to 1.13% in NZ), while the 10-year fell 4bps to 2.03% (compared to 1.55% in NZ).

The reaction in markets to the Kiwi GDP report was muted. The 2-year swap rate (used by banks to hedge 2-year fixed rate mortgages) is basically unchanged at 1.325%. The Kiwi currency lifted to 0.655 from 0.6537 prior to the release.

Following the RBNZ’s OCR statement in March we raised the probability of RBNZ rate cuts, not just to 1.25%, but to 0.75%. We showed how a market, entertaining the risk of such moves, will lower wholesale rates. We had forecast the 2-year swap rate to hit 1.3%, and the NZD to hit 65c and glide lower to 61c later in the year. See Blood, Sugar, Brex-Magik: markets high on risk. Markets has moved swiftly, and look adequately priced for now. The current 2-year swap rate of 1.325% looks fair for now, but the risk is lower, not higher. The Kiwi dollar has hit a recent low of 0.6482. The NZD looks set to push towards 61c on the whiff of weaker news offshore. And the Kiwi dollar should get another leg down with an RBNZ rate cut in August. Lower wholesale and retail lending rates should help investment. But we worry about the impact on savers. The weaker currency is what we need, but other central banks are now in cutting mode, also. What’s needed to truly lift our potential growth and outlook? Fiscal investment is needed to support growth from here.

Following the RBNZ’s OCR statement in March we raised the probability of RBNZ rate cuts, not just to 1.25%, but to 0.75%. We showed how a market, entertaining the risk of such moves, will lower wholesale rates. We had forecast the 2-year swap rate to hit 1.3%, and the NZD to hit 65c and glide lower to 61c later in the year. See Blood, Sugar, Brex-Magik: markets high on risk. Markets has moved swiftly, and look adequately priced for now. The current 2-year swap rate of 1.325% looks fair for now, but the risk is lower, not higher. The Kiwi dollar has hit a recent low of 0.6482. The NZD looks set to push towards 61c on the whiff of weaker news offshore. And the Kiwi dollar should get another leg down with an RBNZ rate cut in August. Lower wholesale and retail lending rates should help investment. But we worry about the impact on savers. The weaker currency is what we need, but other central banks are now in cutting mode, also. What’s needed to truly lift our potential growth and outlook? Fiscal investment is needed to support growth from here.