- Kiwi house prices bounced back into the black, according to REINZ. House prices rose 0.4% in June, with signs of further strength to come. The true litmus test for the housing market will be in spring. And we expect to see an uplift in confidence and activity.

- House prices are down 17.7% from the November 2021 peak. The rampant rise in interest rates restrained demand – by RBNZ design. It appears that most, if not all, of this correction has played out.

- Our forecast peak to trough correction of ~20%, may prove to be a bit pessimistic. The peak in interest rates will mark the bottom of the downturn. And rate cuts will support the rebound. Migration is also surging.

The true litmus test is to come.

Kiwi house prices rose in the month of June. Since the peak in November 2021, we have recorded just 4 monthly gains out of 19, (so that’s 15 contractions). National house prices have fallen 17.7% from the peak. But this followed a 47% gain in the 18 months to November 2021. The extraordinary gains over 2020-21 prompted an aggressive response from the RBNZ. Interest rates have been ratcheted higher, and prices have dropped to more “sustainable” levels. We think that the correction for past excesses has largely run its course. Our forecast peak to trough correction of ~20%, may prove to be a bit pessimistic. The peak in interest rates will mark the bottom of the downturn. And rate cuts will support the rebound. Migration is also surging, adding demand.

Auckland recorded a tentative gain of 0.8% over the month, following some hefty falls over the last two years. Excluding Auckland, house prices are down 14% from the peak. We could also exclude Wellington, but they’d complain. House prices in the Capital have recorded the sharpest falls, down 24% from the peak (Auckland has recorded a fall of 22.5%). But prices lifted 1.15% in June, potentially marking the end of declines in the capital. House prices in Canterbury fell a little further in June, down 0.8%mom, but are only down 8.6% peak to trough. The South Island has outperformed the North during this downturn. But we suspect Auckland and Wellington will lead the recovery into 2024 and beyond.

It looks like the regions are still playing catch up to Auckland and Wellington. There were mixed gains and losses across the regions, but green shoots are emerging.

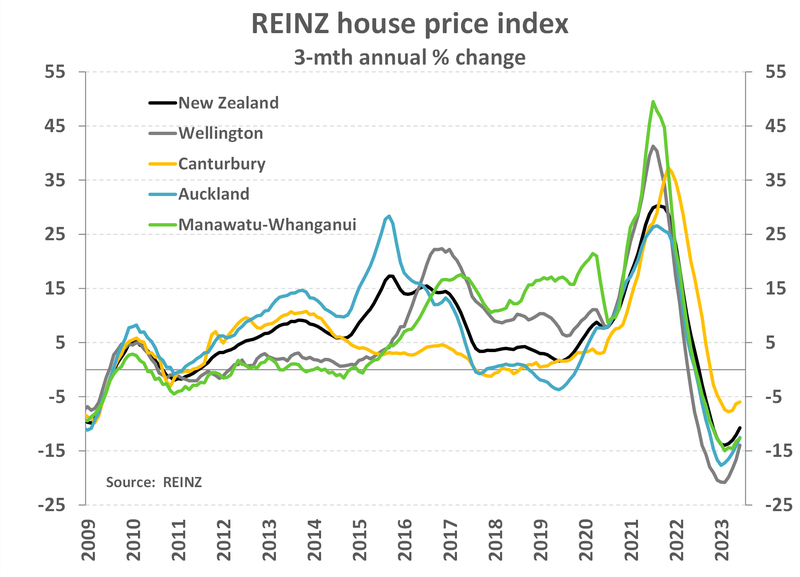

Our first chart shows the annual rates of house price declines are heading north. It’s a good sign.

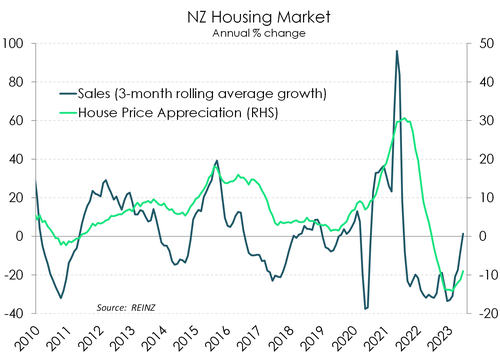

The month of June is a seasonally slow one in the housing market. We’d rather show off our houses in the sunshine. But there was a material gain in sales over the year. House sales are up 15% on last year (and +17% excluding Auckland). “Salespeople across the country are reporting increased first home buyer activity at open homes, with the easing of LVR restrictions that came into effect on 1 June bringing more people out looking. Although activity has increased, caution remains as interest rates, a pending election and further strain caused by the cost-of-living tempers putting pen on paper,” Jen Baird, REINZ Chief Executive

The month of June is a seasonally slow one in the housing market. We’d rather show off our houses in the sunshine. But there was a material gain in sales over the year. House sales are up 15% on last year (and +17% excluding Auckland). “Salespeople across the country are reporting increased first home buyer activity at open homes, with the easing of LVR restrictions that came into effect on 1 June bringing more people out looking. Although activity has increased, caution remains as interest rates, a pending election and further strain caused by the cost-of-living tempers putting pen on paper,” Jen Baird, REINZ Chief Executive

Despite the stabilisation in prices and solid activity, the days to sell reflects a buyers market. The number of days it takes to sell remain frustratingly long at 49, compared to a long-term average of 39. We expect the days to sell to remain awkwardly long over winter, before speeding up in spring.

The true litmus test for the housing market will be made in spring. Confidence in the market is better gauged over the warmer months. We expect interest rates to fall later this year, net migration is surging back, and there’s still a shortage of dwellings. We expect the housing market to bottom over the second half of this year, and we should see some slight gains next year.

A rebound is underway.

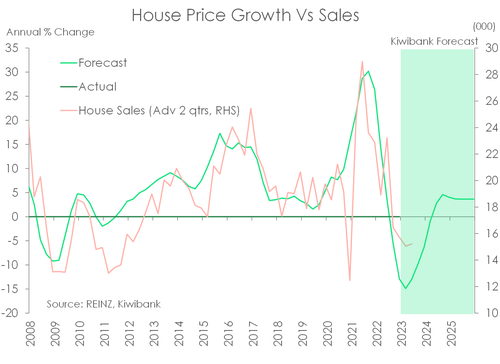

There are three drivers of the housing market. Firstly, falling mortgage rates will support confidence and activity. Although mortgage rates have risen recently, we expect to see falls in mortgage rates into year end. Secondly, the demand/supply imbalance will worsen. The surge in migration and the loss of dwellings at high risk of climate change will only exacerbate the housing shortage. And finally, the residential construction boom is coming to an end. The number of dwellings coming to market will fall back from very high levels. The growth in demand, with a migration boom, will once again outstrip supply in coming years. All three drivers point to a strengthening housing market, and price gains. We see a return to monthly house

There are three drivers of the housing market. Firstly, falling mortgage rates will support confidence and activity. Although mortgage rates have risen recently, we expect to see falls in mortgage rates into year end. Secondly, the demand/supply imbalance will worsen. The surge in migration and the loss of dwellings at high risk of climate change will only exacerbate the housing shortage. And finally, the residential construction boom is coming to an end. The number of dwellings coming to market will fall back from very high levels. The growth in demand, with a migration boom, will once again outstrip supply in coming years. All three drivers point to a strengthening housing market, and price gains. We see a return to monthly house

price gains – albeit very modest gains – beginning from the second half of the year. We forecast annual gains creeping up to 2% by the first quarter of 2024, before hitting a high of 6% by the middle of the year.

Interest rates should fall.

We think the time will come, sooner rather than later, for interest rate cuts. As we outlined in “Are we the waiting: the RBNZ’s prolonged pause will turn to rate cuts, eventually. Interest rates should fall.”If the economy develops in a way we expect, then the RBNZ will start easing early next year. That’s an important message for Kiwi households and businesses. We may have reached the peak in lending rates. And as with all peaks, we will come down the other side. Tailwinds are coming.