- The housing market continues to pay for past excesses. A lack of demand in the market saw 40% fewer house sales than a year ago – the biggest annual fall recorded in 2022.

- The REINZ House Price Index slipped further and was 13.7% down on last November’s covid-era peak in prices.

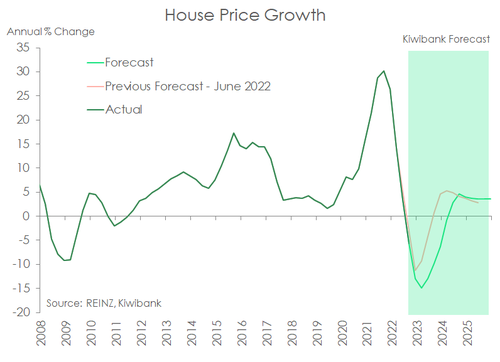

- As noted in our latest outlook note, we now expect house prices to fall further. Mortgage rates have taken a leg higher following last month’s RBNZ MPS, and we are picking annual house price falls to reach 15% in the first quarter of 2023. From peak to trough house prices are expected to fall a little over 20%.

The Market lacks energy.

The typically energetic month of November was far from buoyant in 2022 according to the latest report from REINZ. Sales may have climbed 7.7% in the month, but when accounting for the usual seasonal uplift, sales were in fact down 4.1%. Compared to a year ago, when activity was already trending lower, sales were almost 40% down this November. But last year’s slowing activity was more a case of tight supply around the country. This year, even weaker sales is due to a clear lack of demand, brought on by far tighter credit conditions. And properties are taking much longer to sell. The median number of days to sell across Aotearoa was unchanged at 47 days seasonally adjusted, that’s tracking well above the long-run average of 39 days.

Disappointing sales activity translated into further falls in house prices. The REINZ house price index (HPI) is 13.7% down compared to November last year – another record fall. And last November happens to be the covid-era peak in prices. As we published last week in our latest outlook note, house prices have further to fall. Following the RBNZ’s MPS we updated our view and now see the cash rate reach 5.50% by mid next year. The RBNZ looks determined to hike until it hurts to get inflation back into the RBNZ’s target box. The higher cash rate outlook has already seen mortgage rates take another leg higher and are likely to move higher next year.

From a 13% annual fall in the December quarter, we are now forecasting a trough in annual falls of 15% in the first quarter of 2023. Our forecast suggests a peak to trough fall in house prices of 21% in the current correction. Overall, the sharp fall in prices is in part payback for the excesses in the market of 2020 and 2021. The correction in the housing market to date hasn’t felt as bad as the record house price falls and weak activity might suggest. The labour market has remained incredibly tight this year and has helped to ensure mortgage holders have serviced mortgages and tenants pay the rent. As a consequence, the level of non-performing loans has barely registered so far.

However, 2023 could be a different story. We are predicting a recession brought about by aggressive monetary policy tightening. Around 20% of mortgages are re-fixing heading into 2023, and another 50% over the coming year. Many mortgage holders will be moving from a 2-2.5% rate to 6-7%. There are clear risks on the housing market from a potential overtightening in policy. For now, we are forecasting a steady rise in the unemployment rate over 2023, but not as aggressive as might be expected compared to past recessions. A recovery in the market appears a long way off. However, on the demand side net migration is turning around quickly and will see population growth pick up.

The extremities of the country outperform.

While the largest centres in the North Island are experiencing the deepest correction, the extremities of Aotearoa are experiencing a far softer slowdown. For instance, Northland recorded the first annual fall in the HPI in November since 2014 of 4.9%. At the other end of the country Southland has just recorded its first annual decline in house prices since 2015, at a more modest 2.2% fall. Moreover, the median house price at the bottom of the country popped back up to the all-time high of $475k. Nevertheless, even our apparently strongest markets are cooling, and may be playing catch-up to the larger centres. The median number of days to sell a house in Northland jumped 12days to 60 in November – the highest since mid-2020. And sales in both regions are 20-30% down on a year ago.

Auckland and Wellington have been punished the most so far in the current correction. REINZ recorded 18.4% and 19.5% annual falls in the HPI respectively. However, other regions such as the Waikato and Bay of Plenty appear to be catching up. The BoP for instance recorded a double-digit annual house price fall (11.6%) in November.