- We have received some good news on inflation. Inflation has peaked, globally. We are simply importing less inflation. This is great news. The world war on inflation is being won, albeit slowly.

- Imported inflation eased from 6.4% to 5.2%. That was the pleasant surprise. Petrol prices are down 15% on the year (they will bounce). And the outlook for global prices continues to improve.

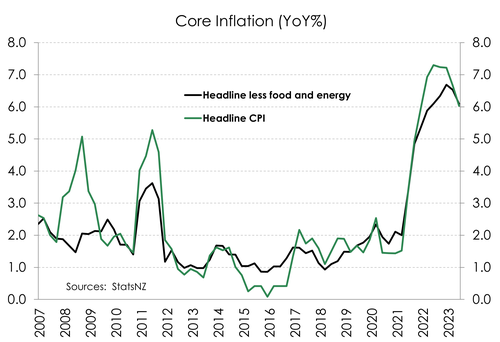

- Domestically generated inflation, esp. construction related prices, remains sticky, and fell from 6.8% to 6.6%. Core measures of inflation, which strip out volatile stuff, came in lower at 6.1%, down from 6.5%. This is a positive shift lower.

- We’re confident we’ve seen the peak in inflation, with the annual rate comfortably below the 7.3% peak at 6.0%. The peak in inflation will mark the peak in interest rates, locally and abroad.

Today’s inflation print was good news. It came in bang in line with our forecast (6.0%), but was slightly higher than consensus (5.9%). It’s worth remembering that the peak in inflation was a whopping 7.3% one year ago. The war in Ukraine sparked a sharp spike in commodity prices. Base effects are now helping. Psychologically, the shift from the 7s to the low 6s is helpful. Although it would have been great to see a 5-handle. Inflation expectations, with the RBNZ’s survey to be completed this week, will fall further -reinforcing the downward momentum. We’re on track to fall back within the RBNZ’s target band early next year.

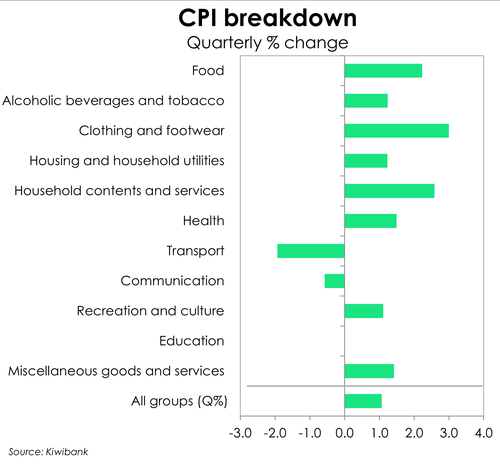

When we slice and dice the data, it’s what we do and love, we see some markedly mixed moves. Prices have risen pretty much across the board. The percentage of goods in the basket recording increases, rose. Food and housing prices recorded the largest gains. And they hurt the most households. Construction-related costs eased to 7.8%yoy (still hot) down from 11% (near boiling). Construction costs will continue to decline, sharply, as the housing market cools. Transport related prices helped, falling 2% over the quarter. International airfares were down a massive 12% on the quarter. And petrol prices were down, before the excise tax was put back on in full from July 1st. We’ll see a bit of a bump in petrol prices in the current, 3rd quarter.

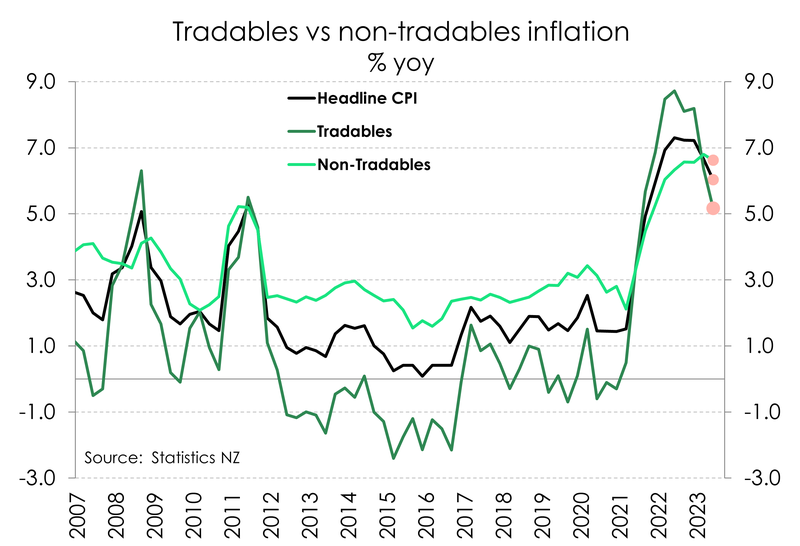

We do like to look at tradables (imported) versus non-tradables (domestic) prices. Half of the inflation we’ve experienced has been imported. And tradables is moving exactly as we had hoped, down to 5.2% from 6.4%, and a peak of 8.7%. Tradables will fall fast from here. But it’s largely outside the RBNZ’s control. The RBNZ has more of a focus on non-tradables (domestically generated) inflation, over which it has influence. Non-tradables inflation fell from 6.8% (the peak) to 6.6%. It’s still a long way back beneath 3%.

Core measures of inflation – that’s economist speak for taking out the stuff we don’t like, like volatile food and energy prices, fell. Core inflation dropped from 6.5% to 6.1%. It’s a significant move in the right direction. But it’s still a long way back beneath 3%. The RBNZ targets 1-3%.

The RBNZ will take comfort in today’s report. The RBNZ had forecast an easing in price pressures to 6.1% - so pretty much in-line. It’s good to see the key indicator moving in the right direction. And most of the other indicators have come in softer than the RBNZ had forecast. There’s no need to tighten further. We expect the RBNZ to sit tight for the remainder of the year. Monetary policy operates with a lag, and we’re yet to see the full impact of past actions on today’s economy. For example: around 40% of all outstanding mortgages roll off their (low) fixed rates, and onto much higher rates, over the next 6 months. That’s pain. And that’s going to impact discretionary spend.

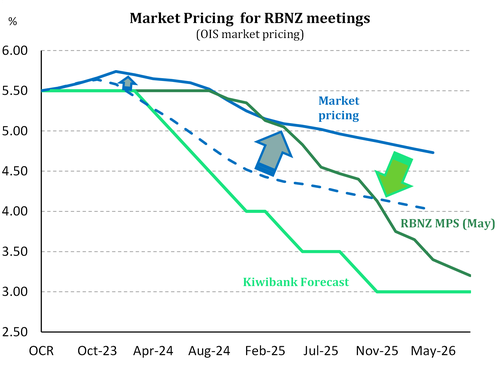

We expect the next move from the RBNZ will be a rate cut. And we’ve pencilled in a move in February. By then, we are likely to be in the middle of a mild recession. A recession engineered by the RBNZ, to tame inflation.

Basket breakdown: broad-based gains, still.

Food and housing-related inflation were again the main drivers of the lift in consumer prices. And price gains are still relatively broad-based. Well over half of all items in the CPI basket recorded a lift in prices. In fact, that proportion grew over the quarter to 68%, from 63% - albeit smaller than the 72% peak.

Food was at the helm of the lift in consumer prices, adding 0.5%pts to the headline rate. Adverse weather conditions earlier this year have resulted in double-digit increases in prices for food, especially fresh produce, up over 20%. Over the quarter, fruit and veg experienced some deflation, down 0.2%, most likely payback for the 9.5% increase over March. More than offsetting the fall, was the 2.7% and 3% increases in grocery food and restaurant meals.

The price impact of the Cyclone and weather events extended beyond food. Insurance premiums spiked in the aftermath. Over the quarter, home insurance and contents insurance rose 5.8% and 6.3%, respectively. Higher risk areas were hit harder, with even higher premiums. We expect to see this re-pricing of insurance (esp. in high risk areas) continue, and become even more targeted. Some houses may become uninsurable. That’s a discussion for another day. But it’s inflationary and will remove housing stock.

Housing-related inflation eased from 7.1% to 6.0%. It’s a decent move lower, helped mainly by cooling construction costs. The home ownership price index, which includes house construction, matched last quarter’s 1.1% gain. However, on an annual basis, costs eased steeply from 11.1%yoy to 7.8%. It’s a material slowdown from the 18% peak recorded late in 2021. Construction costs surged over the past few years with acute shortages in material and labour. But supply chain pressures are easing, shipping costs are falling, and more labour is coming with a surge in migration. In addition, rising mortgage rates and the housing market correction continues to weigh on the building sector.

The slowdown in housing inflation is encouraging. Especially given that it is the largest and most persistent driver of non-tradables inflation. However a 6% rate is still quite heated. And rental price inflation stubbornly stuck at ~4% is keeping it elevated.

There was surprising strength in retail goods. Prices for clothing and footwear rose 3% over the quarter and prices for home contents & furnishings rebounded 2.6% rise. We suspect that further price gains are limited. There are encouraging signs that the costs experienced by firms continues to ease. According to NZIER’s business confidence survey (QSBO, see here), both experienced and expected costs fell back. And a shrinking share of firms expect to raise their prices in the next quarter (Q3). In addition, inventory levels that have expanded over the last few years will need clearing. But at a time when firms are facing softening consumer demand for durable goods. We could see some discounting going forward.

Providing some offset was the fall in the transport group. Over the quarter, a 12% decline in international airfares led the quarterly drop. Although, this may also be a case of payback. Stretched air travel capacity and strong demand for travel saw double-digit spikes in airfares. But that’s beginning to normalise. Outside of the pandemic, that’s the largest fall since the March quarter in 2018. Annually, transport prices are down 0.7%, led by a 15% drop in petrol prices. Global oil prices spiked early last year following the Russia-Ukraine war. Since then, commodity prices have come under pressure with softening global demand and China’s stalling post-Covid recovery.

The data predates the reintroduction of the full fuel excise tax and return to full public transport fares (for those aged 25 years and older), from July 1. Higher public transport fares will have marginal impact on overall inflation, given its relatively small weighting in the CPI basket. It’s petrol prices that’s of greater interest. Petrol alone has a weight of almost 5% in the CPI basket (so we spend about 5% of our hard-earned cash on petrol. Lower-income households spend a far greater proportion). We may see a stronger lift in inflation over the September quarter, with higher petrol prices. But it won’t be enough to lift the annual rate. We’re likely to see a continued deceleration in inflation, but possibly at a slower pace.

Underlying price pressures are easing.

The underlying trend in inflation remains uncomfortably strong but appears to be easing. Key measures confirmed that inflation is past its peak – a development that has been repeated in other developed countries. For instance, the trimmed-mean measures of inflation (exclude volatile price movements), eased further in the June quarter. On an annual basis, trimmed-mean measures fell to between 5.7% and 6%, down from 5.9% and 6.1%. Headline inflation less food, household energy and fuel posted another 0.9% gain, same as the last quarter. The annual measure fell markedly to 6.1% from 6.5%, and now sitting comfortably below the 6.7% peak.

Sit tight. No more rate hikes are needed.

Inflation is moving in the right direction. By year-end we see headline inflation decelerating to 4%. Favourable base effects are in play with last year’s spike in energy and food prices falling out of annual calculations. Cooling commodity prices will also help to lower the cost of imports. And a stalling post-Covid recovery in China will also weigh on imported inflation. Inflation in China is currently just 0%, having fallen from 2.8% last year. So we’re unlikely to import a lot of inflation from our largest trading partner.

Here in Aotearoa, the tricky task is getting back to the RBNZ’s 2% target. A task that hinges on the projected path for domestic inflation – the stickier, demand-driven kind. And a task made difficult by the ongoing strength in wage growth.

We expect the RBNZ to sit tight for the remainder of the year. The RBNZ signalled 5.5% as the peak in the cash rate, with a “very, very high bar” for further increases. We expect no more. The data to date has been weak. And the data to come will also be weak. Signs of an imminent slowdown in economic growth are already surfacing. Firms are pessimistic about future trading activity and households are pulling back on discretionary spending. The RBNZ will also take comfort in today’s report confirming that inflation is on the way down. There’s no need to tighten further. Monetary policy operates with long lags, and we’re yet to see the full impact of past actions on today’s economy.

Violent market moves may be pacified by year-end.

Today’s CPI report card was welcomed by traders. There was a collective sigh of relief. But we still got some action. Financial market traders took the report as being slightly worse than expectations. The consensus among economists was for 5.9% (not 6%). It’s not a big difference. But we saw some old-fashioned punting during the release. There was a bit of funky business in currency markets. We saw the Kiwi dollar driven higher in the few minutes before the release. Someone took a bet. It almost looked like the data was released early. The Kiwi jumped from 62.73 to 63.15, most of the move happened just before the release. And the bird has settled around 62.97, at time of writing. So the Kiwi flyer is higher, but not by much. The same can be said about the rates markets, without the funky trades pre-release. The 2-year swap rate lifted from 5.35% to 5.44%, to settle at 5.4%.

We have seen an extremely volatile wholesale rates market in recent weeks. There have been many market moving events. But it was the illiquidity in a market where the local banks were all facing the same way, and forced to pay.

It wasn’t that long ago, when we had Kiwi rates markets factoring in a peak in the terminal rate around 5.5% (exactly where it should be), and rate cuts commencing from February (exactly our view). The 2 year swap rate was below 5%. Unfortunately, it was not meant to be. Even though we had to agree.

Two weeks ago, we saw a dramatic push higher in rates. The 2-year swap rate lifted to a high of 5.75%. That’s a massive move from the recent low of 4.92%, and a sharp move from the 5.15% at the start of June. The market moved rapidly to price in a terminal rate of 5.75% (reflecting the view of some other commentators. We disagree), and thoughts of rate cuts were pushed deep into 2024 (cuts were pushed from February to October 24).

The dramatic surge in wholesale rates forced local banks to adjust their fixed rates, on mortgages and business, higher.

The sharp move higher in rates was exacerbated by a market caught one way. Banks use wholesale swap rates to price (hedge)

retail mortgage and business lending rates. You want a 2-year fixed rate, we pay the 2-year swap rate. It’s all about locking in the spread between the two, on the two. Paying the 2-year swap rate means we pay the fixed leg of the swap, while we’re receiving a fixed rate on the mortgage. All banks do the same thing, on the same mortgage flow. And all banks were facing the same way, at the same time, and at a time when other market participants (fund managers, hedge funds etc…) stepped away. Unfortunately, this is not unusual. And it’s easy to foresee. [Pay side pressure pushes swap rates higher.]

We have flagged the risk of market illiquidity, on numerous occasions over the years, as banks are forced to hedge large lumpy flow. And we are likely to see it again in spring and summer. There will be periods over the busy warmer months where banks will be forced to fix mortgage flow. Remember, 40% of outstanding mortgages come off fixed rates over the next 6 months – with some chunky flows over September to November.