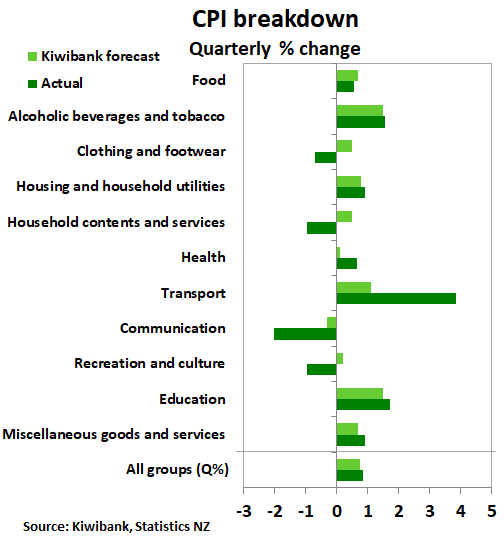

- Inflation jumped 0.8% in the first quarter of 2021, driven by higher transport- and housing-related costs. Petrol at the pump jumped, and rents rose as the rent freeze came to an end.

- At 1.5% the annual rate of inflation held under the RBNZ’s target for now. We’re picking inflation to jump towards 2.5% in the June quarter. But current inflationary pressures should prove transitory.

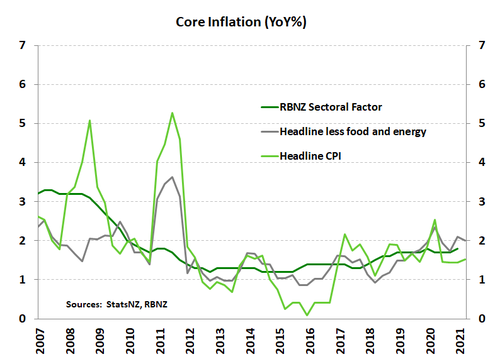

- Strip away the volatility and core inflation remains subdued, The economy is not yet strong enough to generate a sustained lift in prices. The RBNZ should try to look through temporary shocks and disruption

Today’s inflation report came out bang in line with our estimate of 0.8%. Transport rose 4% over the quarter, the greatest gain in a decade. Fuel rose 7% and the cost of used cars bounced back strongly. Construction costs rose a hefty 1.2% with supply shortages (like timber) eating into profits and labour costs rises with border restrictions.

Rents rose 1% on the quarter, following the rents freeze last year. The gain predates the Government’s announcement to remove interest deductibility on investment property.

Food prices rose a modest 0.6% in the quarter, lifted by higher prices for restaurant meals and higher dairy commodity prices. Prices for fruits and vege were little changed. Given rising global food commodity prices, we expect a slight pick-up in food price inflation over the coming quarters.

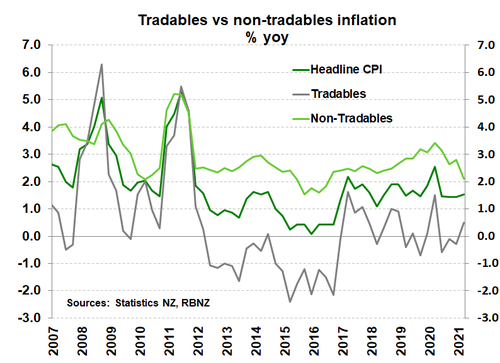

Housing-related inflation pushed up non-tradables - the domestically generated inflation - to 2.1%yoy. But because of the more modest increase in tobacco prices this year, the annual rate is down from 2.8% in the year to December 2020. Tradable inflation – imported inflation – rose 0.5%, with higher prices for used car and international air transport offset by lower annual prices for petrol.

The March quarter also captured the back-to-school bonanza, which saw some discounting for consumer electronics. The WFH movement may also be at work here. Kiwibank’s own card spend data shows that demand for office equipment rose in January as many geared up for a new year of a new way of working.

The 0.8% quarterly gain was slightly below the RBNZ’s estimate of 1%. There was nothing in today’s report the RBNZ would be surprised by, or even react to. They need to see how inflation is tracking this time next year, after the supply disruptions have washed through. Bottlenecks at our ports will eventually be addressed.

Strip away the volatility and core inflation remains subdued, easing from 2.1% to 2.0%. The economy is not yet strong enough to generate a sustained lift in prices. When setting monetary policy, central banks look to the medium term, and try to look through temporary shocks and disruption.

The usual suspects drive prices higher

As usual, transport and housing related costs drove the quarterly rise in prices. Transport lifted 3.9% in the March quarter alone, the biggest rise in over a decade. Pushing prices higher was a pick-up in petrol prices at the pump. Global oil prices have been on the rise in recent months, which saw petrol rise around 7% in the quarter. Used cars were also more expensive, as the inability to travel overseas boost demand, coupled with relatively tight supply

Housing-related inflation was another major contributor to headline inflation. The jump in demand combined with an ongoing shortage of housing led the price of new home construction up 1.2%qoq. The cost pressures of supply shortages are starting to be felt by the construction sector. The difficulty in obtaining timber and house fittings and furnishings are lifting production costs. Add to that higher labour costs given the small pool of workers.. Until the border opens, these price pressures on construction will likely remain.

Rents also lifted another 1% following the Government’s rent freeze last year. Annually, rents are up almost 3% up on last year. Although any impact that the Government’s removal of interest deducibility might have on rents will be a story for the coming quarters.

Housing-related inflation pushed up non-tradables - the domestically generated inflation - to 2.1%yoy. But because of the more modest increase in tobacco prices this year, the annual rate is down from 2.8% in the year to December 2020. Tradable inflation – imported inflation – rose 0.5%, with higher prices for used car and international air transport offset by lower annual prices for petrol.

Housing-related inflation pushed up non-tradables - the domestically generated inflation - to 2.1%yoy. But because of the more modest increase in tobacco prices this year, the annual rate is down from 2.8% in the year to December 2020. Tradable inflation – imported inflation – rose 0.5%, with higher prices for used car and international air transport offset by lower annual prices for petrol.

Core inflation cools

Annual core inflation was notably softer at the start of 2021. StatsNZ’s trimmed-means measures, which remove volatile price movements, fell across the board back below the RBNZ’s 2% target midpoint. Looking at headline inflation less the volatile food group, fuel and household energy prices, it eased a touch to 2%. The core inflation results suggest that once recent and temporary inflation works its way through the numbers, headline inflation will return to a weaker trajectory.

The RBNZ will this afternoon at 3pm release its own core inflation measure, the sectoral factor model, which is also likely to reveal better behaved underlying price increases.

Sandy shores, not concrete floors

Beyond the first quarter, we expect annual headline inflation to overshoot the 2% target. A combination of factors is in play. Ongoing supply chain disruptions, capacity constraints and strong commodity prices are driving production costs higher. Consumer prices are set to take off as firms intend to pass-through these rising costs. Annual figures in the next (June) quarter will be especially strong due to base effects of a weak quarter last year when prices fell. It is likely we see inflation spiking to 2.5%yoy.

After years of underachieving target, this is not an entirely bad thing. Lifting inflation closer to target has been the bane of many central bank governors since the 2008 crisis. These present price pressures should prove transitory. Bottlenecks at our ports will eventually be addressed. The risk of deflation has certainly receded, but strip away the volatility and the long-term outlook for core inflation remains subdued. The economy is not yet strong enough to generate a sustained lift in prices. And tectonic forces pushing prices down, including demographics and technology, remain in play.

When setting monetary policy, the RBNZ should look through the rise, just like every other central bank. In the latest policy review, the RBNZ reiterated that it will take “considerable time and patience” to meet their mandates. Based on our forecasts, the return to full employment and stable inflation (2%) will take two years to achieve with confidence, and that’s without further shocks. Monetary policy is likely to remain unchanged well into 2022.

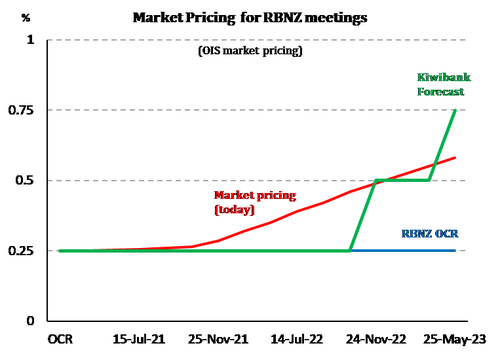

We deem financial markets to be perfectly priced. The first RBNZ rate hike is priced by November 2022, bang on our forecast. And the curve glides higher thereafter, with another hike by the middle of 2023. It’s a long way out, and much will happen between now and then. But in terms of financial market positioning, we see no reason to push against it.

Market reaction

The reaction in financial markets was muted. Because markets are near perfectly priced in our opinion. Wholesale interest rates are likely to hold in current tight ranges, for some time. And the Kiwi currency is likely to drift higher, back towards 75c in time. For more on the RBNZ outlook, and financial market pricing, see: Persuasion: RBNZ pacifies pundits with markets perfectly priced.