Key Points

- The RBNZ left the OCR on hold at 1.75% as widely expected, and brought forward the timing for OCR increases by one quarter.

- The RBNZ’s forecasts included four areas of the new Government’s policies, including increased spending, residential building, immigration policy and increases in the minimum wage.

- There remains significantly uncertainty around the outlook for domestic inflation, and we expect non-tradable inflation to strengthen faster than the RBNZ is forecasting.

- We maintain our view that the RBNZ will leave the OCR unchanged until the end of 2018, before gradually hiking interest rates.

Summary

The RBNZ left the OCR on hold this morning at 1.75% as widely expected. The Bank delivered a slightly more upbeat Monetary Policy Statement (MPS), with a stronger near-term inflation outlook. In addition, the RBNZ moved forward its forecast timing for OCR increases by one quarter - from Q3 2019 to Q2 2019 - and had a slightly higher end point for its OCR track of 2.3%. Also of note was a change in the underlying growth drivers for the economy. Both consumption and residential investment are expected to provide less of a boost to growth, but these are offset more stimulatory fiscal policy and an elevated terms of trade.

The Bank highlighted that there remains considerable uncertainty around the domestic outlook, but our view is a bit more positive on some fronts compared with the RBNZ’s. With headline inflation now running at close to 2%, and capacity and wage pressures increasing, we expect to see non-tradables inflation in the economy pick up at a faster pace than the Bank’s forecasts suggest. In addition, we anticipate that net migration will remain elevated for some time, and the changing composition of migrants will start to have a more stimulatory impact on inflation pressure. As such, we maintain our view for OCR hikes to begin from late 2018.

Of note, Governor Spencer commented in the accompanying press conference that the move to a dual mandate (proposed under the RBNZ Act reform) is unlikely to have a material impact on monetary policy. Given the tightness in the labour market, Spencer implied that if a dual mandate was introduced immediately then it wouldn’t materially change the outlook for monetary policy in NZ.

Growth and government

The Bank’s growth forecasts were more muted in the near term compared with the August MPS, but still have growth rising to an annual pace of 3.8% yoy by early 2018 and holding at that level through next year. Relative to the RBNZ’s August forecasts, growth now remains at an average pace of around 3% yoy into 2020 – extending out the current business cycle. At least in part this appears due to the anticipated boost from higher fiscal spending under the new government, with an additional 0.5%pts expected to be added to GDP growth from fiscal policy. The Bank has incorporated four areas of the new government’s policies into its forecasts, including “increased government spending; the Government’s housing programme; changes to requirements for work and study visas; and increases to the minimum wage”. The RBNZ noted that there remains considerable uncertainty around the outlook for these policies and the path of implementation.

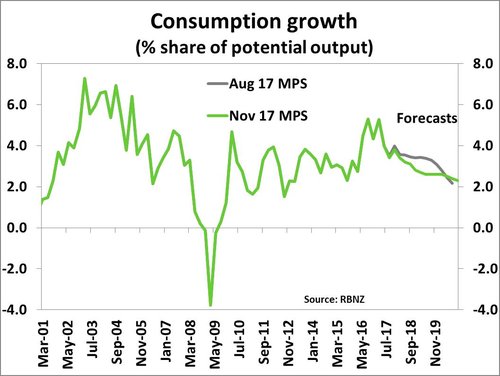

While increased government spending and investment have boosted the growth outlook, other areas of the economy are shaping up a slightly weaker. A more gradual profile for residential investment and moderate house prices gains (see below for details), combined with slightly lower population growth, has seen the RBNZ revise down its outlook for consumption growth.

The terms of trade is expected to remain elevated around current record-high levels, supporting domestic growth. The Bank’s forecasts for whole milk powder (WMP) prices remains at US$3000/mt over the medium-term – which is close to the current price of US$2,852/mt recorded at Tuesday’s Global Dairy Trade auction. We see some downside risk to Fonterra’s current payout forecast of $6.75/kgms but the decline in the NZ dollar should help increase incomes by offsetting lower commodity prices. With less political uncertainty, we expect to see a rebound in business confidence and business investment should remain robust.

Housing outlook subdued

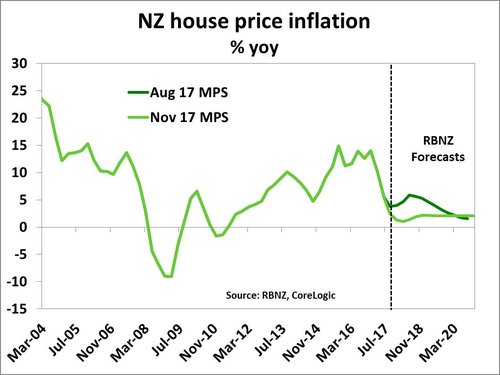

The outlook for the housing market in New Zealand remains uncertain and the RBNZ has pulled back its house price inflation forecasts relative to the August MPS. An underlying supply/demand imbalance remains but is being countered by “pressure on affordability, reduced demand from foreign buyers, uncertainty around tax policy, and revised expectations of future capital gains”. The RBNZ now expects to see annual house price inflation remain at around 2% yoy over the forecast horizon – very close to the current pace implied by REINZ data. In our view, we still expect to see a bit more of a rebound in price appreciation over the coming six months, but a similar price profile as the RBNZ through 2019 and 2020.

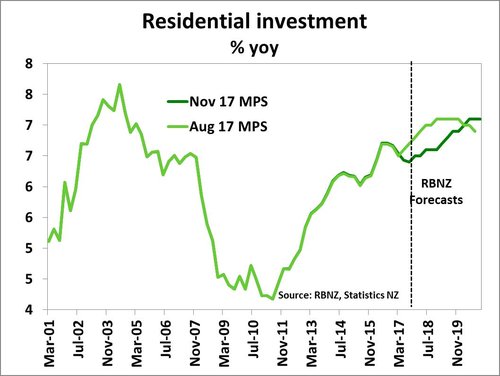

However, much of this will depend on credit conditions in the market, confidence, and the pace (and cost) at which residential construction work can be completed. The RBNZ highlighted the softening we have seen in the construction sector and has revised down its forecasts for residential investment growth in coming years – although it also has a more drawn-out investment profile over the forecast horizon. With strong demand for housing remaining, it looks like supply will now take longer to come on board given various constraints (access to credit, labour and materials). The RBNZ expects to see growth in the construction remain relatively flat over the rest of 2017 (see chart below), before picking up again in coming years – a view we agree with. The Bank’s business visits tied in with other business surveys highlighting that construction firms are facing a range of binding constraints such as labour shortages and availability of finance. The rising cost of development and construction has also seen margins squeezed, causing some projects to fall over – particularly in Auckland.

In line with our view, the Bank noted that there is a risk that public investment in residential building could cannibalise private sector investment – so the net effect on increasing dwelling supply won’t be additive. We have highlighted these concerns in a special housing note (available here). On migration, the Bank is assuming a steeper decline in net migration compared with its August MPS forecasts, although working age population growth is still expected to robust over the next few years (see below for details on migration).

In the press conference, Governor Spencer commented that they are currently reviewing the LVR restrictions and the conditions for their removal – with more details expected at the November FSR on November 29. Any removal of LVRs is expected to be have gradual withdrawal process - e.g. increasing the amount of lending allowed to those with less than a 20% deposit from 10% of all mortgage lending at present up to 15% and then over time up to 20%. The RBNZ showed a desire to still have debt-to-income (DTI) ratio restrictions added to its toolkit but wouldn’t use them in the current environment.

Migration expected to decline, but composition matters

The RBNZ noted that strong population growth has helped boost demand in the economy, but also raised the productive capacity –resulting in lower inflation than in previous net migration booms. The composition of migration matters in this regard. Up until now, this migration cycle has been driven largely by those in younger age cohorts – who tend to add to the labour force (thereby increasing capacity) but have lower consumption than older age groups. This has kept demand and supply in close balance. RBNZ Assistant Governor McDermott noted that the Bank is assuming that the supply/demand impulse from net migration is expected to continue to largely cancel each other out in terms of the inflation outlook. However, with the government’s proposed reduction in student visa numbers and unskilled workers, we expect to see a reduction in supply of workers and an increase in the age of the average migrant – boosting demand more than supply in coming years. If this occurs, then there is upside risk to the RBNZ’s current outlook for non-tradables and wage inflation.

RBNZ recognises stronger near-term inflation

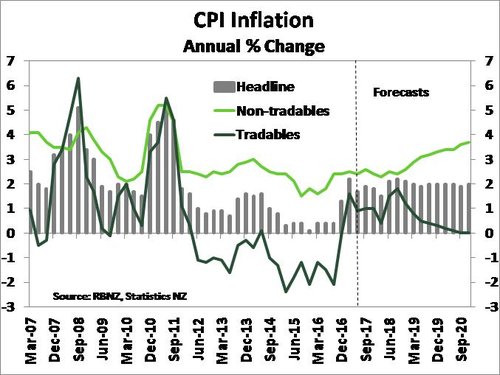

The RBNZ revised its CPI forecast higher in the near-term. The Bank now projects inflation to trough at a higher rate of 1.5% yoy in the March 2018 quarter compared to a 0.7% yoy low presented at the August MPS. In addition, inflation is now forecast to reach 2.1% yoy by the June quarter of 2018, whereas previously the Bank had inflation reaching 2% yoy by early 2019. While the Bank’s inflation forecast track has been revised up significantly in the near-term, thereafter CPI inflation is expected to quickly settle around the middle of the RBNZ’s 1-3% target band in 2019/20. We see a number of risks to the RBNZ’s inflation track, which will mean that the Bank will eventually bring forward OCR hikes to late 2018; these are discussed below.

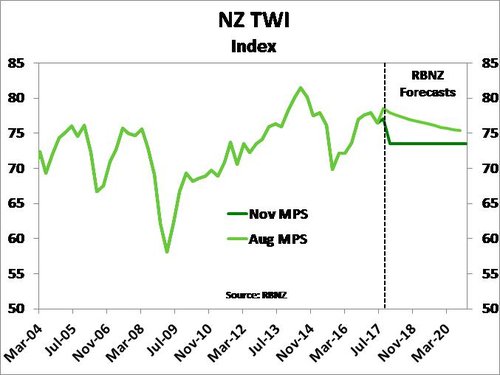

A key driver of the RBNZ’s upward revision is due to a sharp lift in tradables inflation in the near-term following the recent plunge in the NZ dollar. The TWI is currently close to 74, which is 6.5% lower than where it was in late July. The RBNZ’s forecast has been subsequently lowered and flat-lined at 73.5 over the forecast horizon (see chart below). The flat TWI track in part sees tradables inflation cool over the same period. In addition, the RBNZ pointed out that ongoing softness in global inflation will also see tradables inflation remain muted. In our view, a key upside risk to the RBNZ’s outlook for tradables inflation comes from a further sustained depreciation in the NZD. Globally, central banks continue to tighten monetary policy, albeit gradually, and are expected to continue to do so. With the RBNZ still signalling that interest rates will remain on hold into 2019, at the same time global policy tightens, there could be a further reduction in appetite for NZ dollar assets from offshore investors – weighing on the NZD. There is also upside risk around the Bank’s assumption concerning global inflation.

The RBNZ is forecasting non-tradables inflation will gather pace in the coming years, as capacity constraints build further, but less so compared to the Bank’s August MPS. A weaker starting point for GDP growth has meant that the economy’s output gap is likely to provide less momentum to domestic inflation in the near-term. However, we also see some upside risks to the Bank’s forecast of non-tradables inflation. For instance, capacity constraints could build faster than the RBNZ is currently forecasting. As noted above, changes to immigration policy present upside risks to non-tradables inflation in part by lowering the economy’s productive capacity. In addition, the Governments Kiwibuild programme adds significant demand to a building industry that is already under strain from private development and this raises the risk of costs escalating further. Another risk is the the Government’s proposal to increase the minimum wage to $20/hr by April 2021 is likely to have wider implications for wage inflation than simply for those on the minimum wage – which we believe will add to broader wage inflation pressure.

Putting all of this together, we expect to see CPI inflation print above the RBNZ’s own forecasts in the year ahead, necessitating an earlier monetary policy response than the Bank is currently signalling.

Market reaction

Following the release of the MPS, and the accompanying RBNZ press conference, the NZ dollar jumped half a cent to around $0.6970 before settling at close to $0.6950. Wholesale interest rates also increased following the MPS with the 2-year swap rate up a point to 2.20%, while the 5-year swap rate jumped 5pts to 2.69%. OIS market pricing was broadly unchanged today. The market is fully pricing in an OCR hike by February 2019, although the market is over 90% priced for a hike in November 2018.