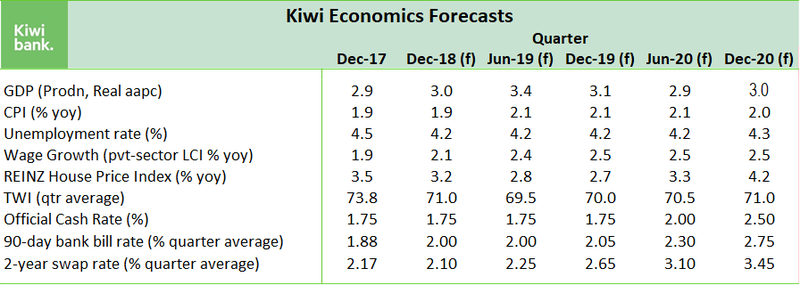

RBNZ show no hike until the end of 2020. We too push out our forecast rate hike from Aug’19 to May’20.

Down risks prevail

- The risks are asymmetric. The RB will keep the OCR at 1.75% “through 2019 and into 2020, longer than we projected in our May Statement.”

- The weaker OCR track has enabled a weaker Kiwi dollar forecast (TWI), but a frustrated inflation track. The RB is clearly cautious.

- “All signals are green for business investment”, but

- “The recent moderation in growth could last longer. Low business confidence can affect employment and investment decisions.”

Summary

The main message for the Reserve Bank was one of heightened uncertainty, as downside risks prevail. The Governor continued to deliver a positive feel during the media conference, but the numbers in the MPS are blatantly dovish. It’s time to watch, worry and wait.

Although economic growth is still forecast to run “above trend in 2019”, the “risks to the growth outlook are tilted to the downside”. The OCR track, the RB’s forecast of its own action, was delayed late into 2020. The lift-off point (in terms of probability) was delayed a year, from Sept’19 to Sept’20. The balance of risks have shifted enough over the last 3 months, to justify postponing rate hike calls. We too push out our expected lift-off into May’20, from Aug’19. The risk of rate moves over the next 12 months is weighted more towards cuts than hikes. And financial markets will price the risk of rate cuts accordingly. The good news here is interest rates and exchange rates will remain lower for much longer, assisting growth.

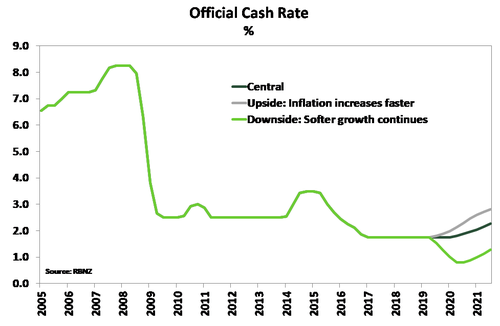

Global growth is still considered strong and the Government’s fiscal impulse will provide a boost. Employment is forecast to “remain strong, and stay near maximum sustainable employment”. The RB noted the “early signs of rising inflationary pressure”, but is willing to look through the upside risks, given the plethora of downside risks elsewhere. In the RB’s scenarios, the “upside” risk was around inflation, again, coming in stronger. The monetary policy response would be roughly +50bps compared to central. Whereas the “downside” risk around growth, again, coming in below trend, warrants cuts of -100bps. That’s asymmetry in risks and response.

Downside to our GDP forecasts are evident, but like the Bank we see enough in the economy to lift growth above trend in 2019 – and hence support a lift in domestic inflation pressure. We are still forecasting a much quicker return to the RBNZ’s 2% inflation target midpoint, with a solid rise in wages – the missing link in the Kiwi economy. And the financial market conditions are now being set in a way that should help the lift in inflation (and growth). Both Kiwi interest rates and the Kiwi dollar are lower, for longer.

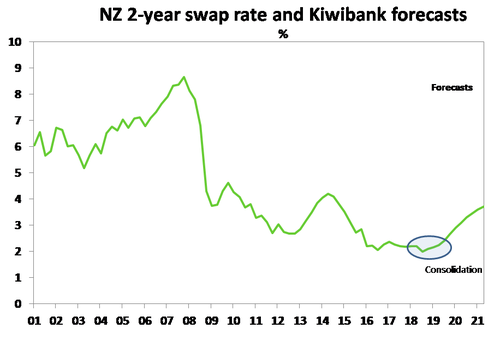

The big news here is the reaction is financial markets to the Dovish signals. The Kiwi dropped over 1% to $0.6680 against the Greenback. The 2-year swap rate dropped 6bps immediately, to ~2.055%, at time of writing. Orr noted he was “very pleased with the performance of the currency. It’s as close to fair value as it gets.” Along with our change in OCR forecast, pushing it out a few months, we have lowered or swap rate forecasts and Kiwi dollar forecasts.

The Kiwi looks like an endangered species, and we see the bird hitting 0.65c by year end (down from 69c previous forecast), and 63c in mid-2019 (down from 67c). So we forecast the Kiwi moving in the same direction, down, but now much lower. Our rate forecasts are also lower, and curve outlook steeper (despite today’s awkward move).

RBNZ looks through inflation drivers

Leading up to the August MPS the key developments were twofold and in our view offsetting. First, inflation was looking stronger, in part due to a decent and consistent rise in underlying measures of inflation and the emergence of cost-push factors. Second, GDP growth was softer with an outlook that is looking increasing uncertain on the back of downbeat business confidence.

On the inflation side, the RBNZ has looked through cost-push inflation drivers, such as higher oil prices, a minimum wage hike and Auckland regional fuel tax. We had expected the recent rise in inflation drivers would have a more sustained impact on CPI inflation. Firms have for a number of years now signalled an intention to raise prices but simply not followed through. The current environment feels increasingly like an opportunity for firms to pass on rising costs to consumers. However, of more concern for the Bank is the uncertainty around economic growth. March quarter GDP growth was weaker than the RBNZ had forecast back in May, and the recent cooling in business confidence suggests there is less capacity pressure in the economy. In our view, headline business confidence is currently exaggerating weakness in the economy. Nevertheless, firms’ own activity measures and investment intentions have pulled back - this can’t be ignored. But neither do these measures suggest the economy is about to fall out of bed.

The RBNZ’s CPI inflation track is broadly unchanged in the August MPS. Yes, the RBNZ lifted near-term inflation track, which sees CPI inflation reach 1.8% by the middle of next year. But inflation in not expected to return to the 2% target midpoint until the March quarter of 2021, a quarter later than the May MPS projections. The RBNZ revised its GDP growth track down in the near-term. However, growth is expected to pick up above trend from mid-2019 to 3.4% yoy, which will support a rise in domestic inflation.

Orr noted at the post release press conference that the “easing in house prices has been a welcome development” We published a note on Monday highlighting the challenges faced in Kiwi housing. Capacity constraints are our biggest problem, as we model a housing market with over 100,000 shortage in dwellings. See Kiwibank Property Insights. The Kiwibuild impact has been revised lower by the RB. The problems in the construction market suggest an inflationary issue in delivering the houses.

Lopsided scenarios underscore a dovish statement

A seam that ran through today’s statement was the Bank’s concerns around downside risks. This was illustrated by the main forecast scenarios included in the MPS. On the upside, the Bank noted the potential for stronger pass-through of cost increases to consumers. This would lead to a stronger-than-expected lift in non-tradables inflation and warrant hikes from late this year and an additional 50bps of hikes over the forecast period. However, there was a notable asymmetry in these scenarios with the Bank’s downside scenario, based on growth continuing to disappoint, would need a full 100bps of cuts to rectify. A cumulative cut of this size does seem at odds with expected GDP growth of the downside scenario. Growth remains around average over 2019 – so hardly a recession scenario requiring the RBNZ to expend its limited policy ammunition on. But the Bank clearly wants to look tough on inflation. They are likely to be encouraged by the recent strengthening in core inflation. Given inflation has been so low for so long, the RBNZ would be keen to prevent the possibility that the current embers of inflation get snuffed out.

Reinforcing the lopsided nature of the risks were comments made throughout the statement and the table of key judgments and risks. The economy: “The risks to the growth outlook are tilted to the downside”. The labour market: “A risk to this outlook is that GDP growth slows further, causing demand for labour to ease”. And where there is the potential for upside; inflation: “The risks around this inflation outlook are roughly balanced”.

The impact of a global trade war on New Zealand.

Adding to the downside theme, the RB discussed the impact of trade war. Every economic commentator, ourselves included, fears a full-blown trade war. And the RB notes it’s our “biggest downside risk”, globally. The likely impacts of announced tariffs to date, are “limited”. But it’s the escalation that scares us, and the RB:

“…if the conflict escalates, the impact on New Zealand would be more significant. The main impact of a trade war on New Zealand will likely be through direct trade channels and uncertainty effects. Around 20 percent of New Zealand’s exports go to China and around 10 percent go to the United States. There could be additional spillovers to New Zealand through other countries in Asia, which have close trading links with China. Lower commodity prices would weigh on New Zealand’s export earnings and could suppress tradables inflation. The impact of global supply chain disruption on New Zealand is likely to be limited, as New Zealand is less integrated into supply chains than economies in Asia.”

Market Reaction is parallel but should be steeper.

The financial market reaction was a little perplexing, but symptomatic of positioning, especially from offshore hedge funds. The 2-year swap rate dropped from 2.11% to 2.0425%, a good 7bps. But the 5-year (and 7-year) outperformed, shedding 11bps in yield. The 10-year even outperformed the 2s, dropping 9bps. Curves normally bull-steepen when cuts are being priced. Today’s reaction was fair, however, as traders took the Governor at his word – nothing for a very long time. We have shaved our interest rate forecasts, and see the 2-year hitting 2% in coming months, before slowing drifting higher over 2019.

The flying Kiwi nosedived against all crosses, with the TWI dropping to 72. We’ve revised our forecast easing in the TWI to 69.5 by mid 2019.

We see the bird hitting 0.65c by year end (down from 69c previous forecast), and 63c in mid-2019 (down from 67c).