- New Zealand’s housing market desperately needs an injection of affordable, sustainable homes. We’re short 80,000 homes. The Govt’s announcements today falls short. It’s merely a drop in the leaky bucket.

- The most effective measures announced today are aimed at demand. The Bright-line test will be extended from 5 years to 10, excluding existing investments (before March 27th) and new builds. The Govt has deliberately given a tax advantage on new builds, hopefully with interest deductibility.

- Interest deductibility on existing dwellings will be scrapped from March 27th, or phased out over four years on existing investment properties. The Govt has yet to decide on interest deductibility for new builds.

- On the supply side, a minuscule $3.8bn will be set aside for a new “accelerator” fund which councils can access for housing infrastructure needs. The fund will be funded by normal Govt debt issuance. The size of the fund is tiny, and hard to take seriously. We know it will grow; it must. But we should have seen a more respectable figure the fund could grow into, rather than a 3.8 figure the fund will grow out of in 5 minutes.

- Kāinga Ora will issue NZ$2bn more debt for land purchases, separate to the housing accelerator fund. They can at least build homes.

- House price caps will be increased on the Home Start Grant and First Home Loans. The lower quartile house price has increased dramatically in the last year alone. With 5% deposits being eligible for singles on $95k (up from $85k) and $150k for couples (up from $130k).

- We were pleased to see the Govt tilting tax advantages in favour of new dwellings. Investors will be more willing to build, and more willing to add to the housing stock, which is in short supply.

Today the Government released its much-awaited housing policy response to the current housing crisis. Policy decisions are desperately needed. We estimate that NZ is 80,000 homes short of where it needs to be, and house price growth is at stratospheric levels. And increasing number of people out shut out of the housing market. Unfortunately, the major changes needed to boost supply were absent today. Our closed border may help us eat into the shortage in the near term, but it misses the point. Housing supply is simply not fast enough to respond to demand pressure in NZ.

The main announcements target property investors, with the extension of the bright-line test on investment property sales from 5 to 10 years. In addition, tax deductibility of interest expenses is to be removed from the 27th of March for new purchases. We believe these demand side measures will have a meaningful impact on the investor community. The hurdles for investors include a 40% deposit coupled with the possibility of a firm DTI restriction, laced with evaporating interest deductibility and a 10-year bright-line test. We are encouraged by the exclusion of new properties. Nudging investor demand into new builds will help boost supply.

The Housing Acceleration Fund is a superb idea. Unfortunately, it’s a superb idea that’s already under-resourced. NZ$3.8bn is merely a drop in a leaky bucket, and is unlikely to have a meaningful impact on infrastructure investment or housing supply. But it is a positive step in the right direction. It is important to grow the fund, so the funds can truly accelerate councils. The greatest challenge developers face is finding viable land to develop, and getting council consent to develop. “Accelerating” the consent process is what’s needed.

Income and house price cap increases to the Home Start Grant and First Home Loans for first home buyers, are changes in the right direction. However, the income caps of $700k in Auckland and $650k in Wellington and Queenstown are still likely to be seen as well below market, given the lack of supply of property in these price ranges.

The $2bn increase in Kāinga Ora borrowing allowance for land purchases is a positive development from today’s announcement. The agency has a good track record of building homes for the vulnerable locked out of the private rental market. And we need a meaningful increase in the social housing stock, not just the retrofitting of existing homes.

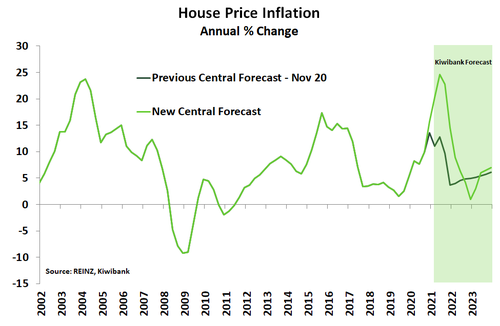

Today’s changes are unlikely to have an immediate cooling effect on house price growth. The return of LVRs may not be having much of an impact on investor activity as previously thought. The recent surge in house prices has only boosted investors’ equity on existing portfolios. We had expected some developments on the approval of Debt-to-income (DTI) and interest-only lending restrictions on investors. But this still looks to be in the pipeline. The RBNZ is expected to make an announcement in May. The RBNZ however still needs to be given the green light on DTIs from the Minister of Finance. Meanwhile we are forecasting annual house price growth will peak at 25% across the country in the June quarter. The tweaks to demand should take some heat of the market. But house price growth is still expected to remain in double-digit territory by the end of the 2021, eroding some of the changes made today to help first home buyers.

Today’s changes are unlikely to have an immediate cooling effect on house price growth. The return of LVRs may not be having much of an impact on investor activity as previously thought. The recent surge in house prices has only boosted investors’ equity on existing portfolios. We had expected some developments on the approval of Debt-to-income (DTI) and interest-only lending restrictions on investors. But this still looks to be in the pipeline. The RBNZ is expected to make an announcement in May. The RBNZ however still needs to be given the green light on DTIs from the Minister of Finance. Meanwhile we are forecasting annual house price growth will peak at 25% across the country in the June quarter. The tweaks to demand should take some heat of the market. But house price growth is still expected to remain in double-digit territory by the end of the 2021, eroding some of the changes made today to help first home buyers.