RBNZ ready to deploy DTIs

- Today’s FSR shows that NZ’s financial system is in a more encouraging place than previously thought possible given the shock of covid.

- However, the growth in high-risk mortgage lending has been a concern. For now, the RB will watch and wait to see the impact of tighter LVRs and recent Government policy changes.

- If needed, and if approved, the RBNZ would be comfortable to introduce DTI lending restrictions, with a considerable 6-month lead time.

- The ultra-low interest rate environment globally has shifted investors up the risk spectrum, but also increasing financial market vulnerabilities.

Summary

Without the prospect of a new policy announcement, today’s Financial Stability Report (FSR) had already lost its drawcard. The RBNZ is set to publish final analysis on additional macro-prudential tools toward the end of the month. It’s clear the RBNZ is willing to tighten macro-prudential policy further, and even utilise new tools, if required. And the RBNZ favours the use of Debt-to-Income (DTI) restrictions. “In terms of new tools, our assessment is that a debt serviceability tool would be the best option for supporting financial stability and sustainable house prices over the medium term.” However, any new policy options have significant lead times of around 6 months before implementation. And the RBNZ has yet to be given the go ahead from the Minister of Finance. For now, the RBNZ will wait and see how recent tightening of LVRs and the Government’s housing policy changes impact the housing market.

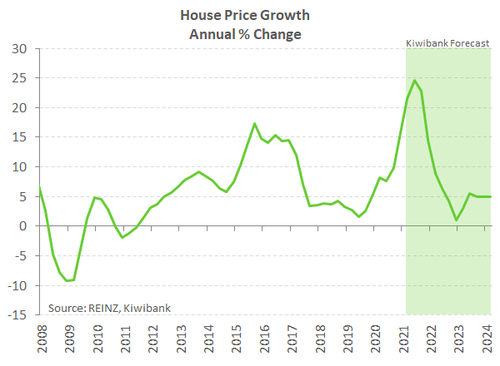

Aside from policy talk, there was still plenty of meaty analysis to chew over. Housing, specifically mortgage debt, was again at the centre of the report. And a rampant housing market, posting near 25% price gains, is a cause for concern. The rise is in part a consequence of ultra-low interest rates, forcing investors out the risk spectrum in the hunt for yield. The market is now more sensitive to the risk of rising interest rates. And the RBNZ will be cautious in any attempt to lift interest rates as a result.

Beyond housing, the RBNZ is encouraged by the performance of the economy in the Covid world. The global economy has emerged with vigour, after a difficult 2020. Tremendous monetary and fiscal policy support combined with a speedy vaccine rollout in the developed world has buoyed confidence. Kiwi export commodity prices continue to lift and support indebted areas of the primary sector such as dairy. Furthermore, the unemployment rate now looks more likely to have peaked at an astonishing low 5.3% in the current cycle. Today StatsNZ released the March quarter employment report at showed a further fall in the unemployment rate to 4.7%. The welcome surprise in the labour market has eased fears around mortgage defaults and has given banks the confidence to continue lending to households and businesses.

Of course, it wouldn’t be much of an FSR without highlighting risks. And covid remains a major risk as NZ is early in its quest to vaccinate the population. The closed border has increased the vulnerability of certain sector, such as tourism and education, if we were to face another major economic shock. However, these sectors aren’t traditionally highly leveraged. Rising Government debt worldwide is also a longer-term risk factor. NZ is no exception, with massive fiscal support deployed last year to fight the pandemic. However, NZ sovereign debt levels remain low compared to other developed counties.

High-risk mortgage lending is a central concern

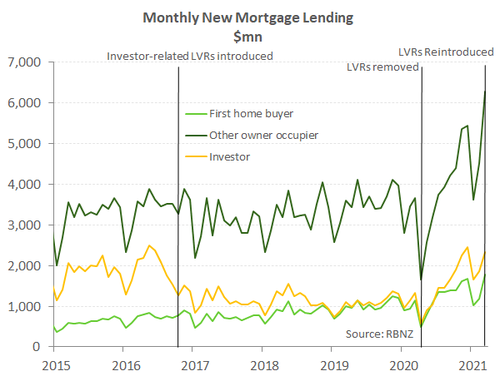

The RBNZ noted the rapid rise in high-risk mortgage lending in on the back of the current housing market boom. While the stock of high LVR lending remains historically low, the recent growth of high-risk lending would be a concern if it was to continue. The RBNZ pointed to the reintroduction and tightening of LVR lending restrictions, and the Government’s changes in tax policy targeting investors. However, like us, the RBNZ needs more time to access how recently announced changes impacts the market. If the RBNZ had been given the go-ahead to use DTI restrictions today, they probably wouldn’t have been applied. It’s too soon.

Early signs of the effects of recent policy changes are mixed. As we have pointed out previously, recent LVR tightening may not slow the market as much as expected. The recent surge in house prices has helped to push up investors’ equity on existing portfolios. Equity that can be used as a deposit for additional borrowing. And looking at the latest bank lending data, owner-occupiers look well placed to take up any slack from investors.

Early signs of the effects of recent policy changes are mixed. As we have pointed out previously, recent LVR tightening may not slow the market as much as expected. The recent surge in house prices has helped to push up investors’ equity on existing portfolios. Equity that can be used as a deposit for additional borrowing. And looking at the latest bank lending data, owner-occupiers look well placed to take up any slack from investors.

We believe there is enough momentum in the housing market to see annual house price growth peak at 25% in the current quarter before losing momentum. We anticipate the house price growth will slow quickly over the second half of the year.

While a risk, a sharp correction in the housing market is unlikely in the foreseeable future. Underpinning the housing market is an ongoing and significant shortage of property. “Supply constraints – including land-use restrictions and barriers to the provision of infrastructure – have seen increased demand for housing translate into higher rents and house prices. While supply remains constrained, construction activity has increased and is expected to remain high. With border restrictions reducing migrant inflows, new housing supply is starting to outstrip population growth.” As we recently published, despite producing a surplus of 13,000 homes over the last year, NZ remains 67,000 homes short of balancing the market. A closed border is helping builders catch up. But there’s still a huge shortfall that will take years to balance.

Interpreting the new remit

The RBNZ’s policy remit has changed. And the RB provided an analytical box (Box A) on the interpretation of the remit change to support the Government’s aim of sustainable house prices. The RBNZ defines a sustainable house price as “…the level that the price would be expected to move towards over several years, given the outlook for fundamental drivers.” Large price fluctuations away from a sustainable house price, would be a cause for concern. Although estimating an actual sustainable price would be difficult and will likely done by feel.

The lack of housing supply is a key driver of house price growth. And supply cannot be addressed by demand side policy, such as those at the disposal of the RBNZ. We hope the Government’s upcoming Budget takes a few more steps to “accelerate” supply.

Ultra-low interest rates have fuelled risk taking

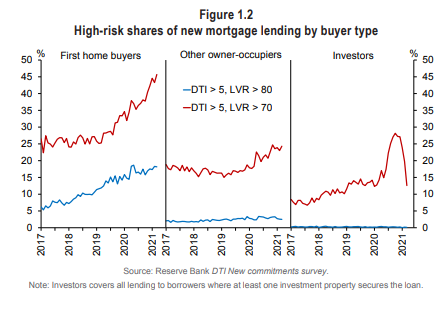

Asset markets, globally, are responding to record low interest rates and waves of fiscal and monetary stimulus. In NZ, the housing market has benefitted the most, with a chronic shortage of affordable homes. Residential lending has accelerated, with a rise in higher risk loans. Looking at the flow of high DTI and LVR lending, first home buyers stick out, as expected. As we’ve noted on numerous occasions, blanket DTIs would adversely impact first home buyers the most.

Lending to investors spiked in the second half of 2020, but has been reined in since, as banks effectively implemented the RBNZ’s LVR restrictions from December. Interestingly, looking at measures of current DTI, its owner-occupiers that are taking a large chunk of high-risk lending. Tightening of LVRs have been effective at cooling high-risk investor lending. It’s not clear that the Government has the appetite to direct DTIs toward owner-occupiers. This is an important point as recently announced reform to the Reserve Bank Act will give the Minister of Finance the power to decide what type of lending the RB can target.

Lending to investors spiked in the second half of 2020, but has been reined in since, as banks effectively implemented the RBNZ’s LVR restrictions from December. Interestingly, looking at measures of current DTI, its owner-occupiers that are taking a large chunk of high-risk lending. Tightening of LVRs have been effective at cooling high-risk investor lending. It’s not clear that the Government has the appetite to direct DTIs toward owner-occupiers. This is an important point as recently announced reform to the Reserve Bank Act will give the Minister of Finance the power to decide what type of lending the RB can target.