There’s not much upside in the upside within the current macro environment. But there’s plenty of downside in the downside.

- Financial markets are now in a risk off environment, as aggressive rate hikes have started to deliver strain to the banking sector, especially in the US. Risk off environments are generally not a friend to the Kiwi dollar. But a lot of uncertainly remains.

- Near-term, we see the Kiwi being supported for now, but we are breaking this up into multiple scenarios. And on the balance of these different scenarios, we see it more likely that there is downside risk for the Kiwi.

- The updraft in the Kiwi flyer, which we predicted at the end of 2022, has now ended. As the world plunges into recession and commodity prices decline, we will most likely see the Kiwi currency spiralling lower. We still forecast a drop to 55c by year end.

The backdrop.

The last quarter has largely played out as we expected in our December publication. We picked that the Kiwi dollar would remain in a bit of an updraft. And it did, climbing all the way to 65c. The RBNZ proved to be fairly more hawkish than its peers, and the Fed appeared to be pivoting with a slowdown in rate hikes. Risk sentiment had improved with growing speculation that the chapter of policy tightening was coming to an end. The USD was dumped, and the Kiwi flyer took off. We pat ourselves on the back. But a good thing never lasts. Hold the champagne.

A lot has happened since our last FX Tactical. Inflation has indeed peaked, but the road back to ‘normal’ is shaping up to be a painfully slow and bumpy one. The threat of persistent inflation lingers. In response, the US Federal Reserve and others have doubled down on the “higher for longer” rates rhetoric. The Greenback regained favour, and the Kiwi flyer lost air. But now, the aggressive tightening from central banks is starting to put the skids into the market.

Pouring cold water on the Fed’s heated message however has been the recent banking sector woes. Financial markets have been roiled by the troubles emerging in the banking sector overseas. We’ve seen the collapse of three US banks, followed by the failure of Swiss banking giant, Credit Suisse. Authorities, regulators, and fellow banks have swiftly stepped in with generous support to shore up confidence. But fears of banking contagion risks remain. Uncertainty is high, risk sentiment is fragile, and financial markets are volatile. “March madness” takes on a whole new meaning this year.

In today’s topsy-turvy environment, picking the levels and direction of currency in 10 minutes’ time would be a fool’s errand – let alone in three months. Short of pulling out the tarot cards, we’ve taken a scenario-based approach. We’ve mapped out three possible futures for the Kiwi dollar – welcome to the multiverse.

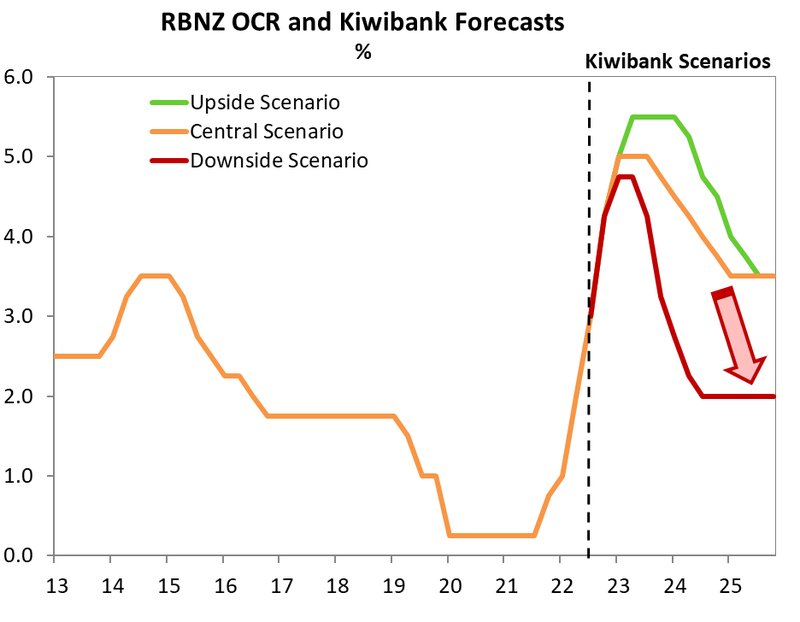

Central scenario (60%): As you were.

Our central scenario is unchanged from our publication in December. In our central scenario, the global disinflation process continues. Fears of bank contagion ensuing from the bank failures dissipate, and markets regain composure. The focus returns to the Fed and the task at hand – returning inflation back to target. With inflation still uncomfortably and unacceptably elevated, central banks will remain on the front foot. But progress so far is pleasing. The Bank of Canada has already paused. The RBA looks to be close behind. The US Fed is expected to hike just once more. And the BoE and ECB will also pause in coming months. We’ve seen a sharp reduction in expected monetary tightening due to uncertainty in financial markets. And the inflation outlook will improve with weakening risk appetite and restrained credit creation. The tightening cycle is drawing to a close.

South of the equator, the RBNZ is also closer to a terminal rate. The RBNZ is hell-bent on breaking the back of the inflation beast, with their thoughts centred around a 5.5% terminal rate. Although, as we have noted on many occasions, the RBNZ’s pre-set path to 5.5% is likely to be a step too far, and cause a deeper recession than they forecast. We believe the OCR should peak at either 4.75% or 5%, and pause for six months. Enough is enough, and the RBNZ has done more than enough.

A soft landing still seems achievable in our central scenario, thanks to robust labour market conditions. There’ll be a slowdown in economic activity. A contraction of a similar magnitude as past recessions however looks unlikely. A lift in the unemployment rate is expected as the Kiwi economy heads into recession and the labour market loosens. However, at a forecast 5.5% (currently 3.4%), that unemployment rate would be significantly lower than previous recession-highs. It’ll be a jobs-rich recession – one for the history books!

We’ve seen a dramatic shift in thinking from continued rate hikes to rate cuts. Market traders are factoring in rate cuts later this year. A whopping 75bp of cuts are priced into the US curve, beginning in September. The same is playing out in the Kiwi curve. Rate cuts are factored in as early as August, with the rate trajectory tumbling to 4.3% by the end of next year. We think the market is getting ahead of itself – as it often does. The RBNZ will disagree with current pricing, at least until they see inflation within their 1-to-3% target band. Rates should grind higher in the near-term, as we bounce back from the panic surrounding the bank failures.

In our central scenario, we see the Kiwi dollar drifting around current levels, with some upside into the 0.6365 resistance level, and then potentially beyond that – depending on market volatility. If the Fed is able to refocus itself onto inflation, rather than a banking crisis, then the Fed is likely to pick up where they left off, and that was hawkish. The market will re-price in line with the Fed’s most recent, and unchanged, dot plot which signals a 5.1% peak. In this scenario there is some upside to the US Dollar which will keep a lid on the Kiwi dollar.

Heading into year end, our central scenario has the Kiwi dropping to 55c. It sounds like a big move, but it is not. We hit 55c on October 13th last year. We’d simply retrace to the previous low. Ultimately, the rapid rate rises will tame inflation. Weaker global growth will put downward pressure on commodity prices and commodity currencies – like the Kiwi (and Aussie) dollar.

Upside scenario (10%): Re-acceleration required.

Our upside scenario assumes the task of bringing inflation down from such lofty heights, is increasingly difficult to achieve. The year has kicked off with a re-acceleration in key measures of economic activity, and inflation readings have surprised to the upside. In this scenario, strong momentum continues. And price pressures prove to be prickly and persistent. Central banks will be forced to tighten even more than anticipated. Prior to the banking system woes, the Fed had clearly signalled their willingness to pick up the pace, if needed, to tame inflation. In comments made during a testimony at Capitol Hill, Chair Jay Powell truly let his hawkish flag fly. “If the totality of the data were to indicate that faster tightening is warranted, we would be prepared to increase the pace of rate hikes”.

In this scenario, sticky inflation will force the Fed to follow through with their uber-hawkish policy stance. Rate cuts will be a story for later in 2024. The RBNZ is expected to keep pace with the Fed, and potentially do more. Unlike in the US and elsewhere, we’ve yet to see Kiwi inflation truly turn, instead it's hovering around the 7% mark. The RBNZ is seen going all the way to 5.5%, as signalled in November and reaffirmed in February. More is needed to bring down inflation and temper price growth expectations. But the more tightening, the greater the risks of a hard landing.

In this upside scenario, there is some upside for the Kiwi dollar, again largely driven by rate differentials. The RBNZ is still on the hawkish side compared with other central banks. Should they continue to signal the delivery of another 75bp of hikes, the Kiwi dollar will benefit, initially – in the short-term of three or so months. But in an environment where the RBNZ indeed delivers all these projected hikes, recession risks grow.

Downside scenario (30%): March madness magnified.

There are numerous downside risks, and they heavily outweigh the upside risks. Here and now, fears of bank failures and contagion risks are front and centre. Although we believe policymakers will continue to act, in desperation, to contain fears and ultimately backstop market liquidity… we never say never. A full-blown bank crisis is still unlikely, in our opinion, but the probability of such risk is clearly higher today than it was a month ago. An uncontrolled meltdown in capital markets may shut the door on foreign funding for Kiwi banks. Risk appetite would evaporate as investors run for the ‘safest’ assets they can find – think Government bonds, gold, and currencies like the USD, Swiss Franc (although tarnished by Credit Suisse), and the Yen. Bank spreads would blow wider, and credit creation (the oil in the economic engine) would seize. The Kiwi dollar would be dropped, without warning. We could see the Kiwi drop well into the 50c range, and maybe into the high 40s. There are no strong resistance levels in a true banking crisis. There are simply more sellers than buyers at (almost) any price. The Kiwi traded below 50c during the GFC and hit a post-float low of 39c in 2000. They’re just numbers. They’re not targets nor resistance levels. They simply show that there is a lot of room below 60c.

The greater risk is weaker economic output (with or without bank funding pressures). Global growth is already forecast to weaken materially this year, and the risks are to the downside of downwardly revised forecasts. If we see a sharper downturn, with deeper recessions across most economies (big and small), commodity currencies will get hit hard. Most hard and soft commodities will trade lower as global activity contracts.

In this downside scenario, the Kiwi dollar is much lower. With credit conditions likely to deteriorate as credit spreads widen, availability for growth is diminished. A flight to the safety of traditional safe haven currencies will follow. And if the RBNZ are indeed forced to change tactic, the previous appeal of the NZ Dollar as a higher yielding currency will quickly diminish. We see downside here, well below 0.5910 and the Kiwi dollar could even head into the 0.55 level quite easily in the upcoming quarter(s). Again, a weaker economic growth scenario would see the Kiwi trade towards 50c (our central scenario is 55c).

Kiwi crosses in the months ahead.

NZDUSD

3-year daily – A failure to move beyond 0.6550 in the last quarter now provides a strong multi-year upside resistance zone into this area (0.6550/0.66). Technically, the longer term picture is bullish with the formation of a reverse ‘head and shoulder’ pattern (circled) now in place. The fundamental backdrop argues otherwise however. A breach of the 0.6080 shoulder support level opens up a move into the low 0.59s – our preferred course of direction within the murky multiverse over the coming quarter.

NZDAUD

5-year daily – you zig, it zags. The reversal from December’s heavily overbought high of 0.9550 provides a classical technical analysis lesson of the fundamentally correlated NZDAUD. A reversal into the 61.8% Fibonacci level (0.8703 – 0.9550) at 0.9027, often referred to as the ‘Golden pocket’ zone, has repelled further downside for now. The timing of looming peak central bank tightening and then eventual loosening will ultimately drive moves to either end of NZDAUD’s traditional 0.90 – 0.98 range. However, the multi-year downtrend highlighted does now argue for further eventual downside from current levels from a risk/reward perspective.

NZDEUR

5-year daily – As detailed in the last FX Tactical, the “descending peaks” longer-term picture has proven to be a bearish outcome. With the EUR also now benefiting as a haven from the US and Swiss banking crisis and a steadfast ECB, downside moves are now approaching the next big test of key support at 0.5700/25 (Oct 22 low, and 50% retracement of 0.5020-0.6413). Given our preferred NZDUSD outlook it would not be surprising to see an ultimate move into the narrowing downtrend triangle support area of 0.5650 in coming weeks.

NZDGBP

5-year daily – Same, same, but slightly different. The pattern continues to converge, however again like the EUR, the pound has outperformed in recent weeks. A break of the 0.51 “pivot zone” now sets up a move to 0.4950. Will this be the move that breaks the multi-year narrowing triangle? If so, then lows in 2022 become the next downside targets.

Glossary

Commodity currencies: include the Kiwi dollar, Aussie dollar, Canadian dollar, Norwegian krone as well as currencies of some developing nations like the Brazilian real. These countries export large amounts of commodities (raw materials like oil, metals and dairy) to the world. And commodity currencies are highly correlated with the global prices of such commodities. When the global economy is strong and demand for commodities is high, commodity prices and thus commodity currencies, tend to outperform. The Aussie and Kiwi dollars are famously known for the sensitivity to good news (risk on) and bad news (risk off).

Interest rate differentials: The difference between the interest rates earnt on two different currencies. New Zealand may offer a significantly higher interest rate than those in Japan, for example, and we see an inflow of Yen into Kiwi dollars (known as the “carry trade”). The widening, and narrowing, of interest rate differentials can have a material impact on capital flows and therefore the exchange rate.

Monetary hawk (hawkish) and Monetary dove (dovish): Characterisations of central bank monetary policy. The hawk is a bird of prey and describes a central bank aggressively raising interest rates to slow economic growth and tame the inflation beast. The peace-loving dove however, reflects a central bank trying to stimulate economic growth by cutting interest rates.

Moving averages: A common method used in technical analysis to smooth out price data by showing the average over various time periods.

Reserve currency: The US dollar is the global reserve currency. The dominance of the US dollar in international trade means most central banks and financial institutions hold large amounts. The majority of FX reserves are held in US dollars. The US currency and debt markets are the most liquid in the world. And liquidity (the ability to buy and sell, especially in times of stress) is important. The next most traded currency is the Euro, but it is nowhere near as popular as the US dollar. About 60% of global reserves are held in dollars, with the Euro attracting only 20%, according to the IMF.

Support and Resistance levels: These are chart levels that appear to limit a currency’s price movement. A support level limits moves to the downside; a resistance level limits moves to the upside.

Terms of trade: The ratio of the prices at which a country sells its exports to the prices it pays for its imports. Put simply, terms of trade is a measure of a country’s purchasing power with the rest of the world. How many imports can be purchased per unit of exports – import bang per export buck. An increase in our terms of trade means New Zealand can purchase more import goods for the same quantity of exports. And a rising terms of trade lifts the incomes of exports and the businesses and communities that support them.