Extraordinary policy responses work

- Unprecedented times demand unprecedented action. Our economy has slipped into a global recession, with most of our industries in lockdown.

- Economic forecasting is difficult at the best of times. The unprecedented nature of the global lockdowns is making reasonable forecasting near impossible. We aim to show the most likely outcomes through scenarios.

- On a positive note, the speed and cohesiveness of policymakers in the Beehive, the RBNZ, and the banks to do whatever it takes is lessening the blow

Flattening curves and forecasts

As economic forecasters, we suddenly feel like Wile E Coyote, looking down without solid ground. The decision to lockdown the country was the correct decision. Health and safety first. We must supress the spread of Covid-19 so our healthcare system can cope. We must flatten the curve. But in doing so, we supress economic activity. The recession we last mentioned, looks likely to last a lot longer and dip a lot deeper. The good news is the policy response to date has been swift and sizeable.

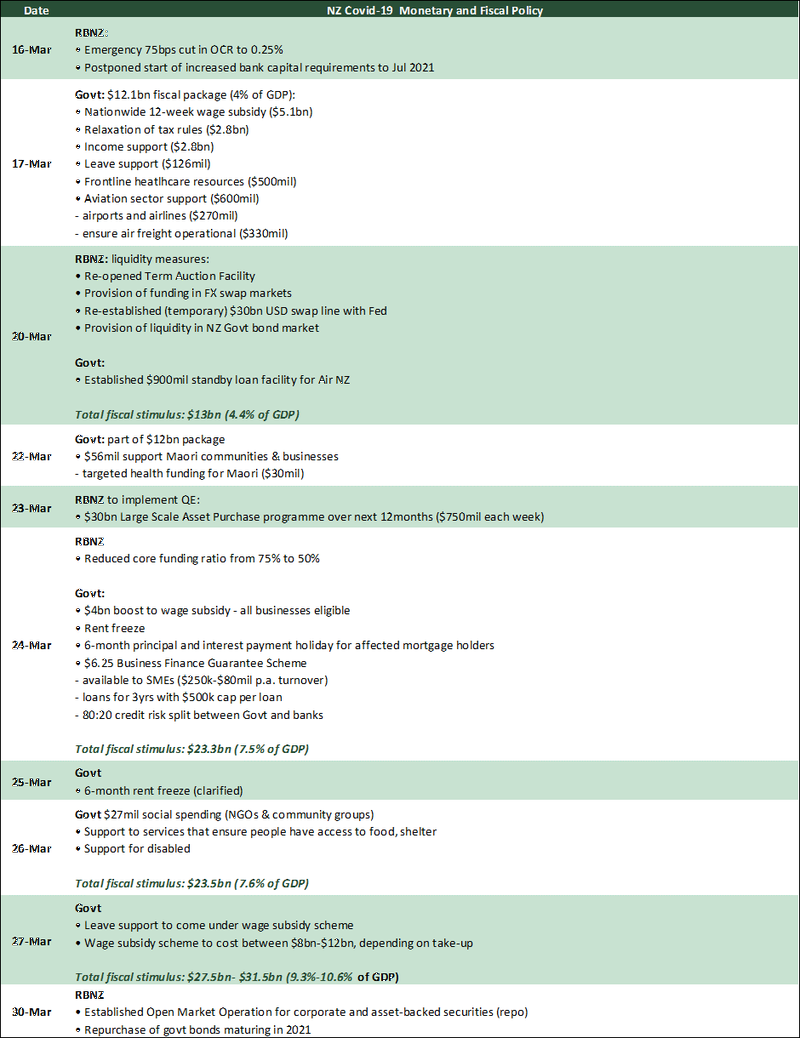

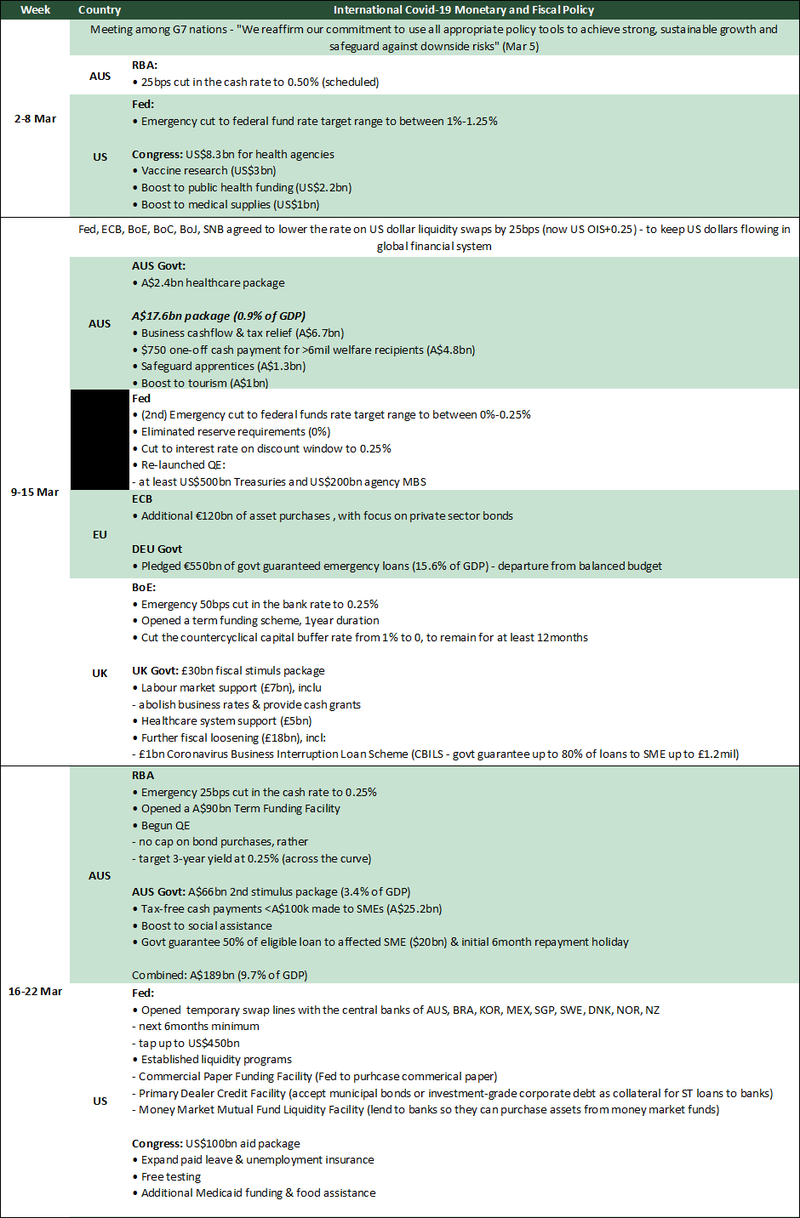

There’s a clear sense of coordination in monetary and fiscal policy across the globe. Most major central banks have cut interest rates down to the operational lower bound. QE is front and centre, once again. And governments are implementing economic relief packages of unprecedented size (5-10% of GDP). All in the span of 28 days. The New Zealand Government package looks likely to rise above $20bn (6.75% of GDP), and the RBNZ has slashed interest rates and has become a backstop buyer in markets.

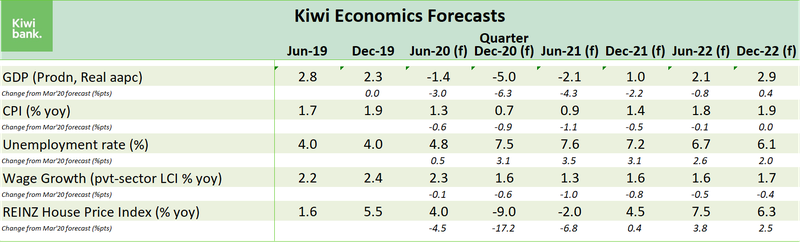

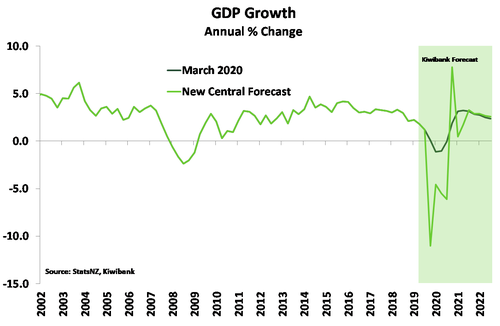

The lockdown has forced us to slash our economic forecasts. GDP is forecast to collapse 12%qoq in the June quarter, and the economy is expected to be 5% smaller over 2020. It would have been much worse had the Authorities not acted swiftly and decisively. But we don’t know if NZ’s lockdown will be extended or repeated in future. And we don’t know how households and firms will respond on the other side. If firms and households come out the other side cautious and continue some form of social distancing, the economic pain of Covid-19 will linger for longer. We therefore find it useful to undertake scenario analysis. Scenario analysis helps us understand the extremes of economic fallout if things worsen. In an extreme scenario where NZ is in lockdown for the entire June quarter, the economy could contact by upwards of 30%qoq in Q2. Under this scenario the economy would be 16% smaller over 2020 than 2019. Business closures would spiral, and job losses would be in the hundreds of thousands, in part because of the cautiousness of firms and households.

Stop fretting about Govt debt

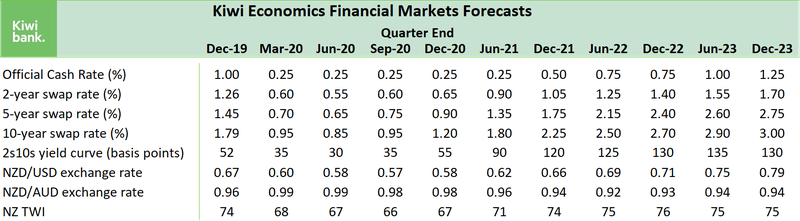

The Government can easily tap into debt markets at record low interest rates. And they have a backstop buyer in the RBNZ. Local and foreign investors still have ample appetite for the relatively safe Kiwi Govie bond. The Government will need to establish a credible return to surplus at some stage. But we have plenty of time in the current climate. Kiwi Government debt is currently rated Aaa under Moody’s and AA+ (positive outlook) under S&P. We’re rated higher than the United Kingdom, and most OECD countries. And our banks are well supported. For what it’s worth, rating agency S&P believes the fiscal stimulus to support the economy and monetary actions taken in the last few weeks should enable banks to support stressed customers and small and midsize enterprises so that the economy and the banking system continues to function while the COVID-19 outbreak continues. “The support measures announced by the RBNZ should alleviate any immediate funding and liquidity risks for the banks, in our view," said Lisa Barrett, a credit analyst at S&P Global Ratings. "Even though credit losses may escalate we think the banks' profitability should remain adequate to absorb increased credit losses, notwithstanding headwinds from low interest rates.”

Steering down the barrel

Since our last forecast update (link here) we’ve entered a four-week lockdown. A recession was already in train with the Chinese seizure to global supply chains. Now, the unprecedented lockdown will deepen the recession. We see the economy recording a record 12% fall in the June quarter alone. That’s big! Few, if any, industries will come out unscathed. A record fall in activity will be followed by a bounce back of sorts. We will come out of lockdown and try to resume life as normal – well as normal as possible. But continued caution and uncertainty is likely to hamper growth for some time to come. And the severe impact on business and household incomes will likely see the economy enter a second period of contracting activity heading into next year. Our activity is likely to look something like a W, rather than the hopeful V shaped recovery. We now see 2020 GDP as a whole being 5% below that of 2019. The risk is tilted towards an even deeper fall, if the lockdown is extended and business and consumer sentiment is hit even harder.

Economic forecasting is difficult at the best of times. The high level of uncertainty at present is making forecasting nigh on impossible. And we would place a large caveat on our forecasts. For one, we don’t know how long NZ will have to remain in lockdown – were hedging our bets and assuming four to six weeks. Epidemiological modelling produced by Auckland University’s Te Pūnaha Matatini (James, Hendy, Plank, Steyn, 2020; Suppression and Mitigation Strategies for Control of COVID-19 in New Zealand) illustrates the importance of the current nationwide lockdown. If no measures were taken to suppress Covid-19, NZ could face 80,000 deaths. James et al. (2020) is based on work published by the Imperial College of London (study here). The work done by Imperial College shows that one period of countrywide lockdown won’t eliminate Covid-19 entirely. NZ may need to extend the current lockdown or undertake continuous on/off periods of lockdown in order to supress the spread of Covid-19 long enough for a vaccine or successful treatment to be adopted. The longer NZ is in lockdown, the larger the impact on the NZ economy, businesses and jobs.

Second, we don’t know how firms and households will respond once lockdown is lifted. If firms and households come out the other side cautious and continue some form of social distancing, the economic pain of Covid-19 will linger for longer. Judging by the experience of China, once their lockdown was lifted, factories did gradually comeback online, but the demand side of the economy was less obliging. Chinese citizens were less willing or able to return to cities. Tentative spending behaviour here in NZ would be understandable. Moreover, the border is unlikely to be rapidly re-opened with cases of the virus still filtering around the world – cold comfort for the tourism sector. And the world economy will remain in recession. These factors are expected to tip the economy into a double dip recession.

Such a large shock will see a rise in business closures and job losses. But the Government’s support package should help take the edge off any hit to the labour market. The package includes a wage subsidy (a decent chunk has already been paid) and cheap short-term lending to business via the Business Finance Guarantee Scheme. These measures are vital to keep businesses alive and liquid. We expect the unemployment rate to peak between 7½-8% in the first half of 2021, before gradually falling thereafter. The unemployment rate always rises with a significant lag to activity.

However, the labour market data will be difficult to interpret in the coming quarters. Because many employees will still be ‘employed’ under wage subsidies, even though their job may not survive the lockdown. Labour force participation may also fall substantially. We expect the fall in participation to linger into 2021, but hopefully recover throughout next year.

Like much of the economy, the housing market has taken a hiatus due to the lockdown. On the other side of lockdown, the market is expected to stumble. An unemployment rate above 7% will impact demand and may force some selling. House prices are forecast to fall 9%yoy by the end of 2020, as some vendors looking for a quick sale may have to lower price expectations. The decline in house prices is expected to be on par with the GFC, even though the hit to economic activity from Covid-19 is likely to be far greater. The fundamental shortage in the housing market will not have vanished through the Covid-19 crisis. We will still have a chronic shortage of affordable houses. And the market will have even cheaper lending rates to support demand.

Flattening the curve

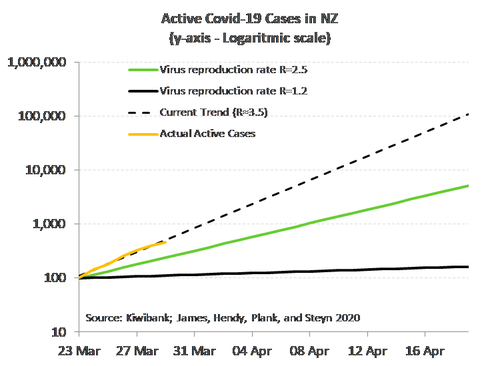

We must supress the spread of Covid-19 so our healthcare system can cope with the additional pressures. Or in other words, flatten the curve and slow the rate of new infectious cases. The modelling presented by epidemiologists show a dire outcome if we did nothing and allowed the virus to spread unabated. A feature these models is the assumption placed on R0 (or “R zero”). R0 is the reproduction rate of the virus or expected additional number of cases generated by each new case. We have done our best to recreate some of the estimates produced by James et al. (2020), under differing R0 assumptions of R0=2.5 and 1.2. Ideally an R0 less than 1 would see active cases fall. Like many developed economies NZ is currently running a R0 above 2.5.

A simple trend off the NZ’s active covid-19 cases (infections to date less recoveries and deaths) of recent days, NZ would hit 100k active cases by mid to late April. A frightening thought. But the nationwide lockdown will go a long way in putting the brakes on the number of new cases and lower R0. Given the long incubation period of the virus 5-14days, we won’t see the impact from the current lockdown for at least another week or two.

It could be much worse

In the current environment we find it useful to undertake scenario analysis. Scenario analysis helps us understand the extremes of economic fallout if things worsened. For instance, if NZ’s period of shutdown was extended for say the entire June quarter, GDP could plunge as much as 30%qoq in Q2. And while we would expect a significant rebound in growth in the third quarter, the economy would quickly enter a second period of contraction much deeper than what we forecast under our central view. For instance, the NZ economy could be 16% smaller over 2020 compared to 2019. We would forecast an unemployment rate peaking around 14% next year under this scenario too. However, under this scenario it’s hard not to see authorities stepping in to do more. That would be both additional fiscal and monetary policy. The Government may also look at the list of essential businesses allowed to operate during a lockdown. Allowing a broadening of firms on the list, but with restrictions to maintain social distancing.

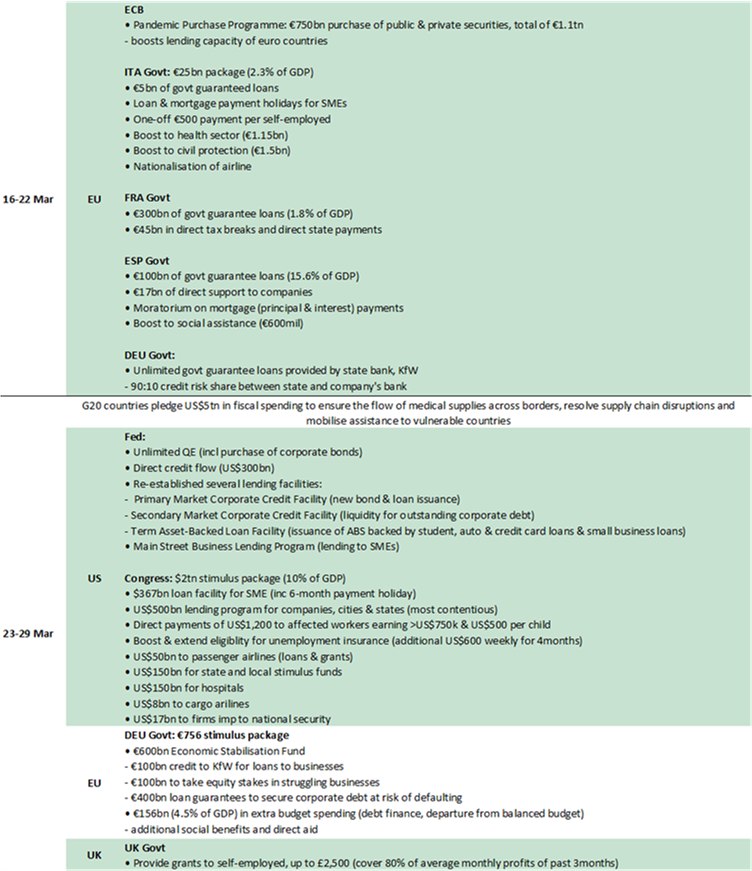

28 days later

There’s a clear sense of coordination in monetary and fiscal policy across the globe. Most major central banks have cut interest rates down to the operational lower bound. QE is front and centre, once again. And governments are implementing economic relief packages of unprecedented size (5-10% of GDP). All in the span of 28 days. Extraordinary times have demanded extraordinary actions – from a €1.1tn bond-buying bazooka to a reincarnated (US$2tn) “Marshall Plan”. “Whatever it takes” is the world’s anthem. Below is a timeline of key NZ and international policy actions to date.