- The Kiwi economy contracted, again. We saw a small decline of 0.1% in the first quarter. But the last quarter of last year was revised down to -0.7% (from -0.6%). We have a weaker starting point. Our economy is smaller than forecast by the RBNZ and Treasury. And the brunt of the slowdown is yet to come. We’re forecasting further contractions over the year ahead.

- Nothing in the report surprised. Business services and manufacturing posted hefty declines. The teacher’s strike had an impact. So too did the weather. With the cyclone impacting agriculture. Rental, hiring and real estate services enjoyed a strong quarter. We suspect the surge in migration is playing a part. Household consumption was weak. And that’s a direct result of higher interest rates hurting household budgets. Not to mention the cost of living and falling house prices.

- The weakness in the economy confirms our stance. The RBNZ may have done too much to rein in inflation. Time will tell. But the downside risks are dominating.

The Kiwi economy is now officially in recession. Technically, we’ve recorded two quarters of contraction. And we’re likely to see a lift in unemployment from here. The recession started much sooner than major forecasters predicted, ourselves included. And we have been more dovish than most. Importantly, our economy is smaller than forecast by the RBNZ and Treasury. The RBNZ’s heavy hand has hit households. And the Government’s tax take has taken a turn. Business revenues are now in question, with rising inventory. And the brunt of the slowdown is yet to come. We’re forecasting further falls over the year ahead. And monetary policy will have to be loosened before long.

Nothing in today’s report surprised. Business services were very weak, and manufacturing posted another hefty decline. The teacher’s strike had an impact. So too did the weather. With the cyclone and flooding negatively impacting agriculture. Rental, hiring and real estate services enjoyed a strong quarter, up 0.7%. We suspect the surge in migration is playing a part here. Household consumption, excluding durables and services, fell 3.4%. That’s weak. And that’s a direct result of higher interest rates hurting household budgets. Not to mention the cost of living crisis and falling house prices weighing on confidence.

It's important to note that the full force of the RBNZ’s rapid rate rises is still working its way through. The last rate rise, to 5.5%, was delivered in May. And rate hikes can take up to two years to work through the economy. We said it at the time, and we’ll say it again: the RBNZ should have paused at 5%. We think we’ll find that the RBNZ’s heavy hand did too much. It’s less about where we have been, and more about where we are going. And the outlook remains awkward, to put it politely.

We expect further contractions in economic activity over 2023, and possibly into 2024. Demand is being weighted down by rising interest rates. If households spend less, which is what we are seeing, then the economy will contract harder. If businesses pull back on their hiring and investment, which is what we’re hearing, then the economy will contract harder.

The forecast slowdown will drive a loosening in the labour market. Add to that the migrant-led increase in labour supply, at a time when demand is turning south. We may see the unemployment rate rising to 5-5.5% in 2024. As the labour market loosens, its inflationary impulse will soften.

At the end of the day, it’s all about inflation

Imported inflation is easing, but it’s homegrown inflation that concerns the RBNZ. Inflation is only forecast to fall below 3%, late in 2024. It’s still a long journey back to the 2% target. The good news is, we’re on the way.

Weak across the board.

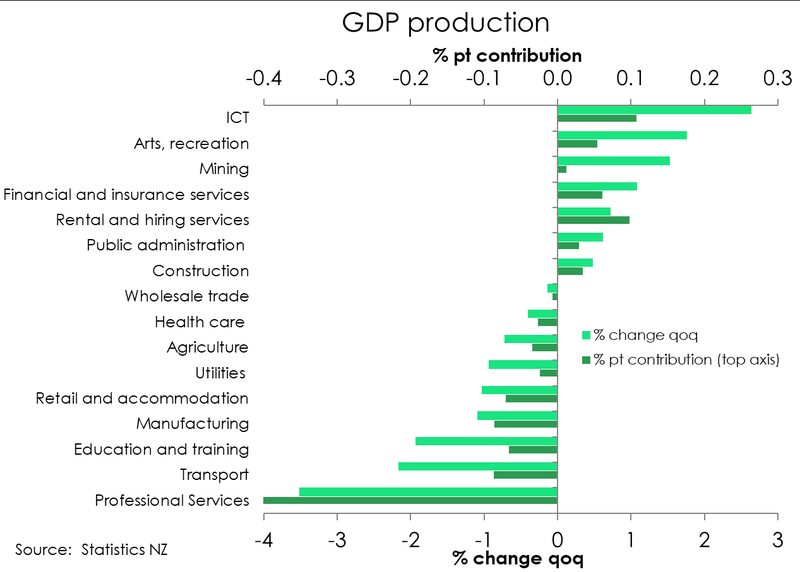

Another quarter, and another round of broad-based weakness. All three main industry groupings recorded declines in activity over the March quarter. Primary services contracted 0.5%. Agriculture managed to eke out a 0.6% lift in output, but was more than offset by the 5.1% and 2% respective declines in forestry and fishing. Output across the three industries posted a collective 0.7% decline – the third consecutive quarterly decline. Over the year to March 2023, output contracted near 3%. The 1.6% lift in mining activity provided some offset.

Activity across the goods-producing industries weakened over Q1. Last quarter’s 0.3% contraction was followed up with a 0.4% decline. And once again, it was manufacturing that recorded the deepest decline. In Q1 output fell 1.1% following a downwardly revised 2.1% drop in Q4 (previously 1.9%). The 0.5% expansion in construction activity was weaker than we were expecting. The upward revision to Q4’s print (1.8% vs 1.6% previously) may explain why we came up short. Nonetheless, growth in the quarter reflects the surprising resilience of the construction sector. But it’s on its last legs. Quarterly growth rates are slowing. No surprises given the weak housing market and continued downtrend in new dwelling consents. Consistent with the steady decline in new building consents, investment in residential building fell further over the quarter (down 0.4%).

Activity across the goods-producing industries weakened over Q1. Last quarter’s 0.3% contraction was followed up with a 0.4% decline. And once again, it was manufacturing that recorded the deepest decline. In Q1 output fell 1.1% following a downwardly revised 2.1% drop in Q4 (previously 1.9%). The 0.5% expansion in construction activity was weaker than we were expecting. The upward revision to Q4’s print (1.8% vs 1.6% previously) may explain why we came up short. Nonetheless, growth in the quarter reflects the surprising resilience of the construction sector. But it’s on its last legs. Quarterly growth rates are slowing. No surprises given the weak housing market and continued downtrend in new dwelling consents. Consistent with the steady decline in new building consents, investment in residential building fell further over the quarter (down 0.4%).

The services sector was especially weak, with a 0.6% quarterly drop in output. The 3.5% drop in business services led the descent. The teacher’s strikes throughout the quarter were also a drag on output. Education posted a near-2% decline. StatsNZ measures output based on the number of students receiving education. And with the teachers’ strike, attendance was light.

The services sector was especially weak, with a 0.6% quarterly drop in output. The 3.5% drop in business services led the descent. The teacher’s strikes throughout the quarter were also a drag on output. Education posted a near-2% decline. StatsNZ measures output based on the number of students receiving education. And with the teachers’ strike, attendance was light.

International visitor arrival numbers remain well below pre-covid levels. And the absence of international tourists continues to weigh on the tourism-dependent service industries. For instance, accommodation & food services fell 0.9% while arts & recreational services posted a chunky 6.2% decline. The weak quarter may also be a function of constrained supply. The resourcing constraints plaguing many sectors, particularly staffing in hospitality, has been well documented. And the ability of the tourism sector to service demand over the holidays was likely inhibited.

Spending softens further.

On the other side of the same coin, expenditure GDP also contracted – down 0.2% in the March quarter. The main drag was the fall in retail and wholesale inventories. Covid-related border restrictions prompted a shift in inventory management from ‘Just in Time’ to ‘Just in Case’. Inventory levels grew every quarter in 2022. But supply chains are normalising and signs of slowing domestic demand are emerging. Retailers and wholesalers are sitting on enough stock.

Mirroring the rebound in food-related manufacturing production (from -2% in Q4 to 1.2% in Q1), the export of goods lifted 0.6%. That was more than offset by a 1.5% decline in export services, partly payback for Q4’s 5.7% rise. Together the export of goods and services declined 2.5%.

The relatively softer growth in construction activity was mimicked by rather weak investment activity. A slowing housing market has seen investment in residential building pull back (-0.9%). Non-residential building investment however picked up 4.3% over the quarter. We may see further investment in this space as the Cyclone rebuild continues.

Providing some offset was the 2.5% gain in private consumption – following flat growth over Q4. A return to growth was driven by the 2.3% increase in international travel. But goods consumption deteriorated further over the March quarter. Consumer spend on durables goods fell 0.9%. And the 0.2% decline non-durables goods in Q4 was followed up with a deep 3.4% decline. Household spending looks to be wilting in the face of the surging cost of living, declining wealth – largely the result of falling house prices – and rising interest rates. A worsening economic outlook has seen consumers trim discretionary spending. The June quarter looks like it’ll be another soggy one for retail. Electronic card spend declined almost 2% over May, with little want for big-ticket items (motor vehicles, durables etc). It’s growing evidence that households have begun (and will continue) tightening their belts.

A significant slowing over the second half.

The second half of 2023 is a different story. The RBNZ is actively working to slow domestic demand to rebalance the economy and return inflation to target. The RBNZ has lifted the cash rate a total of 525bp in the span of just 19 months. While the RBNZ may have called time on rate hikes, previous increases are still working their way through the economy. There’s still a significant chunk of Kiwi mortgages enjoying the low rates of 2020/21. But when the time comes to re-fix, household discretionary incomes will inevitably squeezed. From here, the appetite to spend will wane further, and in turn, economic activity will weaken further.

Monetary policy settings have been tightened, aggressively. And the global backdrop is weakening, especially as China’s post-Covid recovery is losing steam. We still expect a significant slowdown in economic activity over the second half of the year, and heading into 2024. One upside risk to the growth outlook is the recent surge in net migration. The magnitude of migrant flows over the last few quarters has surprised most. Annually, net migration is running at over 72,000. And we’re on track to hit 95k-100k later this year (read more here). Net migration is dual-faceted. A boost to population holds implications for both the supply- and demand-side of the economy. But with today’s mix of migrants, the surge may prove less inflationary than previous episodes. Rising net migration is helping to increase the capacity of the economy – more than it is adding to aggregate demand. Evidence in support of this is growing. First, migrants come here at a working age, and they’re keen to work. The latest labour market update (Q1) showed strong employment growth with the resurgence in migration. At the same time, retail card spending declined by almost 2% in May, despite the rise in migration. We expect the current migration boom to exert more downward pressure on wages, than it will add to aggregate demand and inflation.

There’s more and more hard evidence that domestic demand is responding to restrictive monetary policy, as desired. We don’t believe further hikes to the cash rate are necessary. We expect the RBNZ to keep the cash rate at 5.50% for the remainder of this year. Rate cuts will likely be the next move, but not for a while yet.