- The RBNZ lifted the cash rate 25bps to 0.5% today, as expected. The lift off marks the start of the first tightening cycle in seven years.

- The RBNZ’s dual mandate, targeting inflation and maximum employment, has well and truly been met. And rampant house prices remain a cause for concern.

- Financial markets were (near) fully priced for the move. Traders had prepositioned and the reaction in financial markets was relatively subdued. Interest rates continue to climb higher, and the Kiwi dollar is stuck in quicksand. The Kiwi dollar is undervalued in our view.

We have lift off, after a slight delay

The RBNZ lifted the cash rate 25bps to 0.5% today, as expected. The Kiwi economy has solid momentum and the RBNZ has good reason to withdraw stimulus. And he RBNZ won’t stop here. October marks the beginning of a new chapter for the cash rate: Onwards and upwards.

The RBNZ lifted the cash rate 25bps to 0.5% today, as expected. The Kiwi economy has solid momentum and the RBNZ has good reason to withdraw stimulus. And he RBNZ won’t stop here. October marks the beginning of a new chapter for the cash rate: Onwards and upwards.

“The current COVID-19-related restrictions have not materially changed the medium-term outlook for inflation and employment since the August Statement.” (RBNZ MPR October’21)

Looking ahead we expect today’s rate hike will be the first in a series of hikes towards 1.5% and possibly higher. As signalled by RBNZ Assistant Governor Christian Hawkesby, a least regrets approach will be one with “considered steps”. We expect a 25bp hike to be delivered in October, November, February and May, with the OCR reaching 1.50% by the middle of next year. We expect a considered pause around 1.5%. Although the RBNZ is signalling a continuation to 2% in 2023.

That’s an aggressive track compared to our own forecast track which struggles to rise above 1.5%.

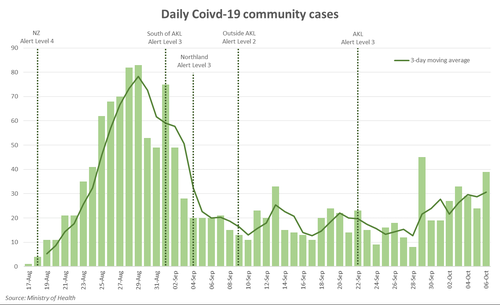

A proviso to our forecast OCR trajectory is of course the current covid outbreak. The delta variant is proving more difficult to stamp out. Another 39 community cases were recorded today, and there’s news that cases have spread further South. An escalation of the outbreak cannot be ruled out. A return to tighter restrictions would challenge the medium-term outlook. In keeping with their ‘least regrets’, considered approach, we’d expect the RBNZ to hit pause if the outlook deteriorates. Although, the Kiwi economy in aggregate is proving incredibly resilient to these disruptions. It would take a far worse disruption than we’ve experienced to materially change the outlook.

A proviso to our forecast OCR trajectory is of course the current covid outbreak. The delta variant is proving more difficult to stamp out. Another 39 community cases were recorded today, and there’s news that cases have spread further South. An escalation of the outbreak cannot be ruled out. A return to tighter restrictions would challenge the medium-term outlook. In keeping with their ‘least regrets’, considered approach, we’d expect the RBNZ to hit pause if the outlook deteriorates. Although, the Kiwi economy in aggregate is proving incredibly resilient to these disruptions. It would take a far worse disruption than we’ve experienced to materially change the outlook.

All signs point to a strong bounce back after lockdown(s).

The Kiwi economy was on a tear heading into the Delta lockdown. Supercharged GDP growth of 2.8%was recorded in the June quarter and the labour market had returned to full employment. Crucially, business confidence surveys remain robust. Yesterday’s QSBO survey showed an anticipated knock to near term confidence, due to the lockdowns, but the all-important outlook for firms’ own activity and hiring intentions held up surprisingly well. Businesses have learnt to adapt to life in lockdown. The QSBO survey suggests once the current disruption ends, economic activity will bounce back strongly.

“Capacity pressures remain evident in the economy, particularly in the labour market. A broad range of economic indicators highlight that the New Zealand economy has been performing strongly in aggregate.” (RBNZ MPR October’21)

Covid aside, labour shortages, supply-chain and capacity issues all point to rising inflation well above the RBNZ’s 1-to-3% target range. And the housing market has continued to flash red with record price growth – although recent restrictions and speed limits point to a slowing market ahead.

A new chapter to look through

Despite the ongoing Delta outbreak, the medium-term outlook remains broadly unchanged. Employment is currently above the maximum sustainable level. And there’s risk of further tightening in the labour market. Hiring intentions have strengthened, and firms are limited to homegrown talent in their search for labour. Inflation too is accelerating. Not only has inflation already breached the top-end of the RBNZ’s 1-3% target band, but is expected to remain elevated. Global supply chain disruptions are proving more persistent, pushing up firms’ costs. And with strong demand, firms are able to pass these costs onto consumer prices. There’s growing risk that businesses and households become accustomed to higher prices, and these “transitory” prices become entrenched.

Despite the ongoing Delta outbreak, the medium-term outlook remains broadly unchanged. Employment is currently above the maximum sustainable level. And there’s risk of further tightening in the labour market. Hiring intentions have strengthened, and firms are limited to homegrown talent in their search for labour. Inflation too is accelerating. Not only has inflation already breached the top-end of the RBNZ’s 1-3% target band, but is expected to remain elevated. Global supply chain disruptions are proving more persistent, pushing up firms’ costs. And with strong demand, firms are able to pass these costs onto consumer prices. There’s growing risk that businesses and households become accustomed to higher prices, and these “transitory” prices become entrenched.

There’s enough in the inflation and labour market strength to justify normalising policy from emergency settings. And then there is the alarming growth in house prices. Annual house price growth hit a record high of 31% in August, despite the lockdown and property sales plunging. Financial stability risks are growing alongside mortgage-related debt. The MPC may not set monetary policy according to house prices, but it’s certainly the elephant in the room. Lifting the cash rate is the coolant the housing market needs.

“The Committee noted that further removal of monetary policy stimulus is expected over time, with future moves contingent on the medium-term outlook for inflation and employment.” (RBNZ MPR October’21).

SELL! No wait, BUY Kiwi!

Financial markets were (near) fully priced for the move today. Traders had prepositioned and the reaction in financial markets was relatively subdued. Interest rates continue to climb higher, and the Kiwi dollar lifted a smidge.

We expect to see a lot more out of the Kiwi in coming months.

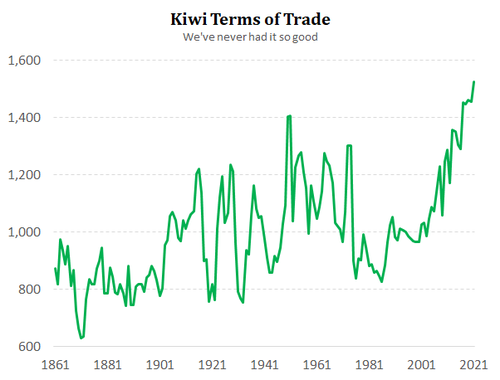

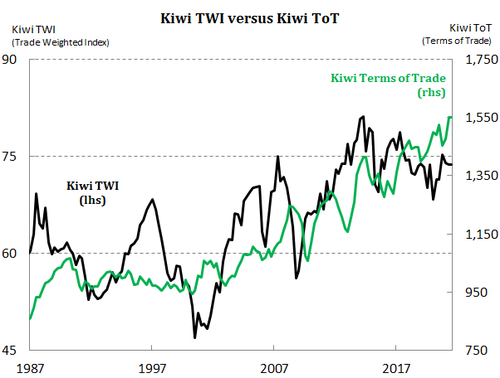

The Kiwi dollar is undervalued, in our opinion. The Kiwi dollar is a “commodity currency’, and New Zealand’s Terms of Trade is at record highs. The Terms of Trade is the highest we’ve seen over the last 160 years. New Zealand’s purchasing power has never been this good.

When compared to the Kiwi dollar, the economic fundamentals of New Zealand point to a lift.

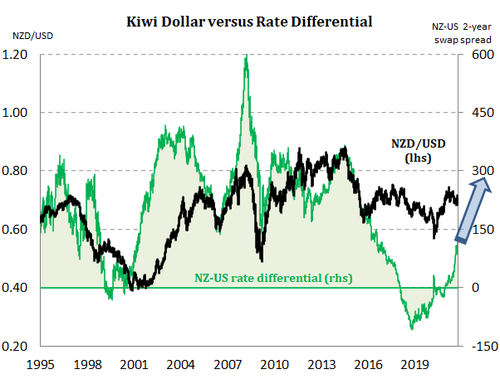

And with the RBNZ ahead of most developed market central banks, interest rate differentials also play a role in predicting the currency. The RBNZ is likely to be a year ahead of the US Fed, and possibly 2 years ahead of the RBA. The widening interest rate differentials, in NZ’s favour, point to further upside in the Kiwi dollar.

We forecast the Kiwi flyer to climb higher and end the year closer to 75c against the USD. And the Kiwi should outperform the Aussie and push towards, and through, 97c, possibly 98c.

RBNZ Statement

The Monetary Policy Committee agreed to increase the Official Cash Rate (OCR) to 0.50 per cent. Consistent with their assessment at the time of the August Statement, it is appropriate to continue reducing the level of monetary stimulus so as to maintain low inflation and support maximum sustainable employment.

The level of global economic activity has continued to recover, supported by accommodative monetary and fiscal settings, and rising vaccination rates enabling a relaxation of mobility restrictions. While economic uncertainty remains elevated due to the prevalent impact of COVID-19, cost pressures are becoming more persistent and some central banks have started the process of reducing monetary policy stimulus.

New Zealand’s public health settings are also evolving as domestic vaccination rates rise. The higher the vaccination rate, the less virus-related disruption there will be to New Zealand’s economic activity over coming years.

The current COVID-19-related restrictions have not materially changed the medium-term outlook for inflation and employment since the August Statement. Capacity pressures remain evident in the economy, particularly in the labour market. A broad range of economic indicators highlight that the New Zealand economy has been performing strongly in aggregate.

While the economy contracted sharply during the recent nationwide health-related lockdown, household and business balance sheet strength, ongoing fiscal policy support, and a strong terms of trade provide confidence that economic activity will recover quickly as alert level restrictions ease. Recent economic indicators support this picture.

However, the Committee is aware that the latest COVID-19 restrictions have badly affected some businesses in Auckland and a range of service industries more broadly. There will be longer-term implications for economic activity both domestically and internationally from the pandemic.

Headline CPI inflation is expected to increase above 4 percent in the near term before returning towards the 2 percent midpoint over the medium term. The near-term rise in inflation is accentuated by higher oil prices, rising transport costs and the impact of supply shortfalls. These immediate relative price shocks risk leading to more generalised price rises. At this time, measures of core inflation and medium-term inflation expectations remain close to 2 percent.

The Committee noted that further removal of monetary policy stimulus is expected over time, with future moves contingent on the medium-term outlook for inflation and employment.